You might also like

- Ken GriffinDocument7 pagesKen Griffinanandoiyer9No ratings yet

- Understanding Financial Statements (Review and Analysis of Straub's Book)From EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Rating: 5 out of 5 stars5/5 (5)

- Profitability Ratio DefinitionsDocument4 pagesProfitability Ratio DefinitionsOzair RahimNo ratings yet

- Putting Intelligent Insights To WorkDocument12 pagesPutting Intelligent Insights To WorkDeloitte Analytics100% (1)

- Profitability: 1-Profit Margin On Revenues 2 - Return On InvestmentDocument10 pagesProfitability: 1-Profit Margin On Revenues 2 - Return On InvestmentAhmed TaherNo ratings yet

- Trading SardinesDocument6 pagesTrading Sardinessim tykesNo ratings yet

- Income StatementDocument3 pagesIncome StatementMamta LallNo ratings yet

- Minutes of Board of Directors MeetingDocument3 pagesMinutes of Board of Directors MeetingMultiplan RINo ratings yet

- Financial Ratio & LeverageDocument25 pagesFinancial Ratio & Leverageankushrasam700No ratings yet

- CEOs Who Created Long-Term ValueDocument14 pagesCEOs Who Created Long-Term ValueSourabh NagpalNo ratings yet

- Return On EquityDocument7 pagesReturn On EquityTumwine Kahweza ProsperNo ratings yet

- Return On EquityDocument6 pagesReturn On EquitySharathNo ratings yet

- Financial TrainingDocument15 pagesFinancial TrainingGismon PereiraNo ratings yet

- Understanding The Income StatementDocument4 pagesUnderstanding The Income Statementluvujaya100% (1)

- Dupont Ratio AnalysisDocument22 pagesDupont Ratio Analysiszeeshan655100% (1)

- TopSteelmakers2013 PDFDocument32 pagesTopSteelmakers2013 PDFgobe86No ratings yet

- Profitability RatiosDocument8 pagesProfitability Ratiosbiplobsinhamats100% (1)

- AFISCO v. CADocument2 pagesAFISCO v. CASophiaFrancescaEspinosa100% (1)

- ROEDocument7 pagesROEfrancis willie m.ferangco100% (1)

- Terms of Share MarketDocument6 pagesTerms of Share Marketsearchanirban6474No ratings yet

- Analyzing Your Financial RatiosDocument38 pagesAnalyzing Your Financial Ratiossakthivels08No ratings yet

- A Study On Profitability Analysis atDocument13 pagesA Study On Profitability Analysis atAsishNo ratings yet

- Week 6 Learning Summary Financial RatiosDocument10 pagesWeek 6 Learning Summary Financial RatiosRajeev ShahdadpuriNo ratings yet

- Income Statement Gross Profit Operating Profit: FormulasDocument3 pagesIncome Statement Gross Profit Operating Profit: FormulasswapnillagadNo ratings yet

- Financial Analysis and Long-Term Planning: May Anne Aves BS Accountancy IIIDocument3 pagesFinancial Analysis and Long-Term Planning: May Anne Aves BS Accountancy IIIMeyannaNo ratings yet

- FSA Chapter 8 NotesDocument9 pagesFSA Chapter 8 NotesNadia ZahraNo ratings yet

- Key Performance IndicesDocument38 pagesKey Performance IndicesSuryanarayana TataNo ratings yet

- Profitability AnalysisDocument12 pagesProfitability AnalysisJudyeast AstillaNo ratings yet

- Financial Ratio Analysis ToolDocument6 pagesFinancial Ratio Analysis ToolJuan Pascual CosareNo ratings yet

- Financial RatiosDocument7 pagesFinancial RatiosVikram KainturaNo ratings yet

- Income Statement IIDocument9 pagesIncome Statement IIEsmer AliyevaNo ratings yet

- Monetrix Combined - FinDocument266 pagesMonetrix Combined - Fin21P028Naman Kumar GargNo ratings yet

- Definition of 'Time Value of Money - TVM'Document4 pagesDefinition of 'Time Value of Money - TVM'Chinmay P KalelkarNo ratings yet

- Analysis On Nestlé Financial Statements 2017Document7 pagesAnalysis On Nestlé Financial Statements 2017Putu DenyNo ratings yet

- Far 4Document9 pagesFar 4Sonu NayakNo ratings yet

- Net Block DefinitionsDocument16 pagesNet Block DefinitionsSabyasachi MohapatraNo ratings yet

- Financial RatiosDocument16 pagesFinancial Ratiosparidhi.b22No ratings yet

- Ratio Analysis: L. Shivakumar Financial Statement AnalysisDocument15 pagesRatio Analysis: L. Shivakumar Financial Statement AnalysisasanchezrtmNo ratings yet

- Analyze key financial ratios to assess business performanceDocument18 pagesAnalyze key financial ratios to assess business performanceAhmed AdelNo ratings yet

- Profitability Turnover RatiosDocument32 pagesProfitability Turnover RatiosAnushka JindalNo ratings yet

- Mba Fa IV Sem 406 (B) Strategic Profit ModelDocument13 pagesMba Fa IV Sem 406 (B) Strategic Profit Model462- gurveen SinghNo ratings yet

- Financial Statement AnalysisDocument14 pagesFinancial Statement AnalysisJomar TeofiloNo ratings yet

- Ratio SignificanceDocument3 pagesRatio SignificanceJonhmark AniñonNo ratings yet

- Rough Work AreaDocument7 pagesRough Work AreaAnkur SharmaNo ratings yet

- What Is Return On AssetsDocument5 pagesWhat Is Return On AssetsIndah ChaerunnisaNo ratings yet

- Financial Ratios: Use and Users of Ratio AnalysisDocument11 pagesFinancial Ratios: Use and Users of Ratio AnalysisSantosh SanNo ratings yet

- Financial RatiosDocument16 pagesFinancial Ratiospraveen bishnoiNo ratings yet

- SSF From LinnyDocument80 pagesSSF From Linnymanojpatel51No ratings yet

- Analysis On Nestlé Financial Statements 2017Document8 pagesAnalysis On Nestlé Financial Statements 2017Fred The FishNo ratings yet

- Du Pont IdentityDocument3 pagesDu Pont Identitykishorepatil8887No ratings yet

- Clo-3 Assignment: Chemical Engineering Economics 2016-CH-454Document9 pagesClo-3 Assignment: Chemical Engineering Economics 2016-CH-454ali ayanNo ratings yet

- Example Thesis On Financial Ratio AnalysisDocument8 pagesExample Thesis On Financial Ratio Analysisejqdkoaeg100% (1)

- CVP Analysis Impact on Financial StatementsDocument2 pagesCVP Analysis Impact on Financial Statementshashim rawabNo ratings yet

- Equity Capital FinancingDocument6 pagesEquity Capital FinancingMirza ShoaibbaigNo ratings yet

- Profitability Is The Ability of A Firm To Generate EarningsDocument2 pagesProfitability Is The Ability of A Firm To Generate EarningsJaneNo ratings yet

- Pertemuan 9BDocument36 pagesPertemuan 9Bleny aisyahNo ratings yet

- Enterprise Value-to-Sales - EV/Sales Definition: Key TakeawaysDocument13 pagesEnterprise Value-to-Sales - EV/Sales Definition: Key Takeawaysprabhubhai sapoliyaNo ratings yet

- BA Financial RatiosDocument54 pagesBA Financial RatiosVolker MeyerNo ratings yet

- DuPont Analysis15training3Document5 pagesDuPont Analysis15training3Noel KlNo ratings yet

- Valuation - NotesDocument41 pagesValuation - NotessreginatoNo ratings yet

- Latihan Kata Sendi NamaDocument6 pagesLatihan Kata Sendi NamasaangetaaNo ratings yet

- Summary PERFORMANCE MEASUREMENT IN DECENTRALIZED ORGANIZATIONSDocument9 pagesSummary PERFORMANCE MEASUREMENT IN DECENTRALIZED ORGANIZATIONSliaNo ratings yet

- 03-Measures of Perfomance in Private SectorDocument5 pages03-Measures of Perfomance in Private SectorHastings KapalaNo ratings yet

- Financial TermsDocument1 pageFinancial TermsKaushik GhoshNo ratings yet

- Basic Accountin Written Assignment SubmissionDocument2 pagesBasic Accountin Written Assignment SubmissionMailu ShirlNo ratings yet

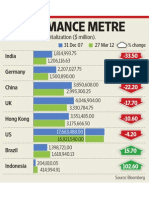

- Market Capitalization Changes of Major Economies 2007-2012Document1 pageMarket Capitalization Changes of Major Economies 2007-2012andrewpereiraNo ratings yet

- Daily DerivativesDocument2 pagesDaily DerivativesandrewpereiraNo ratings yet

- DEFY nonBLUR UG UK EN 68014494001Document66 pagesDEFY nonBLUR UG UK EN 68014494001slatvpmNo ratings yet

- Algorithmic Trading An OverviewDocument20 pagesAlgorithmic Trading An Overviewsaurabh_goyal_10No ratings yet

- Organization, Objectives and Services of India's Export-Import BankDocument2 pagesOrganization, Objectives and Services of India's Export-Import BankandrewpereiraNo ratings yet

- Promoting India's International Trade and Economic GrowthDocument9 pagesPromoting India's International Trade and Economic GrowthandrewpereiraNo ratings yet

- Organization, Objectives and Services of India's Export-Import BankDocument2 pagesOrganization, Objectives and Services of India's Export-Import BankandrewpereiraNo ratings yet

- Tata Motors: Performance HighlightsDocument10 pagesTata Motors: Performance HighlightsandrewpereiraNo ratings yet

- The Non-Deliverable Forward (NDF) Market For The Indian RupeeDocument9 pagesThe Non-Deliverable Forward (NDF) Market For The Indian RupeeandrewpereiraNo ratings yet

- MCB Bank Limited Formerly Known As Muslim Commercial Bank Limited Was Incorporated by The Adamjee Group On July 9Document6 pagesMCB Bank Limited Formerly Known As Muslim Commercial Bank Limited Was Incorporated by The Adamjee Group On July 9Imdad Ali JokhioNo ratings yet

- TVM Exercises in Cash Flow Mapping 1Document2 pagesTVM Exercises in Cash Flow Mapping 1Cherry Anne TolentinoNo ratings yet

- Asian PaintsDocument19 pagesAsian PaintsAmrita KaurNo ratings yet

- EventDocument14 pagesEventVenkatesh VNo ratings yet

- Page 18 To 19Document2 pagesPage 18 To 19Judith CastroNo ratings yet

- Commodity Derivatives Study NotesDocument24 pagesCommodity Derivatives Study NotesAkshaya Investmentz100% (1)

- Finance GlosaryDocument102 pagesFinance GlosaryChandra Shekhar VeldandiNo ratings yet

- Related Parties Problem 4-1: D. Two Ventures Simply Because They Share Joint Control Over Joint VentureDocument3 pagesRelated Parties Problem 4-1: D. Two Ventures Simply Because They Share Joint Control Over Joint Venturejake doinogNo ratings yet

- Balance Sheet of Itc LTDDocument7 pagesBalance Sheet of Itc LTDMarri Sushma Swaraj ReddyNo ratings yet

- Management Accounting Concepts and TechniquesDocument277 pagesManagement Accounting Concepts and TechniquesCalvince OumaNo ratings yet

- Unit-III - EEFA - CostsDocument70 pagesUnit-III - EEFA - CostsRamalingam ChandrasekharanNo ratings yet

- 4.6. Phar-MorDocument4 pages4.6. Phar-Morviethoangvn100% (1)

- Ashish Srivastava ProjectDocument112 pagesAshish Srivastava ProjectSachin LeeNo ratings yet

- 6 Negligent MisstatementDocument3 pages6 Negligent MisstatementJon Black-TiongNo ratings yet

- Equipment Replacement PolicyDocument4 pagesEquipment Replacement PolicyRohan DhandNo ratings yet

- High Rock Industries CaseDocument19 pagesHigh Rock Industries CaseRohan Raj MishraNo ratings yet

- Index Investing & Financial Independence For Expats: Getting Started GuideDocument54 pagesIndex Investing & Financial Independence For Expats: Getting Started GuideAmr Mustafa ToradNo ratings yet

- FEASIBDocument49 pagesFEASIBJeffrel Mae Montaño BrilloNo ratings yet

- Understanding 2011 Rate Case Primer for Carolinas Electric UtilitiesDocument3 pagesUnderstanding 2011 Rate Case Primer for Carolinas Electric UtilitiesShanthi SelvamNo ratings yet

- MCK 13Document5 pagesMCK 13chandumicrocosm1986No ratings yet

- Jungheinrich AG: Germany - EngineeringDocument8 pagesJungheinrich AG: Germany - EngineeringSwagata DharNo ratings yet

- BASIX Relationship Management SheetDocument22 pagesBASIX Relationship Management SheetAnantha LakshmiNo ratings yet

- Indo US Ventures Case DebriefDocument19 pagesIndo US Ventures Case DebriefYazad AdajaniaNo ratings yet