You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Updated Japan Visa RequirementsDocument2 pagesUpdated Japan Visa RequirementsRheneir MoraNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Meditation For AddictionDocument2 pagesMeditation For AddictionharryNo ratings yet

- Pilapil v. CADocument2 pagesPilapil v. CAIris Gallardo100% (2)

- Session 4 - QAR Audit Methodology Manual - Pre-Engagement, Planning and Test of ControlsDocument55 pagesSession 4 - QAR Audit Methodology Manual - Pre-Engagement, Planning and Test of ControlsRheneir Mora100% (1)

- Session 6 - QAR Audit Methodology Manual Presentation - Review and FinalizationDocument23 pagesSession 6 - QAR Audit Methodology Manual Presentation - Review and FinalizationRheneir MoraNo ratings yet

- Session 2 - QAR Audit Methodology Manual - IsQMDocument49 pagesSession 2 - QAR Audit Methodology Manual - IsQMRheneir MoraNo ratings yet

- Session 5 - QAR Audit Methodology Manual Presentation - Detailed ProcedureDocument18 pagesSession 5 - QAR Audit Methodology Manual Presentation - Detailed ProcedureRheneir MoraNo ratings yet

- ANSI-ISA-S5.4-1991 - Instrument Loop DiagramsDocument22 pagesANSI-ISA-S5.4-1991 - Instrument Loop DiagramsCarlos Poveda100% (2)

- Session 1 - QAR Audit Methodology Manual Presentation - Fundamentals of PSA AuditDocument34 pagesSession 1 - QAR Audit Methodology Manual Presentation - Fundamentals of PSA AuditRheneir MoraNo ratings yet

- E Tech SLHT QTR 2 Week 1Document11 pagesE Tech SLHT QTR 2 Week 1Vie Boldios Roche100% (1)

- Chapter 16 - Test Bank Chem 200Document110 pagesChapter 16 - Test Bank Chem 200Jan Chester Chan80% (5)

- Semiotics Study of Movie ShrekDocument15 pagesSemiotics Study of Movie Shreky2pinku100% (1)

- Session 3 - QAR Audit Methodology Manual Presentation - Intro To The ManualDocument12 pagesSession 3 - QAR Audit Methodology Manual Presentation - Intro To The ManualRheneir MoraNo ratings yet

- 5g-core-guide-building-a-new-world Переход от лте к 5г английскийDocument13 pages5g-core-guide-building-a-new-world Переход от лте к 5г английскийmashaNo ratings yet

- Electronic Ticket Receipt 26MAR For RHENEIR PARAN MORADocument3 pagesElectronic Ticket Receipt 26MAR For RHENEIR PARAN MORARheneir MoraNo ratings yet

- 4as Lesson PlanDocument10 pages4as Lesson PlanMannuelle Gacud100% (2)

- Cebu Pacific Air MoraDocument4 pagesCebu Pacific Air MoraRheneir MoraNo ratings yet

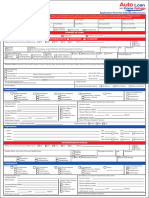

- New Auto-Loan-Application-Form - IndividualDocument2 pagesNew Auto-Loan-Application-Form - IndividualRheneir MoraNo ratings yet

- Peach Confirmation EU88X5Document3 pagesPeach Confirmation EU88X5Rheneir MoraNo ratings yet

- CVR-16 InviteDocument3 pagesCVR-16 InviteRheneir MoraNo ratings yet

- Peach Confirmation QQ5775Document3 pagesPeach Confirmation QQ5775Rheneir MoraNo ratings yet

- Fun Golf SolicitationDocument2 pagesFun Golf SolicitationRheneir MoraNo ratings yet

- Differences PFRSDocument11 pagesDifferences PFRSRheneir MoraNo ratings yet

- Certificate SphinxDocument1 pageCertificate SphinxRheneir MoraNo ratings yet

- SourceTech Consultancy LLCDocument11 pagesSourceTech Consultancy LLCRheneir MoraNo ratings yet

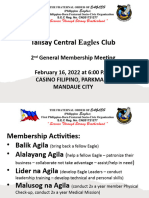

- GMM ProgramDocument1 pageGMM ProgramRheneir MoraNo ratings yet

- PAREB AMLC Online Registration System GuideDocument72 pagesPAREB AMLC Online Registration System GuideRheneir MoraNo ratings yet

- Talisay Central Eagles ClubDocument5 pagesTalisay Central Eagles ClubRheneir MoraNo ratings yet

- 49 Insights July 2022Document41 pages49 Insights July 2022Rheneir MoraNo ratings yet

- 1MSADocument1 page1MSARheneir MoraNo ratings yet

- MS Call CardsDocument3 pagesMS Call CardsRheneir MoraNo ratings yet

- 77th ANC CebuDocument7 pages77th ANC CebuRheneir MoraNo ratings yet

- 2019notice New Forms and Pre EvaluationDocument29 pages2019notice New Forms and Pre EvaluationRheneir MoraNo ratings yet

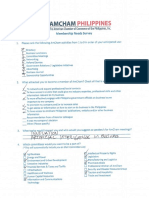

- Amcham Phil. Membership SurveyDocument2 pagesAmcham Phil. Membership SurveyRheneir Mora100% (1)

- 04 Property PicturesDocument1 page04 Property PicturesRheneir MoraNo ratings yet

- Financial ManagementDocument55 pagesFinancial ManagementRheneir MoraNo ratings yet

- 03 - List of PropertiesDocument4 pages03 - List of PropertiesRheneir MoraNo ratings yet

- Implementing Rules and Regulations of The Lending Company Regulation Act of 2007 Ra9474Document19 pagesImplementing Rules and Regulations of The Lending Company Regulation Act of 2007 Ra9474Lance DionelaNo ratings yet

- Img - Oriental Magic by Idries Shah ImageDocument119 pagesImg - Oriental Magic by Idries Shah ImageCarolos Strangeness Eaves100% (2)

- 6401 1 NewDocument18 pages6401 1 NewbeeshortNo ratings yet

- Circular No 02 2014 TA DA 010115 PDFDocument10 pagesCircular No 02 2014 TA DA 010115 PDFsachin sonawane100% (1)

- HDFC Bank-Centurion Bank of Punjab: Presented By: Sachi Bani Perhar Mba-Ib 2010-2012Document40 pagesHDFC Bank-Centurion Bank of Punjab: Presented By: Sachi Bani Perhar Mba-Ib 2010-2012Sumit MalikNo ratings yet

- лк CUDA - 1 PDCnDocument31 pagesлк CUDA - 1 PDCnОлеся БарковськаNo ratings yet

- Chemistry InvestigatoryDocument16 pagesChemistry InvestigatoryVedant LadheNo ratings yet

- MagmatismDocument12 pagesMagmatismVea Patricia Angelo100% (1)

- Ulster Cycle - WikipediaDocument8 pagesUlster Cycle - WikipediazentropiaNo ratings yet

- DE1734859 Central Maharashtra Feb'18Document39 pagesDE1734859 Central Maharashtra Feb'18Adesh NaharNo ratings yet

- Holophane Denver Elite Bollard - Spec Sheet - AUG2022Document3 pagesHolophane Denver Elite Bollard - Spec Sheet - AUG2022anamarieNo ratings yet

- Notice: Grant and Cooperative Agreement Awards: Public Housing Neighborhood Networks ProgramDocument3 pagesNotice: Grant and Cooperative Agreement Awards: Public Housing Neighborhood Networks ProgramJustia.comNo ratings yet

- Symptoms: Generalized Anxiety Disorder (GAD)Document3 pagesSymptoms: Generalized Anxiety Disorder (GAD)Nur WahyudiantoNo ratings yet

- Sheet PilesDocument5 pagesSheet PilesolcayuzNo ratings yet

- Past Simple of BeDocument2 pagesPast Simple of BeRoxana ClepeNo ratings yet

- Unit 7Document10 pagesUnit 7Christopher EddyNo ratings yet

- Financial Performance Report General Tyres and Rubber Company-FinalDocument29 pagesFinancial Performance Report General Tyres and Rubber Company-FinalKabeer QureshiNo ratings yet

- The Leaders of The NationDocument3 pagesThe Leaders of The NationMark Dave RodriguezNo ratings yet

- FCAPSDocument5 pagesFCAPSPablo ParreñoNo ratings yet

- User Manual For Inquisit's Attentional Network TaskDocument5 pagesUser Manual For Inquisit's Attentional Network TaskPiyush ParimooNo ratings yet

- Karnataka BankDocument6 pagesKarnataka BankS Vivek BhatNo ratings yet

- ANI Network - Quick Bill Pay PDFDocument2 pagesANI Network - Quick Bill Pay PDFSandeep DwivediNo ratings yet

- Brahm Dutt v. UoiDocument3 pagesBrahm Dutt v. Uoiswati mohapatraNo ratings yet