You might also like

- Company Finance Profit & Loss Nestle India LTDDocument16 pagesCompany Finance Profit & Loss Nestle India LTDKeshav MishraNo ratings yet

- Term Paper OF Accounting For Managers ON Ashoak Leyland: Lovely Professional UniversityDocument9 pagesTerm Paper OF Accounting For Managers ON Ashoak Leyland: Lovely Professional Universitymanpreet1415No ratings yet

- Industry Segment of Bajaj CompanyDocument4 pagesIndustry Segment of Bajaj CompanysantunusorenNo ratings yet

- ValuationDocument31 pagesValuationAman TaterNo ratings yet

- Financial Management AssignmentDocument5 pagesFinancial Management AssignmentSREEJITH RNo ratings yet

- Business Valuation End TermDocument19 pagesBusiness Valuation End TermVaishali GuptaNo ratings yet

- 4808 Rishab Bansal Excel 39919 1194528774Document27 pages4808 Rishab Bansal Excel 39919 1194528774Rishab BansalNo ratings yet

- Group 1 Adani PortsDocument12 pagesGroup 1 Adani PortsshreechaNo ratings yet

- Divi's Laboratories LTD: Finanance For Managers Activity 2Document10 pagesDivi's Laboratories LTD: Finanance For Managers Activity 2Madhan kumarNo ratings yet

- AFM Project Report FinalDocument19 pagesAFM Project Report FinalRitu KumariNo ratings yet

- Group Project - ACCDocument17 pagesGroup Project - ACCLovie GuptaNo ratings yet

- A Summer Project Report OnDocument17 pagesA Summer Project Report OnHarsh MidhaNo ratings yet

- Juhayna Food Industries: in Millions of EGP (Except For Per Share Items)Document11 pagesJuhayna Food Industries: in Millions of EGP (Except For Per Share Items)Shokry AminNo ratings yet

- Assignment1 PDFDocument93 pagesAssignment1 PDFNaman NandwanaNo ratings yet

- Ration AnalysisDocument9 pagesRation AnalysisAaryan RichhariyaNo ratings yet

- Assingment SCM SEM4 - 1Document17 pagesAssingment SCM SEM4 - 1KARTHIYAENI VNo ratings yet

- Financial Statement AnalysisDocument18 pagesFinancial Statement AnalysisEashaa SaraogiNo ratings yet

- Balance Sheet of Tata Communications: - in Rs. Cr.Document24 pagesBalance Sheet of Tata Communications: - in Rs. Cr.ankush birlaNo ratings yet

- Swot Analysis I. Strenghts: WeaknessesDocument5 pagesSwot Analysis I. Strenghts: WeaknessesNiveditha MNo ratings yet

- Account Assigment DDDocument6 pagesAccount Assigment DDlubna ghazalNo ratings yet

- Balance Sheet of Zuari GlobalDocument4 pagesBalance Sheet of Zuari GlobalmaheshfbNo ratings yet

- Three Statement Model (Beauty of Our FM - ADF) - CompletedDocument9 pagesThree Statement Model (Beauty of Our FM - ADF) - CompletedAnkit SharmaNo ratings yet

- Names of Team Members Roll No Criteria For Selection of Main CompanyDocument31 pagesNames of Team Members Roll No Criteria For Selection of Main CompanyGaurav SharmaNo ratings yet

- Balance SheeetDocument3 pagesBalance SheeetHiren VagadiyaNo ratings yet

- Mini Project Financial Reporting Statements and Analysis MB20104Document11 pagesMini Project Financial Reporting Statements and Analysis MB20104KISHORE KRISHNo ratings yet

- Birla RatioDocument22 pagesBirla RatioveeraranjithNo ratings yet

- Gujarat Narmada Valley Fertilizers & ChemicalsDocument14 pagesGujarat Narmada Valley Fertilizers & ChemicalsPrashant TiwariNo ratings yet

- Colgate Palmolive (India) : Mid-Term Assignment Subject: Accounting For Managerial Decision MakingDocument5 pagesColgate Palmolive (India) : Mid-Term Assignment Subject: Accounting For Managerial Decision MakingIMRAN ALAMNo ratings yet

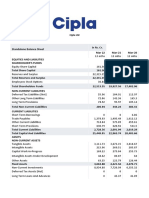

- Cipla LTDDocument6 pagesCipla LTDscribd sogawNo ratings yet

- FA Ratios AssignmentDocument61 pagesFA Ratios AssignmentShambhavi SinhaNo ratings yet

- PVR RatioDocument14 pagesPVR RatioApurwa SawarkarNo ratings yet

- Long Hau LGH - Sonadezi Chau Duc SZC - Case Study Group17Document75 pagesLong Hau LGH - Sonadezi Chau Duc SZC - Case Study Group17Trung Hung HoNo ratings yet

- Guj AlkaliDocument8 pagesGuj AlkalirotiNo ratings yet

- Balance Sheet of Gujarat Alkalies and ChemicalsDocument8 pagesBalance Sheet of Gujarat Alkalies and ChemicalsrotiNo ratings yet

- Guj AlkaliDocument8 pagesGuj AlkalirotiNo ratings yet

- National Aluminium Company LTD Balance Sheet: Non-Current AssetsDocument25 pagesNational Aluminium Company LTD Balance Sheet: Non-Current AssetsSmall Town BandaNo ratings yet

- Long Hau LGH - Sonadezi Chau Duc SZC - Case Study Q7 ReviewDocument59 pagesLong Hau LGH - Sonadezi Chau Duc SZC - Case Study Q7 ReviewTrung Hung HoNo ratings yet

- Financial Summary: Annual Report 2076/77Document1 pageFinancial Summary: Annual Report 2076/77Panchakanya SaccosNo ratings yet

- Ratio Analysis Berger Asian PaintsDocument11 pagesRatio Analysis Berger Asian PaintsHEM BANSALNo ratings yet

- Hawkins Cooker LimitedDocument9 pagesHawkins Cooker LimitedShreshtha SinghNo ratings yet

- Cash Flow Statement Examples2Document8 pagesCash Flow Statement Examples2ReactorAkkharNo ratings yet

- Case Study On Financial Risk AnalysisDocument6 pagesCase Study On Financial Risk AnalysisolafedNo ratings yet

- Ratios Report Ambuja CementDocument11 pagesRatios Report Ambuja CementSajal GoyalNo ratings yet

- Aegis Logistics ResearchDocument4 pagesAegis Logistics ResearchSneha ChavanNo ratings yet

- BirlasoftDocument3 pagesBirlasoftlubna ghazalNo ratings yet

- Content ACCOUNTSDocument7 pagesContent ACCOUNTSjhanvi tandonNo ratings yet

- Waa Solar Financial AnalysisDocument18 pagesWaa Solar Financial AnalysisINBASEKARAN PNo ratings yet

- Ratios of HDFC BankDocument50 pagesRatios of HDFC BankrupaliNo ratings yet

- Customised Dupont AnalysisDocument1 pageCustomised Dupont AnalysisbhuvaneshkmrsNo ratings yet

- Scooter TrendsDocument107 pagesScooter TrendsRima ParekhNo ratings yet

- Havells Balance Sheet (4 Years)Document15 pagesHavells Balance Sheet (4 Years)Tamoghna MaitraNo ratings yet

- ASN SOD Finacial AnalysisDocument6 pagesASN SOD Finacial Analysisjitendra tirthyaniNo ratings yet

- Sapm Stock AnalysisDocument23 pagesSapm Stock AnalysisAthira K. ANo ratings yet

- Fin658 Set 1 Question - Final Jul2022Document8 pagesFin658 Set 1 Question - Final Jul2022Ahmad Lokman MukminNo ratings yet

- ABB India: PrintDocument2 pagesABB India: PrintAbhay Kumar SinghNo ratings yet

- Income: Profit & Loss Account of Abc LTD (In Rs. CR.)Document13 pagesIncome: Profit & Loss Account of Abc LTD (In Rs. CR.)SukantaNo ratings yet

- Accountancy ProjectDocument27 pagesAccountancy ProjectSherin nashwaNo ratings yet

- Financial Report of Shivam Cement by SampurnaDocument24 pagesFinancial Report of Shivam Cement by SampurnaSampurna PoudelNo ratings yet

- Data To Use - Detail InformationDocument44 pagesData To Use - Detail InformationAninda DuttaNo ratings yet

- Merchant Banking - Basics by SayleeDocument36 pagesMerchant Banking - Basics by Sayleesaylee24No ratings yet

- ViewDocument24 pagesViewmanishshinde22No ratings yet

- Model Questions - Jaiib Principles of Banking - Module A & BDocument10 pagesModel Questions - Jaiib Principles of Banking - Module A & Bapi-3808761No ratings yet

- Customer Loyalty Towards Retail Outlet: Retail Marketing - Project ProposalDocument10 pagesCustomer Loyalty Towards Retail Outlet: Retail Marketing - Project ProposalkalathiadhavalNo ratings yet

- Book 1Document1 pageBook 1kalathiadhavalNo ratings yet

- Book 1Document1 pageBook 1kalathiadhavalNo ratings yet

- Contoh Resume Dan CVDocument4 pagesContoh Resume Dan CVsytyeweynaNo ratings yet

- 020 2003 MercantDocument22 pages020 2003 MercantRamVasiNo ratings yet

- Mou System: SPS Solanki AGM (CP)Document82 pagesMou System: SPS Solanki AGM (CP)SamNo ratings yet

- Aviation Leaders Programme in Public Policy - SingaporeDocument1 pageAviation Leaders Programme in Public Policy - SingaporeAnonymous tSYkkHToBPNo ratings yet

- CLEOFAS ComparativeAnalysisDocument12 pagesCLEOFAS ComparativeAnalysiskeithNo ratings yet

- Gautam Resume PDFDocument4 pagesGautam Resume PDFGautam BhallaNo ratings yet

- Public Health Engineering Department, Haryana Public Health Engineering Division No.2, Panipat Notice Inviting TenderDocument17 pagesPublic Health Engineering Department, Haryana Public Health Engineering Division No.2, Panipat Notice Inviting Tenderpmcmbharat264No ratings yet

- Packplus 2018 - Exhibitors Details Invitation Show Area Stand No. Hall Form 1 Status Zone GST NumberDocument75 pagesPackplus 2018 - Exhibitors Details Invitation Show Area Stand No. Hall Form 1 Status Zone GST NumberTruck Trailer & Tyre ExpoNo ratings yet

- Business Terms and GlossaryDocument31 pagesBusiness Terms and GlossaryRavi ManiyarNo ratings yet

- Construction Management (CENG 260) : Lecturer: Raed T. Jarrah Lecture 11a - Cost ControlDocument19 pagesConstruction Management (CENG 260) : Lecturer: Raed T. Jarrah Lecture 11a - Cost ControlHusseinNo ratings yet

- Resetting The Standards FinalDocument27 pagesResetting The Standards FinaltabbforumNo ratings yet

- Ajay Kumar SethyDocument96 pagesAjay Kumar SethyShakti MohapatraNo ratings yet

- City of Malabon University: Senior High SchoolDocument8 pagesCity of Malabon University: Senior High SchoolSean Harvey BautistaNo ratings yet

- An Introduction To Supply Base Management PDFDocument16 pagesAn Introduction To Supply Base Management PDFAmrin Diba100% (1)

- CorpWatch - What Is NeoliberalismDocument2 pagesCorpWatch - What Is NeoliberalismsanjnuNo ratings yet

- Techknowlogia Journal 2000 Mac AprilDocument68 pagesTechknowlogia Journal 2000 Mac AprilMazlan ZulkiflyNo ratings yet

- Eric Khrom of Khrom Capital 2012 Q3 LetterDocument5 pagesEric Khrom of Khrom Capital 2012 Q3 LetterallaboutvalueNo ratings yet

- Motor CertificateDocument1 pageMotor CertificateNeil VickeryNo ratings yet

- University of The Punjab: NOTIFICATION NO.309 /Cond.D.SDocument2 pagesUniversity of The Punjab: NOTIFICATION NO.309 /Cond.D.SZain Ul AbideenNo ratings yet

- Smile CardDocument2 pagesSmile CardSahajPuriNo ratings yet

- SAP Archiving StrategyDocument36 pagesSAP Archiving StrategyHariharan ChoodamaniNo ratings yet

- PWAL - Technical Proposal On AuditDocument63 pagesPWAL - Technical Proposal On AuditOlufemi MoyegunNo ratings yet

- 260CT Revision NotesDocument30 pages260CT Revision NotesSalman Fazal100% (4)

- Place of Supply: After Studying This Chapter, You Will Be Able ToDocument85 pagesPlace of Supply: After Studying This Chapter, You Will Be Able ToRohit SoniNo ratings yet

- GAMA 2017 AnnualReport ForWeb Final PDFDocument60 pagesGAMA 2017 AnnualReport ForWeb Final PDFYangNo ratings yet

- SLUPDocument1 pageSLUPMaria Lee100% (1)

- Amazon Consolidated Interview Experience DocumentDocument4 pagesAmazon Consolidated Interview Experience DocumentNiraj Kumar100% (1)

- 1 An Introduction Investing and ValuationDocument19 pages1 An Introduction Investing and ValuationEmmeline ASNo ratings yet

- D, Aveni, Richard, A, (1995) Coping With Hypercompetition Utilizing The New 7S S FrameworkDocument13 pagesD, Aveni, Richard, A, (1995) Coping With Hypercompetition Utilizing The New 7S S Frameworkeduardoaleman2015No ratings yet

- Global Information Technology Report 2004/2005 Executive SummaryDocument5 pagesGlobal Information Technology Report 2004/2005 Executive SummaryWorld Economic Forum50% (2)