You might also like

- Compensation of General Partners of Private Equity FundsDocument6 pagesCompensation of General Partners of Private Equity FundsManu Midha100% (1)

- Equitable Recoupment Tax AssumptionDocument5 pagesEquitable Recoupment Tax AssumptionErwin April MidsapakNo ratings yet

- BIR RULING (DA - (C-168) 519-08) - Liquidated DamagesDocument8 pagesBIR RULING (DA - (C-168) 519-08) - Liquidated Damagesjohn allen MarillaNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Corporate Finance MCQsDocument0 pagesCorporate Finance MCQsonlyjaded4655100% (1)

- Cir VS BurroughDocument2 pagesCir VS BurroughMP ManliclicNo ratings yet

- Digest (1986 To 2016)Document151 pagesDigest (1986 To 2016)Jerwin DaveNo ratings yet

- Case Digest - OPT and DSTDocument30 pagesCase Digest - OPT and DSTGlargo GlargoNo ratings yet

- Coa 2015-014Document2 pagesCoa 2015-014melizze100% (2)

- Of of of The For TheirDocument7 pagesOf of of The For TheirKatherine MakalintalNo ratings yet

- Philippine Supreme Court Case on Creditor Rights in Property ForeclosureDocument18 pagesPhilippine Supreme Court Case on Creditor Rights in Property ForeclosureSalma GurarNo ratings yet

- CIR v. CA: Employees' Trusts Exempt from Withholding TaxDocument2 pagesCIR v. CA: Employees' Trusts Exempt from Withholding TaxRem SerranoNo ratings yet

- Request of Atty. ZialcitaDocument2 pagesRequest of Atty. ZialcitaAngelo Castillo100% (1)

- Investing Is Most Intelligent When It Is Most BusinesslikeDocument3 pagesInvesting Is Most Intelligent When It Is Most BusinesslikeKohinoor RoyNo ratings yet

- TAX-07-GROSS-INCOME (With Answers)Document12 pagesTAX-07-GROSS-INCOME (With Answers)Kendrew SujideNo ratings yet

- CIR Vs CA, CTA, and GCL Retirement Plan TAXDocument2 pagesCIR Vs CA, CTA, and GCL Retirement Plan TAXLemuel Angelo M. Eleccion100% (1)

- Filipinas Life Assurance Company v. CTADocument1 pageFilipinas Life Assurance Company v. CTADemi Lewk100% (2)

- Annual Report 2014Document110 pagesAnnual Report 2014Kevin Brown0% (1)

- 06 Gross IncomeDocument103 pages06 Gross IncomeJSNo ratings yet

- CIR v. CTA, GCLDocument2 pagesCIR v. CTA, GCLIan GanasNo ratings yet

- CIR vs. Procter and GambleDocument3 pagesCIR vs. Procter and GambleRobNo ratings yet

- CIR Vs CA, CTA, GCLDocument3 pagesCIR Vs CA, CTA, GCLNoel GalitNo ratings yet

- Commissioner of Internal Revenue vs. Premium Leisure Corp. CTA (En Banc)Document1 pageCommissioner of Internal Revenue vs. Premium Leisure Corp. CTA (En Banc)kimNo ratings yet

- Sema Vs COMELEC PDFDocument2 pagesSema Vs COMELEC PDFHerzl Hali V. HermosaNo ratings yet

- Barreto V VillanuevaDocument1 pageBarreto V VillanuevaSalma GurarNo ratings yet

- Insolvency-Suspension of PaymentsDocument8 pagesInsolvency-Suspension of PaymentsSalma GurarNo ratings yet

- Taxation of retirement benefits in Zialcita caseDocument2 pagesTaxation of retirement benefits in Zialcita caseJustin LoredoNo ratings yet

- Deutsche Bank Ag Manila Branch vs. CirDocument2 pagesDeutsche Bank Ag Manila Branch vs. CirSalma Gurar100% (3)

- Commissioner v. Goodyear Philippines tax treaty governs redemptionDocument2 pagesCommissioner v. Goodyear Philippines tax treaty governs redemptionAnn QuebecNo ratings yet

- Wise Vs MeerDocument2 pagesWise Vs MeerSalma GurarNo ratings yet

- Wise Vs MeerDocument2 pagesWise Vs MeerSalma GurarNo ratings yet

- Balboa Vs FarralesDocument1 pageBalboa Vs FarralesSalma GurarNo ratings yet

- Balboa Vs FarralesDocument1 pageBalboa Vs FarralesSalma GurarNo ratings yet

- Cir Vs CastanedaDocument2 pagesCir Vs CastanedaAyra CadigalNo ratings yet

- CIR v. CA and Castaneda GR 96016 October 17, 1991Document1 pageCIR v. CA and Castaneda GR 96016 October 17, 1991Vel JuneNo ratings yet

- Vera Vs NavarroDocument1 pageVera Vs NavarroSalma GurarNo ratings yet

- 020 Island Power Corp V CirDocument2 pages020 Island Power Corp V CirNorman ManaloNo ratings yet

- CIR V CA and GCLDocument2 pagesCIR V CA and GCLWilliam SantosNo ratings yet

- TAX Digests Cases BenefitsDocument7 pagesTAX Digests Cases BenefitsRomhead SJNo ratings yet

- CIR v. GCL Retirement Plan Exemption from Withholding TaxDocument3 pagesCIR v. GCL Retirement Plan Exemption from Withholding TaxIan VillafuerteNo ratings yet

- Highlighted CIR v. Castaneda, G.R. No. 96016, October 17, 1991, 203 SCRA 72.htmlDocument2 pagesHighlighted CIR v. Castaneda, G.R. No. 96016, October 17, 1991, 203 SCRA 72.htmlCharity RomagaNo ratings yet

- Catipay - Case Study #2Document3 pagesCatipay - Case Study #2Riza DizonNo ratings yet

- 13-14. Commissioner of Internal Revenue Vs CA and GCL IncDocument2 pages13-14. Commissioner of Internal Revenue Vs CA and GCL IncEANo ratings yet

- 12 CIR vs. CADocument1 page12 CIR vs. CAKristie Renz Anne PanesNo ratings yet

- Taxation LMT by Atty. LoanzonDocument13 pagesTaxation LMT by Atty. LoanzonDeon marianoNo ratings yet

- URA V Siraje Hassan Kajura Supreme CourtDocument7 pagesURA V Siraje Hassan Kajura Supreme CourtMusiime Katumbire Hillary50% (2)

- CIR v. CA, 207 SCRA 487 (1992) PDFDocument5 pagesCIR v. CA, 207 SCRA 487 (1992) PDFsbce14No ratings yet

- CIR Vs GCL Retirement PlanDocument2 pagesCIR Vs GCL Retirement PlanFranz GarciaNo ratings yet

- 4 Commissioner - of - Internal - Revenue - v. - Court - ofDocument8 pages4 Commissioner - of - Internal - Revenue - v. - Court - ofClaire SantosNo ratings yet

- G.R. No. 96016 October 17, 1991 Commissioner of Internal Revenue, Petitioner, vs. The Court of Appeals and Efren P. Castaneda, RespondentsDocument1 pageG.R. No. 96016 October 17, 1991 Commissioner of Internal Revenue, Petitioner, vs. The Court of Appeals and Efren P. Castaneda, RespondentsCristy Yaun-CabagnotNo ratings yet

- Glorilyn M. Montejo 8-14 Cases On Double or Tax Exemption CIR vs. CA G.R. No. 95022 207 March 23, 1992 SCRA 487 Tax Exemption FactsDocument10 pagesGlorilyn M. Montejo 8-14 Cases On Double or Tax Exemption CIR vs. CA G.R. No. 95022 207 March 23, 1992 SCRA 487 Tax Exemption FactsAna leah Orbeta-mamburamNo ratings yet

- Petitioner vs. vs. Respondents Leovigildo Monasterial: Second DivisionDocument2 pagesPetitioner vs. vs. Respondents Leovigildo Monasterial: Second DivisionVMNo ratings yet

- CIR vs. Castaneda Tax RulingDocument1 pageCIR vs. Castaneda Tax RulingLisa GarciaNo ratings yet

- Xiii Xvi ReviewerDocument38 pagesXiii Xvi Reviewerjuna luz latigayNo ratings yet

- XIII-XVI ReviewerDocument53 pagesXIII-XVI Reviewerjuna luz latigayNo ratings yet

- 4 - Cir Vs Procter ND CambleDocument15 pages4 - Cir Vs Procter ND CambleMark Paul CortejosNo ratings yet

- GCL Retirement Plan Tax RefundDocument6 pagesGCL Retirement Plan Tax RefundLord AumarNo ratings yet

- CIR vs Court of Appeals - Terminal leave pay tax exemptionDocument1 pageCIR vs Court of Appeals - Terminal leave pay tax exemptionBenjie SalesNo ratings yet

- Taxation of Corporate Dividends and Stock DividendsDocument16 pagesTaxation of Corporate Dividends and Stock DividendsGeralyn GabrielNo ratings yet

- Tax Exemption of Retirement BenefitsDocument6 pagesTax Exemption of Retirement BenefitsAllan YdiaNo ratings yet

- Proctor and GambleDocument64 pagesProctor and GambleAnonymous sBdR2FxYQjNo ratings yet

- A.M. No. 90-6-015-SC October 18, 1990Document5 pagesA.M. No. 90-6-015-SC October 18, 1990AngelNo ratings yet

- Unit 2 - Income From SalaryDocument14 pagesUnit 2 - Income From SalaryRakhi DhamijaNo ratings yet

- Cir Vs Procter and GambleDocument36 pagesCir Vs Procter and GamblecarmineNo ratings yet

- Tax LSPU Final Examination March 2016 AnswersDocument10 pagesTax LSPU Final Examination March 2016 AnswersKring de VeraNo ratings yet

- Employee Benefits and Retirement PlanningDocument20 pagesEmployee Benefits and Retirement PlanningchiposityNo ratings yet

- Commissioner of Internal Revenue v. Procter and Gamble G.R. L-66838Document11 pagesCommissioner of Internal Revenue v. Procter and Gamble G.R. L-66838Dino Bernard LapitanNo ratings yet

- Commissioner of Internal Revenue v. GCL Retirement Plan G.R. 95022Document6 pagesCommissioner of Internal Revenue v. GCL Retirement Plan G.R. 95022Dino Bernard LapitanNo ratings yet

- CIR Vs Procter & GambleDocument44 pagesCIR Vs Procter & GambleDario G. TorresNo ratings yet

- Highlighted in Re Zialcita, AM No. 90-6-015-SC, Oct. 18, 1990.htmlDocument4 pagesHighlighted in Re Zialcita, AM No. 90-6-015-SC, Oct. 18, 1990.htmlCharity RomagaNo ratings yet

- Government employees' terminal leave pay tax exemption upheldDocument8 pagesGovernment employees' terminal leave pay tax exemption upheldAna GNo ratings yet

- 35intercontinental Broadcasting Corporation VDocument2 pages35intercontinental Broadcasting Corporation Vcrisanto perezNo ratings yet

- Banco de Oro vs RCBC dispute over tax treatment of PEACe BondsDocument64 pagesBanco de Oro vs RCBC dispute over tax treatment of PEACe BondsJesse Myl MarciaNo ratings yet

- CIR V Procter & GambleDocument12 pagesCIR V Procter & GambleParis LisonNo ratings yet

- PE Uniform - JPGDocument1 pagePE Uniform - JPGSalma GurarNo ratings yet

- Admissibility of Income Tax Returns in Court CasesDocument1 pageAdmissibility of Income Tax Returns in Court CasesSalma GurarNo ratings yet

- Petitioner Seeks Recovery of Shares Sold by ReceiverDocument4 pagesPetitioner Seeks Recovery of Shares Sold by ReceiverSalma GurarNo ratings yet

- Petitioner Seeks Recovery of Shares Sold by ReceiverDocument4 pagesPetitioner Seeks Recovery of Shares Sold by ReceiverSalma GurarNo ratings yet

- CIR Vs CADocument2 pagesCIR Vs CASalma GurarNo ratings yet

- 2004 Notarial RulesDocument11 pages2004 Notarial RulesSalma GurarNo ratings yet

- EAO UtilizationDocument1 pageEAO UtilizationSalma GurarNo ratings yet

- Legal EthicsDocument12 pagesLegal EthicsJoanna MandapNo ratings yet

- CIR Vs CADocument1 pageCIR Vs CASalma GurarNo ratings yet

- 2 Unjieng V PosadasDocument1 page2 Unjieng V PosadasSalma GurarNo ratings yet

- 2011 Annual Audit Report Part 3Document32 pages2011 Annual Audit Report Part 3Salma GurarNo ratings yet

- RP V City of DavaoDocument4 pagesRP V City of DavaoSalma GurarNo ratings yet

- Tax RatesDocument2 pagesTax RatesSalma GurarNo ratings yet

- Letters of Credit: Transfield Philippines v Luzon Hydro Electric Corp (2004Document5 pagesLetters of Credit: Transfield Philippines v Luzon Hydro Electric Corp (2004Salma GurarNo ratings yet

- Recover full value of sharesDocument5 pagesRecover full value of sharesSalma GurarNo ratings yet

- Public Lands Case DecidedDocument15 pagesPublic Lands Case DecidedSalma GurarNo ratings yet

- House ModelDocument1 pageHouse ModelSalma GurarNo ratings yet

- Natl-NGAS TableofContentsVol1Document8 pagesNatl-NGAS TableofContentsVol1janicasiaNo ratings yet

- Accountacy With CA Q.P.Document3 pagesAccountacy With CA Q.P.riyaskalpettaNo ratings yet

- Employee Motivation12th From Lic To MaheshDocument60 pagesEmployee Motivation12th From Lic To MaheshDachepally Praveen KumarNo ratings yet

- 6Document5 pages6Carlo ParasNo ratings yet

- Maxicare Digest Attach After Page 66Document1 pageMaxicare Digest Attach After Page 66twenty19 lawNo ratings yet

- Mock Exam AnswersDocument19 pagesMock Exam AnswersDixie CheeloNo ratings yet

- Solutions To Session 6 Practice ProblemsDocument3 pagesSolutions To Session 6 Practice ProblemsKeshav soodNo ratings yet

- Planning Front Office Operations ForecastDocument12 pagesPlanning Front Office Operations ForecastAshutosh SinghNo ratings yet

- SAP Cash Bank AccountingDocument5 pagesSAP Cash Bank AccountingHenrique BergerNo ratings yet

- OffentliggorelseDocument59 pagesOffentliggorelsenot youNo ratings yet

- Acc407 Test 2 Feb 2022 QQ (1) EpjjDocument6 pagesAcc407 Test 2 Feb 2022 QQ (1) EpjjShahrillNo ratings yet

- Dlonsod Case Digest Income TaxDocument11 pagesDlonsod Case Digest Income TaxRalph MondayNo ratings yet

- One Dividend Policy by An Organization - Team 2Document15 pagesOne Dividend Policy by An Organization - Team 2Aishwarya KulkarniNo ratings yet

- Introduction to Computing Lab #13Document4 pagesIntroduction to Computing Lab #13Muhammad FahadNo ratings yet

- CIR vs. La FlorDocument13 pagesCIR vs. La FlorKim RoqueNo ratings yet

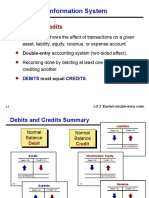

- Accounting Information System Debits and CreditsDocument84 pagesAccounting Information System Debits and CreditsDavid Bradley BeckNo ratings yet

- DO - 029 - S2011 Revised Guidelines On Preparation of ABCDocument6 pagesDO - 029 - S2011 Revised Guidelines On Preparation of ABCroldskiNo ratings yet

- Foreign Exchange Investment Department Bangladesh Bank Head Office DhakaDocument2 pagesForeign Exchange Investment Department Bangladesh Bank Head Office Dhakamirmuiz2993No ratings yet

- What Is The Money MarketDocument22 pagesWhat Is The Money MarketMuhammad HasnainNo ratings yet

- IT Act With Master Guide To Income Tax ActDocument22 pagesIT Act With Master Guide To Income Tax ActManoj RaghavNo ratings yet

- Ar2015 EngDocument234 pagesAr2015 EngKen ChiaNo ratings yet

- Westchester Overtime Costs MillionsDocument2 pagesWestchester Overtime Costs MillionsGerald McKinstryNo ratings yet

- Circular Flow of Income &Document40 pagesCircular Flow of Income &Kunal Uddhavrao GaradNo ratings yet

- Project Document OF The Asian Infrastructure Investment BankDocument51 pagesProject Document OF The Asian Infrastructure Investment BankVishal DaveNo ratings yet

- JBE Accounting Case AnalysisDocument8 pagesJBE Accounting Case AnalysisTaufan PutraNo ratings yet