You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Invesment WisdomDocument2 pagesInvesment WisdomSajid BalochNo ratings yet

- AppGuide NSNP NSDEE English PDFDocument32 pagesAppGuide NSNP NSDEE English PDFSajid BalochNo ratings yet

- PIBT Information Memorandum PDFDocument23 pagesPIBT Information Memorandum PDFSajid BalochNo ratings yet

- Pattern of Shareholdings PDFDocument2 pagesPattern of Shareholdings PDFSajid BalochNo ratings yet

- Annual Report 2016 PDFDocument112 pagesAnnual Report 2016 PDFSajid BalochNo ratings yet

- Annual Accounts 2009 PDFDocument71 pagesAnnual Accounts 2009 PDFSajid BalochNo ratings yet

- Annual Report 2017 PDFDocument96 pagesAnnual Report 2017 PDFSajid BalochNo ratings yet

- CDC ChargesDocument1 pageCDC ChargesSajid BalochNo ratings yet

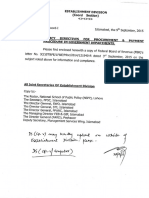

- FBR-Policy Directives For Procurement and Payment Procedure in Government DepartmentsDocument3 pagesFBR-Policy Directives For Procurement and Payment Procedure in Government DepartmentsSajid BalochNo ratings yet

- ISCO Tax Card TY 2016 FinalDocument13 pagesISCO Tax Card TY 2016 FinalAtteique AnwarNo ratings yet

- Section 153Document1 pageSection 153Sajid BalochNo ratings yet

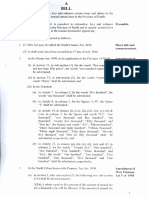

- Sindh Finance Bill 2016aDocument8 pagesSindh Finance Bill 2016aSajid BalochNo ratings yet

- Budget Analysis Report June 07Document27 pagesBudget Analysis Report June 07Sajid BalochNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Culture AuditDocument12 pagesCulture AuditBharath MenonNo ratings yet

- ENT Business Plan 07122022 121053pmDocument56 pagesENT Business Plan 07122022 121053pmAreej IftikharNo ratings yet

- YASHDocument15 pagesYASHyashNo ratings yet

- Cutover Strategy in SAP FICO PDFDocument6 pagesCutover Strategy in SAP FICO PDFkkka TtNo ratings yet

- Acknowledgements: Indo-Austrian Trade & Scope For Investment Opportunities 1Document52 pagesAcknowledgements: Indo-Austrian Trade & Scope For Investment Opportunities 1arun1974No ratings yet

- Indonesia EDocument8 pagesIndonesia EAghla AmwalanaNo ratings yet

- Best Buy Usa OriginalllDocument1 pageBest Buy Usa OriginalllmedNo ratings yet

- Step 3.4 Partnerships and Partnership Management: Resources For Implementing The WWF Project & Programme StandardsDocument19 pagesStep 3.4 Partnerships and Partnership Management: Resources For Implementing The WWF Project & Programme StandardsShanonraj KhadkaNo ratings yet

- Event GuideDocument58 pagesEvent GuideBach Tran100% (2)

- Organizationa Behaviour: An Introductory TextDocument8 pagesOrganizationa Behaviour: An Introductory TextNguyễn Bích KhuêNo ratings yet

- F&B in Shopping MallsDocument4 pagesF&B in Shopping MallsAbdellah EssonniNo ratings yet

- COMPANY A - BPM Assessment - Final PDFDocument35 pagesCOMPANY A - BPM Assessment - Final PDFhussein jardali100% (1)

- Anil Sharma ResumeDocument4 pagesAnil Sharma ResumeAnnil SharmaNo ratings yet

- The Decline of American Capitalism (1934)Document517 pagesThe Decline of American Capitalism (1934)antoniojoseespNo ratings yet

- Managerial Economics in A Global Economy, 5th Edition by Dominick SalvatoreDocument18 pagesManagerial Economics in A Global Economy, 5th Edition by Dominick SalvatoreChi7inNo ratings yet

- Orange Wine ProductionDocument41 pagesOrange Wine ProductionDagobert R. Le Grand50% (2)

- Draft SubmissionDocument8 pagesDraft SubmissionEthan HuntNo ratings yet

- Cost Breakup of Indian Ride Sharing CabsDocument3 pagesCost Breakup of Indian Ride Sharing CabsNNS RohitNo ratings yet

- KasusDocument4 pagesKasusTry DharsanaNo ratings yet

- Dell Inc: By-Group 8 Surbhi Swarnim Swati VivekDocument13 pagesDell Inc: By-Group 8 Surbhi Swarnim Swati VivekDicky FirmansyahNo ratings yet

- Role of Young EntrepreneursDocument8 pagesRole of Young EntrepreneursanilambicaNo ratings yet

- Guinness 6th EdDocument2 pagesGuinness 6th Edachikungu2225No ratings yet

- Functions of Commercial BanksDocument52 pagesFunctions of Commercial BanksPulkit_Saini_789No ratings yet

- Woodsmith 239 PDFDocument68 pagesWoodsmith 239 PDFdomingo figueroa100% (2)

- Bsp-Credit Risk ManagementDocument69 pagesBsp-Credit Risk Managementjhomar jadulanNo ratings yet

- 23A ECON 1194 Assignment 2Document2 pages23A ECON 1194 Assignment 2Nhu NgocNo ratings yet

- Quantity Estimation & Construction Management (Book)Document273 pagesQuantity Estimation & Construction Management (Book)Adarsh RathoreNo ratings yet

- imageRUNNER+ADVANCE 4200 BrochureDocument12 pagesimageRUNNER+ADVANCE 4200 BrochureMc_KeaneNo ratings yet

- San Bernardino Bondholders Vs CalpersDocument114 pagesSan Bernardino Bondholders Vs Calpersjon_ortizNo ratings yet

- SAP FICO NotesDocument39 pagesSAP FICO NotesShivaniNo ratings yet