You might also like

- Schaum's Outline of Basic Business Mathematics, 2edFrom EverandSchaum's Outline of Basic Business Mathematics, 2edRating: 5 out of 5 stars5/5 (1)

- Exercises and Answers Chapter 5Document8 pagesExercises and Answers Chapter 5MerleNo ratings yet

- DCF TakeawaysDocument2 pagesDCF TakeawaysvrkasturiNo ratings yet

- Projects SolutionsDocument81 pagesProjects SolutionsMd Miraz100% (1)

- Financial Statement Analysis and Security Valuation Solutions Chapter 6Document6 pagesFinancial Statement Analysis and Security Valuation Solutions Chapter 6Mia Greene100% (1)

- Nike Inc - Cost of Capital - Syndicate 10Document16 pagesNike Inc - Cost of Capital - Syndicate 10Anthony KwoNo ratings yet

- Principles of Cash Flow Valuation: An Integrated Market-Based ApproachFrom EverandPrinciples of Cash Flow Valuation: An Integrated Market-Based ApproachRating: 3 out of 5 stars3/5 (3)

- Distribution Network of NestleDocument26 pagesDistribution Network of Nestlemattogill100% (6)

- Business Plan On Fruits and Vegetable Supply ChainDocument27 pagesBusiness Plan On Fruits and Vegetable Supply ChainKishan Tank85% (165)

- Audit and Internal ReviewDocument5 pagesAudit and Internal ReviewkhengmaiNo ratings yet

- Sampa VideoDocument24 pagesSampa VideodoiNo ratings yet

- Free Book On Basic Financial ModellingDocument100 pagesFree Book On Basic Financial ModellingCareer and TechnologyNo ratings yet

- SolutionMINI CASEThe Leveraged Buyout of Cheek ProductsDocument4 pagesSolutionMINI CASEThe Leveraged Buyout of Cheek ProductsEfri Dwiyanto100% (2)

- FINAN204-21A - Tutorial 7 Week 10Document6 pagesFINAN204-21A - Tutorial 7 Week 10Danae YangNo ratings yet

- Concept Questions: Chapter Five Accrual Accounting and Valuation: Pricing Book ValuesDocument41 pagesConcept Questions: Chapter Five Accrual Accounting and Valuation: Pricing Book Valuesaqiilah subrotoNo ratings yet

- Concept Questions: Chapter Five Accrual Accounting and Valuation: Pricing Book ValuesDocument41 pagesConcept Questions: Chapter Five Accrual Accounting and Valuation: Pricing Book Valuesamina_alsayegh50% (2)

- SEx 5Document44 pagesSEx 5Amir Madani100% (3)

- Assignment 4Document6 pagesAssignment 4Oktami IndriyaniNo ratings yet

- Question 1Document8 pagesQuestion 1elvitaNo ratings yet

- Quiz 1 Practice ProblemsDocument8 pagesQuiz 1 Practice ProblemsUmaid FaisalNo ratings yet

- DCF ExamplesDocument7 pagesDCF Examplesarti guptaNo ratings yet

- Sampa Video G3 - SecBDocument3 pagesSampa Video G3 - SecBEina GuptaNo ratings yet

- BANK3011 Workshop Week 4 SolutionsDocument5 pagesBANK3011 Workshop Week 4 SolutionsZahraaNo ratings yet

- Solution To Practice Exercise Set 1: B8110, Fall 2009Document10 pagesSolution To Practice Exercise Set 1: B8110, Fall 2009Aasrith KandulaNo ratings yet

- Solution To Self-Study Exercise 4Document6 pagesSolution To Self-Study Exercise 4chanNo ratings yet

- Sol3ch6 RevDocument49 pagesSol3ch6 RevSonyaTanSiYing100% (1)

- Solution To Self-Study Exercise 3Document4 pagesSolution To Self-Study Exercise 3chanNo ratings yet

- SMChap 006Document22 pagesSMChap 006Anonymous mKjaxpMaLNo ratings yet

- Exam1 Solutions 40610 2008Document7 pagesExam1 Solutions 40610 2008JordanNo ratings yet

- Chapter 7 Prospective Analysis: Valuation Theory and ConceptsDocument7 pagesChapter 7 Prospective Analysis: Valuation Theory and ConceptsWalm KetyNo ratings yet

- Ankush - Gupta - Financial Management and Valuation - MBA - DBF - DEC - 2020 - Word FileDocument8 pagesAnkush - Gupta - Financial Management and Valuation - MBA - DBF - DEC - 2020 - Word FileAnkush GuptaNo ratings yet

- Cost of CapitalDocument24 pagesCost of CapitalShubham PariharNo ratings yet

- Accrual Accounting and Valuation: Pricing Book ValuesDocument46 pagesAccrual Accounting and Valuation: Pricing Book ValuesNancy Howard100% (1)

- Week 6 Assignment Part 2 (Empty)Document11 pagesWeek 6 Assignment Part 2 (Empty)adomahattafuahNo ratings yet

- Equity Valuation Assignment Chapter 7Document7 pagesEquity Valuation Assignment Chapter 7mehandiNo ratings yet

- Sampa VideoDocument24 pagesSampa Videopawangadiya1210No ratings yet

- Busi 331 Project 1 Marking Guide: HandbookDocument28 pagesBusi 331 Project 1 Marking Guide: HandbookDilrajSinghNo ratings yet

- 04 - Tutorial 4 - Week 6 SolutionsDocument8 pages04 - Tutorial 4 - Week 6 SolutionsJason ChowNo ratings yet

- 5 Solution Maf302Document6 pages5 Solution Maf302diana.p7reiraNo ratings yet

- Trial 1 - DominionDocument17 pagesTrial 1 - Dominionelenasalvazia9No ratings yet

- New Lecture 10 SPR 09Document11 pagesNew Lecture 10 SPR 09bat0oNo ratings yet

- Residual IncomeDocument5 pagesResidual IncomeLH0% (1)

- ACME Prob - 04-01Document6 pagesACME Prob - 04-01srutijnpNo ratings yet

- What Is More Valuable - (A) Taka 1,50,000 Per Year For Ever or (B) An Annuity of Taka 2,80,000 For 4 Years? Annual Rate Is 20 PercentDocument24 pagesWhat Is More Valuable - (A) Taka 1,50,000 Per Year For Ever or (B) An Annuity of Taka 2,80,000 For 4 Years? Annual Rate Is 20 Percentafsana zoyaNo ratings yet

- Midterm - Solutions 1) Theoretical QuestionsDocument4 pagesMidterm - Solutions 1) Theoretical QuestionsMarcos CachuloNo ratings yet

- Solutions To Exam Financial Statement Analysis June 23, 2011Document8 pagesSolutions To Exam Financial Statement Analysis June 23, 2011BuketNo ratings yet

- Ratio Analysis Case Study SolutionDocument7 pagesRatio Analysis Case Study SolutionRanjuNo ratings yet

- FCFE and FCFF Model SessionDocument25 pagesFCFE and FCFF Model SessionABHIJEET BHUNIA MBA 2021-23 (Delhi)No ratings yet

- Cv. Chapter 5Document23 pagesCv. Chapter 5VidhiNo ratings yet

- Chapter 4: Risk Measurement and Hurdle Rates in PracticeDocument10 pagesChapter 4: Risk Measurement and Hurdle Rates in PracticeOsama bin adnanNo ratings yet

- Capital StructureDocument17 pagesCapital StructuresaifNo ratings yet

- Lbo Case StudyDocument6 pagesLbo Case StudyRishabh MishraNo ratings yet

- Ejercicio Nro 8 SolucionnnnnnDocument9 pagesEjercicio Nro 8 SolucionnnnnnSugar Leonardo Herrera CoaquiraNo ratings yet

- APV and EVA Approach of Firm Valuation Module 8 (Class 37 and 38)Document23 pagesAPV and EVA Approach of Firm Valuation Module 8 (Class 37 and 38)Vineet AgarwalNo ratings yet

- APV and EVA Approach of Firm Valuation Module 8 (Class 37 and 38)Document23 pagesAPV and EVA Approach of Firm Valuation Module 8 (Class 37 and 38)Vineet AgarwalNo ratings yet

- LBO Valuation - Working File CV2Document5 pagesLBO Valuation - Working File CV2Ayushi GuptaNo ratings yet

- 23 Nov 2018 Mixed Questions With Solutions PDFDocument9 pages23 Nov 2018 Mixed Questions With Solutions PDFLaston MilanziNo ratings yet

- Seminar 3 N1591 - MCK Chap 8 QuestionsDocument4 pagesSeminar 3 N1591 - MCK Chap 8 QuestionsMandeep SNo ratings yet

- Chapter 9. Tool Kit For The Cost of CapitalDocument14 pagesChapter 9. Tool Kit For The Cost of CapitalasimqaiserNo ratings yet

- Mid Test SolutionDocument5 pagesMid Test SolutionHương Phạm MaiNo ratings yet

- 13 - Discounted Cash Flow Techniques (Part 1)Document7 pages13 - Discounted Cash Flow Techniques (Part 1)ayushagarwal23No ratings yet

- Business Valuation ModelDocument14 pagesBusiness Valuation Modeldagagovind7No ratings yet

- Personal Money Management Made Simple with MS Excel: How to save, invest and borrow wiselyFrom EverandPersonal Money Management Made Simple with MS Excel: How to save, invest and borrow wiselyNo ratings yet

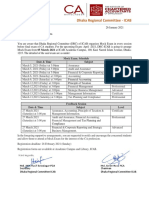

- Dhaka Regional Committee - ICAB: Mock Exam. Schedule Date & Time Subject LevelDocument1 pageDhaka Regional Committee - ICAB: Mock Exam. Schedule Date & Time Subject LevelMd MirazNo ratings yet

- VAT Mock Exam Time 2 Hours Marks 60: Prepared by Snehasish Barua, FCADocument3 pagesVAT Mock Exam Time 2 Hours Marks 60: Prepared by Snehasish Barua, FCAMd MirazNo ratings yet

- 3 Business Finance Questions Nov Dec 2019 CLDocument2 pages3 Business Finance Questions Nov Dec 2019 CLMd Miraz0% (1)

- Advanced Level 2021Document2 pagesAdvanced Level 2021Md MirazNo ratings yet

- 3 Business Finance Questions Nov Dec 2019 CLDocument2 pages3 Business Finance Questions Nov Dec 2019 CLMd Miraz0% (1)

- Prohibition of Beneficial Owners Trade Rule 1995Document6 pagesProhibition of Beneficial Owners Trade Rule 1995Reefat HasanNo ratings yet

- Tax Compliances Day 4Document15 pagesTax Compliances Day 4Md MirazNo ratings yet

- Evaluating Performance - Chapter 12Document10 pagesEvaluating Performance - Chapter 12Md MirazNo ratings yet

- Tax Compliances Day 4Document15 pagesTax Compliances Day 4Md MirazNo ratings yet

- Corporate Gov PDFDocument1 pageCorporate Gov PDFMd MirazNo ratings yet

- Capiatal Budgeting Analysis 12.8Document4 pagesCapiatal Budgeting Analysis 12.8Md MirazNo ratings yet

- 2.IAS 39 Financial Instruments Rec and Meas - SELKDocument43 pages2.IAS 39 Financial Instruments Rec and Meas - SELKVher Ducay100% (1)

- AIS09Document45 pagesAIS09Azhar UddinNo ratings yet

- Previous LiteratureDocument1 pagePrevious LiteratureMd MirazNo ratings yet

- U V J Ucyj E Wë: Mycörvzš¿X Evsjv 'K Mikvi Cöv - WGK WK V Awa'ßiDocument28 pagesU V J Ucyj E Wë: Mycörvzš¿X Evsjv 'K Mikvi Cöv - WGK WK V Awa'ßiMd MirazNo ratings yet

- Previous LiteratureDocument1 pagePrevious LiteratureMd MirazNo ratings yet

- Microsoft Word Shortcut Keys PDFDocument5 pagesMicrosoft Word Shortcut Keys PDFMd MirazNo ratings yet

- NunDocument33 pagesNunMd MirazNo ratings yet

- Capiatal Budgeting Analysis 12.8Document4 pagesCapiatal Budgeting Analysis 12.8Md MirazNo ratings yet

- #Love - Pixel - B - Hash Tags - Deskgram PDFDocument10 pages#Love - Pixel - B - Hash Tags - Deskgram PDFMd MirazNo ratings yet

- Jamil Sir Presentation SamplingDocument47 pagesJamil Sir Presentation SamplingMd MirazNo ratings yet

- Previous LiteratureDocument1 pagePrevious LiteratureMd MirazNo ratings yet

- Smart Box On The GoDocument52 pagesSmart Box On The GoNaimul Haque NayeemNo ratings yet

- Case Study - Bax Container Limited: Superior TechnologyDocument18 pagesCase Study - Bax Container Limited: Superior TechnologyMd MirazNo ratings yet

- Mohammad Al-Amin RashidDocument64 pagesMohammad Al-Amin RashidMd MirazNo ratings yet

- Instructions !!!Document1 pageInstructions !!!Al EneNo ratings yet

- Basic Ali 2009 PDFDocument101 pagesBasic Ali 2009 PDFMd MirazNo ratings yet

- Parmalatfinalpresentation 170717010056Document15 pagesParmalatfinalpresentation 170717010056Md MirazNo ratings yet

- Our Adwords Proposal: Passionate About Helping Small Businesses Excel Through Paid SearchDocument7 pagesOur Adwords Proposal: Passionate About Helping Small Businesses Excel Through Paid SearchASWT PlasticsNo ratings yet

- Scalable Capital ISA GuideDocument15 pagesScalable Capital ISA Guidenitind_kNo ratings yet

- This Is RealDocument17 pagesThis Is RealCheemee LiuNo ratings yet

- Typologies of E-TourismDocument18 pagesTypologies of E-Tourismsubbu2raj3372No ratings yet

- Media-Planning Solved MCQs (Set-2)Document8 pagesMedia-Planning Solved MCQs (Set-2)PARTH MANJREKARNo ratings yet

- SDLCDocument5 pagesSDLCShaira SalandaNo ratings yet

- Edelman Copy FINAL Flipkart Pay Later Now Available On PhonePeDocument2 pagesEdelman Copy FINAL Flipkart Pay Later Now Available On PhonePeArbaz KhanNo ratings yet

- Worksheet FABM2 Q1 M2 2 SCI Multi-StepDocument3 pagesWorksheet FABM2 Q1 M2 2 SCI Multi-StepMarjun AbogNo ratings yet

- BUS227Document70 pagesBUS227Dauda AdijatNo ratings yet

- Cost Accounting Mcqs PDFDocument31 pagesCost Accounting Mcqs PDFநானும்நீயும்No ratings yet

- FinAcc2 Tut102Document177 pagesFinAcc2 Tut102Caladan RakeNo ratings yet

- FIN 521 Finance For Managers Syllabus Fall 2016Document6 pagesFIN 521 Finance For Managers Syllabus Fall 2016Ahmed SecunovicNo ratings yet

- QuestionnaireDocument5 pagesQuestionnaireRiyaNo ratings yet

- Chapter 3 & 4 - Putu Rian Arde SuryaDocument4 pagesChapter 3 & 4 - Putu Rian Arde SuryaRian Arde SuryaNo ratings yet

- St. Vincent'S College Incorporated: WWW - Svc.edu - PH Svci - 1917@svc - Edu.phDocument8 pagesSt. Vincent'S College Incorporated: WWW - Svc.edu - PH Svci - 1917@svc - Edu.phGeorey PaglinawanNo ratings yet

- Solution Chapter 7Document26 pagesSolution Chapter 7Roselle Manlapaz LorenzoNo ratings yet

- Ias & IfrsDocument7 pagesIas & IfrsAsiful IslamNo ratings yet

- Points Earned: Correct Answer(s) : D: Reference: 12-19Document15 pagesPoints Earned: Correct Answer(s) : D: Reference: 12-19RiaNo ratings yet

- Understanding The Time Value of MoneyDocument5 pagesUnderstanding The Time Value of Moneygeneration.m31989No ratings yet

- UFO Fondue Marketing PlanDocument15 pagesUFO Fondue Marketing PlanTee Nick VannNo ratings yet

- ACC211 Week 4-5 SIMDocument22 pagesACC211 Week 4-5 SIMIvan Pacificar BioreNo ratings yet

- Revision Pack 4 May 2011Document27 pagesRevision Pack 4 May 2011Lim Hui SinNo ratings yet

- Customer Information FORMDocument1 pageCustomer Information FORMEniger CaspeNo ratings yet

- Process Costing - Lecture NotesDocument11 pagesProcess Costing - Lecture NotesOtenyo MeshackNo ratings yet

- Exp19 Excel Ch03 Cap GymDocument6 pagesExp19 Excel Ch03 Cap GymParth PatelNo ratings yet

- Management AccountingDocument10 pagesManagement Accountingnikhilgangwani100% (3)

- Unit 5Document6 pagesUnit 5CaptainVipro YTNo ratings yet

- SCLT 6318 AssignmentDocument3 pagesSCLT 6318 AssignmentRamitha DabareNo ratings yet