You might also like

- Executive Order No. 125-ADocument7 pagesExecutive Order No. 125-ALR FNo ratings yet

- Reorganizing Philippines Ministry of Transportation and CommunicationsDocument13 pagesReorganizing Philippines Ministry of Transportation and CommunicationsLR FNo ratings yet

- Quitclaim Affidavit ReleaseDocument2 pagesQuitclaim Affidavit ReleaseLR FNo ratings yet

- Rules Implementing Code of Conduct for Public OfficialsDocument18 pagesRules Implementing Code of Conduct for Public OfficialsicebaguilatNo ratings yet

- Eo 93Document2 pagesEo 93LR FNo ratings yet

- Begun and Held Metro Manila, On Monday, The Twerity Third of July, T W o Thousand SevenDocument33 pagesBegun and Held Metro Manila, On Monday, The Twerity Third of July, T W o Thousand SevenSusielyn Anne Tumamao AngobungNo ratings yet

- IRR of RA 9295 2014 Amendments - Domestic Shipping Development ActDocument42 pagesIRR of RA 9295 2014 Amendments - Domestic Shipping Development ActIrene Balmes-LomibaoNo ratings yet

- Executive Order No. 109Document3 pagesExecutive Order No. 109Ian HatolNo ratings yet

- Opening Water Transport IndustryDocument6 pagesOpening Water Transport IndustryLR FNo ratings yet

- Deposit Refund Agreement (Template)Document2 pagesDeposit Refund Agreement (Template)LR FNo ratings yet

- 2014-2017 Bar TaxationDocument41 pages2014-2017 Bar TaxationLR F0% (1)

- Affidavit Change Color Motor VehicleDocument1 pageAffidavit Change Color Motor VehicleLR FNo ratings yet

- Torts Civil Liability in Criminal CasesDocument2 pagesTorts Civil Liability in Criminal CasesLR FNo ratings yet

- PALE Current Judicial Ethics CasesDocument52 pagesPALE Current Judicial Ethics CasesLR F100% (1)

- Affidavit of Loss of PassportDocument1 pageAffidavit of Loss of PassportPlan Can JoxNo ratings yet

- Affidavit of Loss Not For SaleDocument1 pageAffidavit of Loss Not For SaleLR FNo ratings yet

- Canons 17-19 CasesDocument33 pagesCanons 17-19 CasesLR FNo ratings yet

- Special Proceedingss Habeas Corpus BarDocument3 pagesSpecial Proceedingss Habeas Corpus BarLR FNo ratings yet

- Villanueva Vs DomingoDocument8 pagesVillanueva Vs Domingozpuse_wtpNo ratings yet

- Transportation Law Case DigestDocument38 pagesTransportation Law Case DigestLR FNo ratings yet

- Taxation Cases 2bDocument130 pagesTaxation Cases 2bLR FNo ratings yet

- LMC - Boundary Dispute CasesDocument12 pagesLMC - Boundary Dispute CasesLR FNo ratings yet

- Sales Civil Law Memory AidDocument4 pagesSales Civil Law Memory AidLR FNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument7 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledLR FNo ratings yet

- San Beda College of LawDocument36 pagesSan Beda College of LawVladimir ReyesNo ratings yet

- Legal Medicine-Judicial-AffidavitDocument10 pagesLegal Medicine-Judicial-AffidavitLR FNo ratings yet

- Ra 7160 IrrDocument263 pagesRa 7160 IrrAlvaro Garingo100% (21)

- Sales Civil Law Memory AidDocument4 pagesSales Civil Law Memory AidLR FNo ratings yet

- Supreme Court decisions on effect and application of lawsDocument65 pagesSupreme Court decisions on effect and application of lawsAmicus CuriaeNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Expedited customs procedures for express shipmentsDocument10 pagesExpedited customs procedures for express shipmentsRafael JuicoNo ratings yet

- CIR V PASRCDocument9 pagesCIR V PASRCJENNY BUTACANNo ratings yet

- Customs Bonded Warehouse RulesDocument2 pagesCustoms Bonded Warehouse RulesJoshua BasilioNo ratings yet

- Contribution of Customs Information System to Customs Department PerformanceDocument54 pagesContribution of Customs Information System to Customs Department PerformanceSt. Lawrence University SLAUNo ratings yet

- Wolkite University College of Social Sciences and Humanities Department of Governance and Development Studies Challenges and ProspectsDocument41 pagesWolkite University College of Social Sciences and Humanities Department of Governance and Development Studies Challenges and ProspectsSefa MisebahNo ratings yet

- Glossary of International Freight TermsDocument27 pagesGlossary of International Freight TermsAnand Khisti.100% (4)

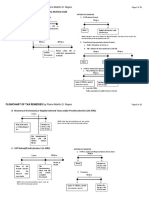

- Flowchart of Tax Remedies I. Remedies UnDocument12 pagesFlowchart of Tax Remedies I. Remedies UnKevin Ken Sison Ganchero100% (2)

- Bringing Tobacco Back From The Foreigner: You Come Back From A European Union CountryDocument5 pagesBringing Tobacco Back From The Foreigner: You Come Back From A European Union CountryHappy PrinceNo ratings yet

- Oring PerformanceDocument66 pagesOring Performancefake fNo ratings yet

- What Customs Manual Says About Disposal of Unclaimed and Uncleared CargoDocument3 pagesWhat Customs Manual Says About Disposal of Unclaimed and Uncleared CargoCM AngNo ratings yet

- BIR RulingDocument3 pagesBIR RulingyakyakxxNo ratings yet

- U.S. Customs Form: CBP Form 442 - Application For Exemption From Special Landing RequirementsDocument3 pagesU.S. Customs Form: CBP Form 442 - Application For Exemption From Special Landing RequirementsCustoms FormsNo ratings yet

- Chapter I: Provisional Assessment: 1.1 HighlightsDocument22 pagesChapter I: Provisional Assessment: 1.1 HighlightsrajaNo ratings yet

- Receipt BookingDocument1 pageReceipt BookingFR ChannelNo ratings yet

- SIMS Exim ManagementDocument56 pagesSIMS Exim ManagementRounaq DharNo ratings yet

- Foreign Trade Policy (2015-2020)Document17 pagesForeign Trade Policy (2015-2020)Neha RawalNo ratings yet

- How To Use Import Export InformationDocument3 pagesHow To Use Import Export InformationTSEDEKENo ratings yet

- GST Impact On Indian Textile IndustryDocument33 pagesGST Impact On Indian Textile IndustryHarsh Gautam100% (6)

- Crew Declaration: Approved Form Customs Act 1901 Section 71AAABDocument1 pageCrew Declaration: Approved Form Customs Act 1901 Section 71AAABPaul mulderNo ratings yet

- ThesiscipcbfrevisedDocument16 pagesThesiscipcbfrevisedJannah Sanguenza Montero100% (1)

- EouDocument12 pagesEouRuby SinghNo ratings yet

- WarehousingDocument9 pagesWarehousingVarun ModiNo ratings yet

- My FormatDocument13 pagesMy FormatNedu Iyida0% (1)

- JhdsjkduijhsbsgdDocument4 pagesJhdsjkduijhsbsgdRanvidsNo ratings yet

- YaokasinDocument6 pagesYaokasinEdward Marc P. JovellanosNo ratings yet

- CA Final 40 Days Revision Program For DT IDTDocument5 pagesCA Final 40 Days Revision Program For DT IDTMala M PrasannaNo ratings yet

- Tax Cases 2Document146 pagesTax Cases 2Sylver JanNo ratings yet

- Mock Test August 2018Document5 pagesMock Test August 2018Suzhana The WizardNo ratings yet

- BRIEF HISTORICAL VIEW OF MODERN TAX ADMINISTRATION IN ALBANIA, 1994-2011 - AL-TaxDocument3 pagesBRIEF HISTORICAL VIEW OF MODERN TAX ADMINISTRATION IN ALBANIA, 1994-2011 - AL-TaxEduart GjokutajNo ratings yet

- Bangladesh Case StudyDocument42 pagesBangladesh Case StudyTasmiaNo ratings yet