You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Advanced Competitive Position AssignmentDocument7 pagesAdvanced Competitive Position AssignmentGeraldine Aguilar100% (1)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- BBA Semester III Project (Marketing Strategy) BritanniaDocument65 pagesBBA Semester III Project (Marketing Strategy) BritanniaWe Rocks100% (1)

- Din 11864 / Din 11853: Armaturenwerk Hötensleben GMBHDocument70 pagesDin 11864 / Din 11853: Armaturenwerk Hötensleben GMBHkrisNo ratings yet

- Sample of Memorandum of Agreement (MOA)Document12 pagesSample of Memorandum of Agreement (MOA)Johanna BelestaNo ratings yet

- Final QARSHI REPORTDocument31 pagesFinal QARSHI REPORTUzma Khan100% (2)

- The East Pacific Merchandising Corporation vs. The Director of Patents and Luis P. PellicerDocument31 pagesThe East Pacific Merchandising Corporation vs. The Director of Patents and Luis P. PellicerRalph HonoricoNo ratings yet

- SynopsisDocument12 pagesSynopsisNikhil JainNo ratings yet

- Annotated Glossary of Terms Used in The Economic Analysis of Agricultural ProjectsDocument140 pagesAnnotated Glossary of Terms Used in The Economic Analysis of Agricultural ProjectsMaria Ines Castelluccio100% (1)

- Law Firms List 2Document13 pagesLaw Firms List 2Reena ShauNo ratings yet

- EJBDocument160 pagesEJBAnkit Jain100% (1)

- Alok Kumar Singh Section C WAC I 3Document7 pagesAlok Kumar Singh Section C WAC I 3Alok SinghNo ratings yet

- Ias 2Document29 pagesIas 2MK RKNo ratings yet

- 73 220 Lecture07Document10 pages73 220 Lecture07api-26315128No ratings yet

- Save Capitalism From CapitalistsDocument20 pagesSave Capitalism From CapitalistsLill GalilNo ratings yet

- Six Sigma Black Belt Wk1 Define Amp MeasureDocument451 pagesSix Sigma Black Belt Wk1 Define Amp Measuremajid4uonly100% (1)

- GL 003 14 Code of Good Practice For Life InsuranceDocument19 pagesGL 003 14 Code of Good Practice For Life InsuranceAdrian BehNo ratings yet

- Exemption Certificate - SalesDocument2 pagesExemption Certificate - SalesExecutive F&ADADUNo ratings yet

- Guide To Importing in ZimbabweDocument22 pagesGuide To Importing in ZimbabweMandla DubeNo ratings yet

- MARK977 Research For Marketing Decisions Autumn Semester, 2017 Week 8Document54 pagesMARK977 Research For Marketing Decisions Autumn Semester, 2017 Week 8Soumia HandouNo ratings yet

- SAP InvoiceDocument86 pagesSAP InvoicefatherNo ratings yet

- All Bom HC CircularsDocument55 pagesAll Bom HC CircularsSkk IrisNo ratings yet

- Section 114-118Document8 pagesSection 114-118ReiZen UelmanNo ratings yet

- SAP ResumeDocument4 pagesSAP ResumesriabcNo ratings yet

- Financial Accounting AssignmentDocument11 pagesFinancial Accounting AssignmentMadhawa RanawakeNo ratings yet

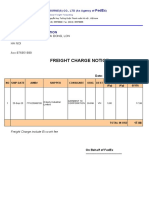

- Freight Charge Notice: To: Garment 10 CorporationDocument4 pagesFreight Charge Notice: To: Garment 10 CorporationThuy HoangNo ratings yet

- Part & Process Audit: Summary: General Supplier InformationDocument20 pagesPart & Process Audit: Summary: General Supplier InformationNeumar Neumann100% (1)

- The CEO Report v2 PDFDocument36 pagesThe CEO Report v2 PDFplanet_o100% (1)

- Lean Production SystemDocument8 pagesLean Production SystemRoni Komarul HayatNo ratings yet

- Upload 1 - Heirs of Tan Eng Kee v. CADocument4 pagesUpload 1 - Heirs of Tan Eng Kee v. CAPatricia VillamilNo ratings yet

- Report On Credit Appraisal in PNBDocument76 pagesReport On Credit Appraisal in PNBSanchit GoyalNo ratings yet