You might also like

- How to Get Funding For Your New Product IdeaFrom EverandHow to Get Funding For Your New Product IdeaRating: 4.5 out of 5 stars4.5/5 (6)

- Digital Marketing Agency Business Plan ExampleDocument31 pagesDigital Marketing Agency Business Plan ExampleShafique Ur RehmanNo ratings yet

- Upmetrics Business Plan TemplateDocument30 pagesUpmetrics Business Plan TemplateVTS Internal1No ratings yet

- Finance Case Study For Tech Startup Video.01Document10 pagesFinance Case Study For Tech Startup Video.01koenigNo ratings yet

- Partnership Dissolution - 2Document27 pagesPartnership Dissolution - 2Trisha GarciaNo ratings yet

- Gift Shop Business Plan ExampleDocument36 pagesGift Shop Business Plan ExampleAmaizing Wooden CraftNo ratings yet

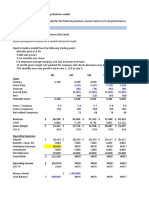

- Sample Financial ModelDocument69 pagesSample Financial ModelfoosaaNo ratings yet

- 12 Digital MarketingDocument28 pages12 Digital MarketingShabNo ratings yet

- Photography Business Plan ExampleDocument27 pagesPhotography Business Plan ExampleIbrahim RishadNo ratings yet

- Related Psas: Psa 700, 710, 720, 560, 570,: Auditing TheoryDocument13 pagesRelated Psas: Psa 700, 710, 720, 560, 570,: Auditing TheoryMay RamosNo ratings yet

- Paper LBO Model Example - Street of WallsDocument6 pagesPaper LBO Model Example - Street of WallsAndrewNo ratings yet

- EMI Group PLC Case Study Report: CFIN-522: Applied Topics: Corporate FinanceDocument11 pagesEMI Group PLC Case Study Report: CFIN-522: Applied Topics: Corporate FinanceJauhari WicaksonoNo ratings yet

- How To Purchase A Profitable Youtube Channel That Pays You For YearsDocument18 pagesHow To Purchase A Profitable Youtube Channel That Pays You For YearsWajahat Mazhar100% (1)

- Payday Loan Business Plan ExampleDocument23 pagesPayday Loan Business Plan ExampleJoseph Bwalya Mucheleka100% (1)

- Atlassian Roadshow Pitch Deck Draft - November 2015 - COMPLETE DECK - FINALDocument48 pagesAtlassian Roadshow Pitch Deck Draft - November 2015 - COMPLETE DECK - FINALTechCrunch100% (1)

- AdRoll Ultimate Guide To Building A Digital Brand WorkbookDocument55 pagesAdRoll Ultimate Guide To Building A Digital Brand WorkbookQuan Péron100% (1)

- Kandidate Hiring For GrowthDocument18 pagesKandidate Hiring For Growthjglass785No ratings yet

- Chapter 12: Leverage and Capital StructureDocument26 pagesChapter 12: Leverage and Capital Structuredebate ddNo ratings yet

- 1.1 Keys To Success: Trendsetters Business Plan Executive SummaryDocument7 pages1.1 Keys To Success: Trendsetters Business Plan Executive SummarymeeventsNo ratings yet

- PS 9 - Chapter 11 - Earnings Management (Solutions)Document40 pagesPS 9 - Chapter 11 - Earnings Management (Solutions)Matteo VidottoNo ratings yet

- Portfolio ManagementDocument31 pagesPortfolio Managementharjot singhNo ratings yet

- Business Plan of Broking Firm: Quick Return Investments Quick Return InvestmentsDocument26 pagesBusiness Plan of Broking Firm: Quick Return Investments Quick Return InvestmentsSunny ParekhNo ratings yet

- Healthcare Assignment Worksheet SIEDocument23 pagesHealthcare Assignment Worksheet SIEsoniekNo ratings yet

- Business Plan FinalDocument7 pagesBusiness Plan Finalapi-545858178No ratings yet

- The Great Re-Ignition Scale-Up Conference (Fri, 25th Feb) - DAY 2Document162 pagesThe Great Re-Ignition Scale-Up Conference (Fri, 25th Feb) - DAY 2Esmeralda HerreraNo ratings yet

- Security Agency Business Plan ExampleDocument39 pagesSecurity Agency Business Plan ExampleedjamesenduranceNo ratings yet

- Carsas Business PlanDocument37 pagesCarsas Business Planvictor thomasNo ratings yet

- Zero To IPO: Lessons From The Unlikely Story ofDocument44 pagesZero To IPO: Lessons From The Unlikely Story ofoutlook.krishnaNo ratings yet

- Advertising Agency Business Plan ExampleDocument28 pagesAdvertising Agency Business Plan ExampleDaniel PipaNo ratings yet

- Edelweiss Abridged AR21 Equity - 31072021 - 080948 - AMDocument92 pagesEdelweiss Abridged AR21 Equity - 31072021 - 080948 - AMSag SagNo ratings yet

- Dealnet Investor Presentation November 2016Document19 pagesDealnet Investor Presentation November 2016kaiselkNo ratings yet

- Back Start UpDocument11 pagesBack Start UpekaNo ratings yet

- G4 - Revel Optis CalDocument9 pagesG4 - Revel Optis CalSteve MedhurstNo ratings yet

- Construction Company Business Plan ExampleDocument19 pagesConstruction Company Business Plan ExamplemiintlyricsNo ratings yet

- Sylabus FinalDocument13 pagesSylabus FinalshahzaibNo ratings yet

- Business Plan Destajo Group 1Document24 pagesBusiness Plan Destajo Group 1Grose Maryjoy Cantiveros DestajoNo ratings yet

- Operation Management Paper FinalDocument10 pagesOperation Management Paper Finalapi-315869258No ratings yet

- Income Disclosure StatementDocument2 pagesIncome Disclosure StatementArin BawalNo ratings yet

- Entrepreneurship - Lesson 2Document14 pagesEntrepreneurship - Lesson 2Adeel AnwarNo ratings yet

- Executive Summary: 1.1 ObjectivesDocument26 pagesExecutive Summary: 1.1 ObjectivesKiran P. UndeNo ratings yet

- Benchmarking Saas Start-Ups: How Am I Doing? Really?Document20 pagesBenchmarking Saas Start-Ups: How Am I Doing? Really?Mahasewa IdNo ratings yet

- Hair and Beauty Salon Business PlanDocument28 pagesHair and Beauty Salon Business PlanDonNo ratings yet

- PresentationDocument43 pagesPresentationapi-3779310No ratings yet

- Business Plan TemplateDocument10 pagesBusiness Plan Templateakinade busayoNo ratings yet

- Pro-Growth HR Group: N B: L BDocument30 pagesPro-Growth HR Group: N B: L BAmit AroraNo ratings yet

- Licit Global PDFDocument10 pagesLicit Global PDFLanod KamakazeNo ratings yet

- Savtech: Save Checks With SavtechDocument21 pagesSavtech: Save Checks With SavtechDavid KellerNo ratings yet

- Tutoring Business Plan ExampleDocument23 pagesTutoring Business Plan Example24 Alvarez, Daniela Joy G.No ratings yet

- AR2021Document169 pagesAR2021Dennis AngNo ratings yet

- BUSINESS PLAN LetzzgooDocument6 pagesBUSINESS PLAN LetzzgooRia MuhiNo ratings yet

- Why Track Sales Pipeline Velocity? Who Cares? Isn't Pipeline Just A Vanity Metric?Document7 pagesWhy Track Sales Pipeline Velocity? Who Cares? Isn't Pipeline Just A Vanity Metric?santosh kumarNo ratings yet

- MCQ 6019 TestDocument38 pagesMCQ 6019 TestpathiranapremabanduNo ratings yet

- Mobile Beauties: 1 Simple Workplace ProjectDocument12 pagesMobile Beauties: 1 Simple Workplace ProjectSayyedKhawarAbbasNo ratings yet

- Vending Machine Business Plan ExampleDocument28 pagesVending Machine Business Plan ExampleRami MishlawiNo ratings yet

- Executive Summary: 1.1 Overview and Summary of Business ProposalDocument18 pagesExecutive Summary: 1.1 Overview and Summary of Business Proposalviper99309No ratings yet

- Finance Assignment 2Document12 pagesFinance Assignment 2fotimaxusanova855No ratings yet

- Food Business Profit and Loss StatementDocument20 pagesFood Business Profit and Loss StatementTarek TorbeyNo ratings yet

- MissionDocument3 pagesMissionShibly Qureshi TamimNo ratings yet

- Bookstore Business Plan ExampleDocument30 pagesBookstore Business Plan ExampleAre EbaNo ratings yet

- Haplos Soap Business Plan2Document6 pagesHaplos Soap Business Plan2Airah MondonedoNo ratings yet

- PayScale Salary ReportsDocument2 pagesPayScale Salary Reportsaravind kumar100% (1)

- The One Page Business Plan CanvasV2017Document1 pageThe One Page Business Plan CanvasV2017Eya Castor BermudezNo ratings yet

- (YEAR) : John & SonsDocument28 pages(YEAR) : John & SonsCinta Rizkia Zahra LubisNo ratings yet

- Tugas Pengantar BisnisDocument18 pagesTugas Pengantar BisnisFarah FairuzNo ratings yet

- Eih Limited: West Bengal, India Delhi 110 054, India S.N. Sridhar, Company Secretary and Compliance OfficerDocument4 pagesEih Limited: West Bengal, India Delhi 110 054, India S.N. Sridhar, Company Secretary and Compliance Officerudeybeer7045No ratings yet

- F9 Financial Management Progress Test 2 PDFDocument3 pagesF9 Financial Management Progress Test 2 PDFCoc GamingNo ratings yet

- Recent Trends in Startup May 2023Document18 pagesRecent Trends in Startup May 2023Pallavi DhaddaNo ratings yet

- Integrated Bank Audit WRKG Papers With SAsDocument3,996 pagesIntegrated Bank Audit WRKG Papers With SAsSHAHNo ratings yet

- Chapter 6 - FS Analysis (Worksheet)Document6 pagesChapter 6 - FS Analysis (Worksheet)angelapearlrNo ratings yet

- 1.0 Executive Summary: 1.1 ObjectivesDocument5 pages1.0 Executive Summary: 1.1 Objectivesethnan lNo ratings yet

- Chapter 11-Investments in Noncurrent Operating Assets-Utilization and RetirementDocument33 pagesChapter 11-Investments in Noncurrent Operating Assets-Utilization and RetirementYukiNo ratings yet

- Ashok Leyland - Annual Report 2017-18Document220 pagesAshok Leyland - Annual Report 2017-18Kumar Prakash100% (1)

- Ajanta Pharma LTD.: Credit Analysis & Research LimitedDocument7 pagesAjanta Pharma LTD.: Credit Analysis & Research Limitedaadsare11287No ratings yet

- SFM DJB - Nov20 Suggested Answers PDFDocument22 pagesSFM DJB - Nov20 Suggested Answers PDFJash BhagatNo ratings yet

- AccountancyDocument9 pagesAccountancyBARSHANo ratings yet

- Application For Registration As An Australian Company: 1 State/territory of RegistrationDocument10 pagesApplication For Registration As An Australian Company: 1 State/territory of Registrationquaz4No ratings yet

- Zimbabwe Stock Exchange Pricelist: The Complete List of ZSE Indices Can Be Obtained From The ZSE Website: WWW - Zse.co - ZWDocument1 pageZimbabwe Stock Exchange Pricelist: The Complete List of ZSE Indices Can Be Obtained From The ZSE Website: WWW - Zse.co - ZWBen GanzwaNo ratings yet

- IntAcc2 - Final Departmental Examination - 2nd Sem AY 2020 2021Document30 pagesIntAcc2 - Final Departmental Examination - 2nd Sem AY 2020 2021Mika MolinaNo ratings yet

- Lecture Notes On Revaluation and Impairment PDFDocument6 pagesLecture Notes On Revaluation and Impairment PDFjudel ArielNo ratings yet

- Advanced Accounting - 2015 (Chapter 17) Multiple Choice Solution (Part I)Document1 pageAdvanced Accounting - 2015 (Chapter 17) Multiple Choice Solution (Part I)John Carlos DoringoNo ratings yet

- Ar 2017 2018Document237 pagesAr 2017 2018Anonymous mMtf10f4No ratings yet

- CH 01 Hull OFOD9 TH EditionDocument36 pagesCH 01 Hull OFOD9 TH EditionPhonglinh WindNo ratings yet

- Xiaojia CV enDocument4 pagesXiaojia CV enapi-434978142No ratings yet

- 11 Income-Tax Lecture-NotesDocument6 pages11 Income-Tax Lecture-NotesandreamrieNo ratings yet

- 6.6.4 Classification of Accounts - SAP - COMPASS CompaniesDocument2 pages6.6.4 Classification of Accounts - SAP - COMPASS CompaniesBaher MohamedNo ratings yet

- Protfolio Analysis of Different CompaniesDocument24 pagesProtfolio Analysis of Different CompaniesPrakash Kumar HindujaNo ratings yet

- CASH FLOW ESTIMATION & RISK ANALYSIS DawDocument7 pagesCASH FLOW ESTIMATION & RISK ANALYSIS DawMaximusNo ratings yet