You might also like

- Stryker Corporation - Assignment 22 March 17Document4 pagesStryker Corporation - Assignment 22 March 17Venkatesh K67% (6)

- Lady M DCF TemplateDocument4 pagesLady M DCF Templatednesudhudh100% (1)

- The EwertDocument2 pagesThe EwertAsif Nasseir100% (1)

- Multi-Period Excess Earnings Method: Southeast Chapter of Business Appraisers September 19-20, 2014Document33 pagesMulti-Period Excess Earnings Method: Southeast Chapter of Business Appraisers September 19-20, 2014Zouhour Ben GhaziNo ratings yet

- Sbux, Peet, and Pro-Forma Pete-DdrxDocument12 pagesSbux, Peet, and Pro-Forma Pete-DdrxfcfroicNo ratings yet

- Apple & RIM Merger Model and LBO ModelDocument50 pagesApple & RIM Merger Model and LBO ModelDarshana MathurNo ratings yet

- Beatrice Peabody's Bond and Stock Valuation ModelDocument4 pagesBeatrice Peabody's Bond and Stock Valuation Modelseth litchfieldNo ratings yet

- Bakery Project Start-Up Business Plan - PDF - Economic Growth - BreadsDocument40 pagesBakery Project Start-Up Business Plan - PDF - Economic Growth - BreadsTaaha Acmad86% (7)

- Analisis Allergy GoneDocument14 pagesAnalisis Allergy GoneGabriela MedranoNo ratings yet

- FGV Acquisition Plan: Financial Analysis On IOI and KLKDocument48 pagesFGV Acquisition Plan: Financial Analysis On IOI and KLKAlexis ChooNo ratings yet

- Nike Inc - Cost of Capital - Syndicate 10Document16 pagesNike Inc - Cost of Capital - Syndicate 10Anthony KwoNo ratings yet

- Vdocuments - MX Chiraigh Din 1Document8 pagesVdocuments - MX Chiraigh Din 1muhamaad.ali.javedNo ratings yet

- Capestone Analysis ExcelDocument29 pagesCapestone Analysis Excelprajout2014No ratings yet

- I. Income StatementDocument27 pagesI. Income StatementNidhi KaushikNo ratings yet

- Current Financial Analysis and ValuationDocument30 pagesCurrent Financial Analysis and ValuationAbhinav PandeyNo ratings yet

- Valuation of AppleDocument25 pagesValuation of AppleQuofi SeliNo ratings yet

- Amazon ValuationDocument22 pagesAmazon ValuationDr Sakshi SharmaNo ratings yet

- 1/29/2010 2009 360 Apple Inc. 2010 $1,000 $192.06 1000 30% 900,678Document18 pages1/29/2010 2009 360 Apple Inc. 2010 $1,000 $192.06 1000 30% 900,678X.r. GeNo ratings yet

- Fin 600 - Radio One-Team 3 - Final SlidesDocument20 pagesFin 600 - Radio One-Team 3 - Final SlidesCarlosNo ratings yet

- Polaroid 1996 CalculationDocument8 pagesPolaroid 1996 CalculationDev AnandNo ratings yet

- ABNB ValuationDocument4 pagesABNB ValuationKasturi MazumdarNo ratings yet

- Lesson 3Document29 pagesLesson 3Anh MinhNo ratings yet

- Rockboro Machine Tools Financial StrategyDocument10 pagesRockboro Machine Tools Financial StrategyPatcharanan SattayapongNo ratings yet

- 04 06 Public Comps Valuation Multiples AfterDocument19 pages04 06 Public Comps Valuation Multiples AfterShanto Arif Uz ZamanNo ratings yet

- 07 12 Sensitivity Tables AfterDocument30 pages07 12 Sensitivity Tables Aftermerag76668No ratings yet

- DocxDocument41 pagesDocxChanduNo ratings yet

- Revised ModelDocument27 pagesRevised ModelAnonymous 0CbF7xaNo ratings yet

- DCF Calculator - V2.2Document5 pagesDCF Calculator - V2.2MuhammadYahsyallahNo ratings yet

- Finance Case Study For Tech Startup Video.01Document10 pagesFinance Case Study For Tech Startup Video.01Extreme TourismNo ratings yet

- Uv0052 Xls EngDocument12 pagesUv0052 Xls Engpriyanshu14No ratings yet

- AFM - IPRO - Mock A - AnswersDocument14 pagesAFM - IPRO - Mock A - AnswersAltaf HussainNo ratings yet

- Optional Problem (Retirement Planning)Document1 pageOptional Problem (Retirement Planning)Rushil SurapaneniNo ratings yet

- BreakEvenPointAnalysis and Selling PriceDocument8 pagesBreakEvenPointAnalysis and Selling PriceAnonymous zOo2mbaVANo ratings yet

- JaletaDocument8 pagesJaletaአረጋዊ ሐይለማርያምNo ratings yet

- QSO 533 Week 4 Homework Starter FileDocument35 pagesQSO 533 Week 4 Homework Starter FileMellaniNo ratings yet

- Project NPV Sensitivity AnalysisDocument54 pagesProject NPV Sensitivity AnalysisAsad Mehmood100% (3)

- Key Performance Indicators (Kpis) : FormulaeDocument4 pagesKey Performance Indicators (Kpis) : FormulaeAfshan AhmedNo ratings yet

- Colorscope 20101029 v0.1 ABDocument16 pagesColorscope 20101029 v0.1 ABakshaybansal100% (2)

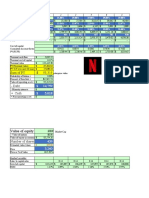

- Sum of PV $ 95,315: Netflix Base Year 1 2 3 4 5Document6 pagesSum of PV $ 95,315: Netflix Base Year 1 2 3 4 5Laura Fonseca SarmientoNo ratings yet

- Solucion Caso Lady MDocument13 pagesSolucion Caso Lady Mjohana irma ore pizarroNo ratings yet

- Bicycle Shop Financial Model - CapEx ForecastDocument9 pagesBicycle Shop Financial Model - CapEx ForecastNatalieNo ratings yet

- CCME Financial Analysis ReportDocument5 pagesCCME Financial Analysis ReportOld School ValueNo ratings yet

- Calculate financial projections and equity value for companyDocument4 pagesCalculate financial projections and equity value for companySunil SharmaNo ratings yet

- DCF Base Year 1 2 3 4 Assumptions:: Valuation of Facebook, Based On Prof. Aswath DamodaranDocument12 pagesDCF Base Year 1 2 3 4 Assumptions:: Valuation of Facebook, Based On Prof. Aswath DamodaranSahaana VijayNo ratings yet

- Historical ProjectionsDocument2 pagesHistorical ProjectionshekmatNo ratings yet

- Inputs For Valuation Current InputsDocument6 pagesInputs For Valuation Current InputsÃarthï ArülrãjNo ratings yet

- FcffevaDocument6 pagesFcffevaShobhit GoyalNo ratings yet

- Análisis Equipo Nutresa Lina - Caso HanssenDocument24 pagesAnálisis Equipo Nutresa Lina - Caso HanssenSARA ZAPATA CANONo ratings yet

- Análisis Equipo Nutresa Lina - Caso Hanssen VFinalDocument28 pagesAnálisis Equipo Nutresa Lina - Caso Hanssen VFinalSARA ZAPATA CANONo ratings yet

- Análisis Equipo Nutresa Lina - Caso Hanssen V2Document27 pagesAnálisis Equipo Nutresa Lina - Caso Hanssen V2SARA ZAPATA CANONo ratings yet

- ProformaDocument1 pageProformaapi-401204785No ratings yet

- Nike Inc. Cost of Capital DCF AnalysisDocument6 pagesNike Inc. Cost of Capital DCF AnalysisrizqighaniNo ratings yet

- Genzyme DCF PDFDocument5 pagesGenzyme DCF PDFAbinashNo ratings yet

- SBI Press Release - SBI Q4 FY22 & Annual ResultsDocument2 pagesSBI Press Release - SBI Q4 FY22 & Annual ResultsSudarshan VaradhanNo ratings yet

- Financial-Forecast AFN FinMgmt 13e BrighamDocument19 pagesFinancial-Forecast AFN FinMgmt 13e BrighamRimpy SondhNo ratings yet

- MFL 1 Cfin2Document17 pagesMFL 1 Cfin2Siddharth SureshNo ratings yet

- Kes 2 - EPPM3644 BBAE KL - CLEAR LAKE BAKERY - KUMP 3Document5 pagesKes 2 - EPPM3644 BBAE KL - CLEAR LAKE BAKERY - KUMP 3Durga LetchumananNo ratings yet

- BNI 111709 v2Document2 pagesBNI 111709 v2fcfroicNo ratings yet

- Apple Case StudyDocument2 pagesApple Case StudyPrakhar MorchhaleNo ratings yet

- Damodaran Excel - After Class - RegDocument2 pagesDamodaran Excel - After Class - RegAris KurniawanNo ratings yet

- Excel To Business Analys ExamDocument15 pagesExcel To Business Analys Examrhea23aNo ratings yet

- MacabacusEssentialsDemoComplete 210413 104622Document21 pagesMacabacusEssentialsDemoComplete 210413 104622Pratik PatwaNo ratings yet

- Solutions Selling Model - ConsolidatedDocument61 pagesSolutions Selling Model - ConsolidatedRuben GomezNo ratings yet

- Suggested End of Chapter Problems and QuestionsDocument4 pagesSuggested End of Chapter Problems and QuestionsThe oneNo ratings yet

- Principles of Cash Flow Valuation: An Integrated Market-Based ApproachFrom EverandPrinciples of Cash Flow Valuation: An Integrated Market-Based ApproachRating: 3 out of 5 stars3/5 (3)

- FE Labeling Final Rule Formulae - RuleDocument24 pagesFE Labeling Final Rule Formulae - RuleSashi VelnatiNo ratings yet

- Chapter 8 Homework Assignment Ver 1.0Document2 pagesChapter 8 Homework Assignment Ver 1.0Sashi VelnatiNo ratings yet

- Michigan Green Power Wind Turbine Blade Plant Project - Org ChartDocument1 pageMichigan Green Power Wind Turbine Blade Plant Project - Org ChartSashi VelnatiNo ratings yet

- Competitive Environment of The Airline IndustryDocument19 pagesCompetitive Environment of The Airline IndustrySashi VelnatiNo ratings yet

- SSNLF Key RatiosDocument16 pagesSSNLF Key RatiosSashi VelnatiNo ratings yet

- Southwest 5 FORCESDocument11 pagesSouthwest 5 FORCESBvvss RamanjaneyuluNo ratings yet

- Another European Automaker Has U.S Emissions Problem PDFDocument4 pagesAnother European Automaker Has U.S Emissions Problem PDFSashi VelnatiNo ratings yet

- How Do The 7 Largest Auto Companies Stack Up Against Each OtherDocument3 pagesHow Do The 7 Largest Auto Companies Stack Up Against Each OtherSashi VelnatiNo ratings yet

- The EPA's Fuel Efficiency Testing May Not WorkDocument15 pagesThe EPA's Fuel Efficiency Testing May Not WorkSashi VelnatiNo ratings yet

- Making Pay PublicDocument10 pagesMaking Pay PublicSashi VelnatiNo ratings yet

- Prudential AsianAmerFinExperReportDocument16 pagesPrudential AsianAmerFinExperReportSashi VelnatiNo ratings yet

- Another European Automaker Has U.S Emissions ProblemDocument4 pagesAnother European Automaker Has U.S Emissions ProblemSashi VelnatiNo ratings yet

- Chapter 12 Exchange-Rate DeterminationDocument56 pagesChapter 12 Exchange-Rate DeterminationSashi VelnatiNo ratings yet

- Analyzing Porter's Five Forces On Delta Airlines (DAL) - InvestopediaDocument5 pagesAnalyzing Porter's Five Forces On Delta Airlines (DAL) - InvestopediaSashi VelnatiNo ratings yet

- International Trade TheoriesDocument46 pagesInternational Trade TheoriesChiranjay BiswalNo ratings yet

- P&G Financial Analysis and ValuationDocument30 pagesP&G Financial Analysis and ValuationSashi VelnatiNo ratings yet

- ROIC SpreadsheetDocument8 pagesROIC SpreadsheetSashi VelnatiNo ratings yet

- Myrna 2009 Employment Relations TodayDocument7 pagesMyrna 2009 Employment Relations TodaySashi VelnatiNo ratings yet

- Investor Presentation Kotak Goldman Sachs Conference September2005 PDFDocument37 pagesInvestor Presentation Kotak Goldman Sachs Conference September2005 PDFSashi VelnatiNo ratings yet

- Water Usage CalculatorDocument8 pagesWater Usage CalculatorSashi VelnatiNo ratings yet

- How To Read A Car's VINDocument12 pagesHow To Read A Car's VINSashi VelnatiNo ratings yet

- Making Pay PublicDocument10 pagesMaking Pay PublicSashi VelnatiNo ratings yet

- 2013 December Breakfast Briefing Presentation - Stuart JohnsonDocument37 pages2013 December Breakfast Briefing Presentation - Stuart JohnsonSashi VelnatiNo ratings yet

- What Is Evidence-Based Human Resource Management?Document3 pagesWhat Is Evidence-Based Human Resource Management?Sashi VelnatiNo ratings yet

- Viavision eDocument8 pagesViavision eSashi VelnatiNo ratings yet

- John Casesa - GuggenheimDocument26 pagesJohn Casesa - GuggenheimSashi VelnatiNo ratings yet

- Here's What The Average American's Budget Looks Like (Warning - It's Not Pretty!) - The Motley FoolDocument9 pagesHere's What The Average American's Budget Looks Like (Warning - It's Not Pretty!) - The Motley FoolSashi VelnatiNo ratings yet

- 4c AlfaRomeo Spec Sheet UsDocument5 pages4c AlfaRomeo Spec Sheet UsSashi VelnatiNo ratings yet

- Alfa Romeo 2014 Business PlanDocument55 pagesAlfa Romeo 2014 Business PlanFiat500USA100% (1)

- Investment DecisionDocument26 pagesInvestment DecisionToyin Gabriel AyelemiNo ratings yet

- FM CH02Document94 pagesFM CH02nitu mdNo ratings yet

- Project Finance ValuationDocument141 pagesProject Finance ValuationRohit KatariaNo ratings yet

- 7 Urea Synthesis Using Chemical Looping ProcessDocument10 pages7 Urea Synthesis Using Chemical Looping ProcessandiesNo ratings yet

- Ross 10e Chap008 StudentDocument42 pagesRoss 10e Chap008 StudentValentin MardonNo ratings yet

- 1 PBDocument6 pages1 PBMohammad MultazamNo ratings yet

- Capital Budgeting Techniques: NPV, IRR & MoreDocument96 pagesCapital Budgeting Techniques: NPV, IRR & MoreAarushi ManchandaNo ratings yet

- Risk Analysis in Capital BudgetingDocument6 pagesRisk Analysis in Capital BudgetingSandhya VermaNo ratings yet

- Project Proposal For GC (Demissie)Document21 pagesProject Proposal For GC (Demissie)alemayehu tariku100% (1)

- TPG 2021 Annual ReportDocument1,175 pagesTPG 2021 Annual Report魏xxxappleNo ratings yet

- CARE Form 1.6 - Hibionada - MatucoDocument7 pagesCARE Form 1.6 - Hibionada - MatucoBea Nicole EstradaNo ratings yet

- Capital Budgeting Techniques Explained in DetailDocument26 pagesCapital Budgeting Techniques Explained in DetailTisha SosaNo ratings yet

- Corporate Finance Fin622 Short NoteDocument29 pagesCorporate Finance Fin622 Short Notezahidwahla133% (3)

- Ranking Mutually Exclusive InvestmentsDocument22 pagesRanking Mutually Exclusive InvestmentsSimran JainNo ratings yet

- La Consolacion College Manila: Finman IiDocument14 pagesLa Consolacion College Manila: Finman Iigerald calignerNo ratings yet

- 11ch21 Capital BudgetingDocument54 pages11ch21 Capital BudgetingLi'ilzam NuurNo ratings yet

- True True: True or False QuestionsDocument7 pagesTrue True: True or False QuestionsJimmyChaoNo ratings yet

- Capital Budgeting and Cash Flow ProjectionDocument21 pagesCapital Budgeting and Cash Flow Projectionnira_110No ratings yet

- Capital Budgeting TechniquesDocument97 pagesCapital Budgeting TechniquesPriyanshu Singh0% (1)

- MS11 - Capital BudgetingDocument8 pagesMS11 - Capital BudgetingElsie GenovaNo ratings yet

- MGT Info (KL-PS) Question BankDocument14 pagesMGT Info (KL-PS) Question BankPrabir Kumer RoyNo ratings yet

- The MRT 3 Contract: Atty. Helena C. Tolentino 1 June 2012Document39 pagesThe MRT 3 Contract: Atty. Helena C. Tolentino 1 June 2012helicarinotolentino100% (4)

- Beyond Budgeting DissertationDocument7 pagesBeyond Budgeting DissertationCustomWrittenPapersCanada100% (1)

- CAPITAL BUDGETING DECISION - IMI Delhi - 2022Document46 pagesCAPITAL BUDGETING DECISION - IMI Delhi - 2022Eeshank KarnwalNo ratings yet

- Case... Phuket Beach HotelDocument3 pagesCase... Phuket Beach HotelSanjay Kumar JainNo ratings yet