You might also like

- COMMERCIAL LAW REVIEWER - OngoingDocument93 pagesCOMMERCIAL LAW REVIEWER - OngoingAmiel SaquisameNo ratings yet

- NFo BJT1bt7PsZ69 AOU024Kv3zMsPKF9 Ilp D 1 S 2 Fundamentals of Insurance Updated 01-30-2018Document13 pagesNFo BJT1bt7PsZ69 AOU024Kv3zMsPKF9 Ilp D 1 S 2 Fundamentals of Insurance Updated 01-30-2018Tech VisionNo ratings yet

- Terminology and ConceptsDocument5 pagesTerminology and Conceptsdid0kuLNo ratings yet

- Insurance Class NotesDocument5 pagesInsurance Class NotesNaiza Mae R. BinayaoNo ratings yet

- Insurance Contract PDFDocument50 pagesInsurance Contract PDFdiacu diana100% (6)

- IC 38 Jan QuestionDocument37 pagesIC 38 Jan QuestionDeepaNo ratings yet

- 01 Property Casualty Insurance Basics-14Document28 pages01 Property Casualty Insurance Basics-14kandurimaruthiNo ratings yet

- Topic Insurance LawDocument28 pagesTopic Insurance LawAtty Rester John NonatoNo ratings yet

- Root 2Document41 pagesRoot 2Pranav ViraNo ratings yet

- MercRev - InsuranceDocument18 pagesMercRev - InsuranceA GrafiloNo ratings yet

- Insurance MatrixDocument12 pagesInsurance MatrixAssecmaNo ratings yet

- INS 21 Chapter9-Insurance PoliciesDocument27 pagesINS 21 Chapter9-Insurance Policiesvenki_hinfotechNo ratings yet

- Legal Principle of InsuranceDocument44 pagesLegal Principle of InsuranceFahim MahmudNo ratings yet

- San Beda College of Law: Insurance CodeDocument27 pagesSan Beda College of Law: Insurance CodeJANISCHAJEAN RECTONo ratings yet

- United India Insurance Co REPORT 22.07.19Document53 pagesUnited India Insurance Co REPORT 22.07.19Trilok SamtaniNo ratings yet

- Report 22.07.19Document53 pagesReport 22.07.19Trilok SamtaniNo ratings yet

- Maid BedaDocument24 pagesMaid BedaMarx LibiranNo ratings yet

- Insurance ConceptsDocument9 pagesInsurance ConceptsAlexandra Nicole SugayNo ratings yet

- InsuranceDocument50 pagesInsuranceRhose Azcelle MagaoayNo ratings yet

- Insurance Midterms ReviewerDocument28 pagesInsurance Midterms ReviewerMichaela SarmientoNo ratings yet

- InsuranceDocument45 pagesInsuranceAlex HaymeNo ratings yet

- 1 - General-Provisions1 (AQUINO INSURANCE SUMMARY)Document4 pages1 - General-Provisions1 (AQUINO INSURANCE SUMMARY)aifapnglnnNo ratings yet

- Session 4 - Types of InsuranceDocument50 pagesSession 4 - Types of InsuranceJames Patrick PedrosoNo ratings yet

- Risk Chapter 7Document15 pagesRisk Chapter 7Wonde Biru100% (1)

- B LawDocument26 pagesB LawShrutika JainNo ratings yet

- Key Facts InsuranceDocument18 pagesKey Facts InsurancePrimal PropheciesNo ratings yet

- Insurance Code: 7. Personal - Each Party Having in ViewDocument24 pagesInsurance Code: 7. Personal - Each Party Having in ViewEhem DrpNo ratings yet

- Understanding Insurance BasicsDocument25 pagesUnderstanding Insurance BasicsTewodros TeshomeNo ratings yet

- San Beda College of Law: Insurance CodeDocument27 pagesSan Beda College of Law: Insurance Codeglee0% (1)

- INSURANCE Beda Reviewer PDFDocument24 pagesINSURANCE Beda Reviewer PDFLalay BarceNo ratings yet

- Warranties in Insurance PoliciesDocument12 pagesWarranties in Insurance PoliciesKinoLodaNo ratings yet

- Risk Chapter 4Document14 pagesRisk Chapter 4Wonde BiruNo ratings yet

- 3.fundamentals of Insurance-Part-2 - 1526989599Document10 pages3.fundamentals of Insurance-Part-2 - 1526989599Prakash PNo ratings yet

- Fundamentals of Insurance Part 2Document10 pagesFundamentals of Insurance Part 2Rajendranath Behera0% (1)

- Insurance PlanningDocument18 pagesInsurance PlanningNeha SharmaNo ratings yet

- Insurance 101Document53 pagesInsurance 101Seerat MahajanNo ratings yet

- Handbook On InsuranceDocument20 pagesHandbook On InsuranceSri Muslihah BakhtiarNo ratings yet

- Insurance Bernstein2Document17 pagesInsurance Bernstein2JobaiyerNo ratings yet

- Reflection On Justness and SincerityDocument9 pagesReflection On Justness and SincerityGayFleur Cabatit RamosNo ratings yet

- Insurance Contract (Power Point To Learn) Commercial LawDocument11 pagesInsurance Contract (Power Point To Learn) Commercial Lawpaulamartinsoto00No ratings yet

- San Beda Memory Aid - InsuranceDocument24 pagesSan Beda Memory Aid - InsurancebreeH20No ratings yet

- Risk Management and Insurance CH 04 Legal Principles of InsuranceDocument18 pagesRisk Management and Insurance CH 04 Legal Principles of Insuranceshekaibsa38No ratings yet

- 2022 Commercial Law Syllabus-Based EREVIEWERDocument83 pages2022 Commercial Law Syllabus-Based EREVIEWERRaikha D. BarraNo ratings yet

- Insurance GlossaryDocument59 pagesInsurance Glossarypramod.dNo ratings yet

- Property & Casualty Insurance BasicsDocument28 pagesProperty & Casualty Insurance Basics邵晨冬No ratings yet

- INS 21 Chapter 6-ClaimsDocument30 pagesINS 21 Chapter 6-Claimsvenki_hinfotechNo ratings yet

- Insurance Reviewer 2005Document25 pagesInsurance Reviewer 2005emmaniago0829No ratings yet

- Commercial Law - InsuranceDocument14 pagesCommercial Law - InsuranceRoji Belizar HernandezNo ratings yet

- INSURANCE (Sept 13)Document22 pagesINSURANCE (Sept 13)Vida MarieNo ratings yet

- Insurance - Business LawDocument18 pagesInsurance - Business LawAlbertina Lucia CerdaNo ratings yet

- Insurance ReviewerDocument3 pagesInsurance Reviewerjao jaoNo ratings yet

- Insurance Code: 7. Personal - Each Party Having in ViewDocument24 pagesInsurance Code: 7. Personal - Each Party Having in Viewjolly faith pariñasNo ratings yet

- Insurance LawDocument1 pageInsurance LawCinja ShidoujiNo ratings yet

- Insight Into Basics of General InsuranceDocument50 pagesInsight Into Basics of General Insurancepiyushkumarjha12No ratings yet

- 2020111817285486601-Legal Angle - November 2020 - Issue 03Document6 pages2020111817285486601-Legal Angle - November 2020 - Issue 03Reshmi SanathNo ratings yet

- Reviewer InsuranceDocument25 pagesReviewer InsuranceShaine ArellanoNo ratings yet

- Understanding Named, Automatic and Additional Insureds in the CGL PolicyFrom EverandUnderstanding Named, Automatic and Additional Insureds in the CGL PolicyNo ratings yet

- Life, Accident and Health Insurance in the United StatesFrom EverandLife, Accident and Health Insurance in the United StatesRating: 5 out of 5 stars5/5 (1)

- State Farm Auto PolicyDocument28 pagesState Farm Auto Policyhatanolove80% (5)

- Auto InsuranceDocument14 pagesAuto InsurancehatanoloveNo ratings yet

- MoveDocument31 pagesMovehatanolove100% (1)

- MoveDocument31 pagesMovehatanolove100% (1)

- Risk and InsuranceDocument17 pagesRisk and Insurancehatanolove100% (5)

- Tir 08 2 BerggrenDocument19 pagesTir 08 2 BerggrenhatanoloveNo ratings yet

- GNIPCDocument4 pagesGNIPChatanolove100% (2)

- The Application of Austrian Business Cycle TheoryDocument21 pagesThe Application of Austrian Business Cycle Theoryhatanolove100% (1)

- Practice Midterm KeyDocument4 pagesPractice Midterm KeyhatanoloveNo ratings yet

- Study Questions For Chapters 14-16-20Document4 pagesStudy Questions For Chapters 14-16-20hatanoloveNo ratings yet

- SHQ Practice Q Answer KeyDocument1 pageSHQ Practice Q Answer KeyhatanoloveNo ratings yet

- Mgmt3620 Syllabus (S08)Document4 pagesMgmt3620 Syllabus (S08)hatanoloveNo ratings yet

- SHQ Practice QDocument1 pageSHQ Practice QhatanoloveNo ratings yet

- Revised Schedule MGNT4670 Winter 2008 Section 02Document2 pagesRevised Schedule MGNT4670 Winter 2008 Section 02hatanoloveNo ratings yet

- Sample Questions: Multiple ChoicesDocument4 pagesSample Questions: Multiple ChoiceshatanoloveNo ratings yet

- Supply Side Economics-GwartneyDocument3 pagesSupply Side Economics-GwartneyhatanoloveNo ratings yet

- SCF - Practice QDocument3 pagesSCF - Practice QhatanoloveNo ratings yet

- Midterm InformationDocument2 pagesMidterm InformationhatanoloveNo ratings yet

- Milton FriedmanDocument3 pagesMilton FriedmanhatanoloveNo ratings yet

- Libby Chapter 6 Study NotesDocument6 pagesLibby Chapter 6 Study NoteshatanoloveNo ratings yet

- Management Mistakes That President Bush MadeDocument5 pagesManagement Mistakes That President Bush Madehatanolove100% (2)

- Martha StewartDocument4 pagesMartha Stewarthatanolove100% (3)

- Keynes Robert ReichDocument4 pagesKeynes Robert ReichhatanoloveNo ratings yet

- Libby Chap 11 Study NotesDocument16 pagesLibby Chap 11 Study Noteshatanolove100% (4)

- HW 7 Answer KeyDocument2 pagesHW 7 Answer KeyhatanoloveNo ratings yet

- Income, Life-Satisfaction and Real Consumption InequalityDocument4 pagesIncome, Life-Satisfaction and Real Consumption InequalityhatanoloveNo ratings yet

- Governor Frederic S. Mishkin: How Should We Respond To Asset Price Bubbles?Document10 pagesGovernor Frederic S. Mishkin: How Should We Respond To Asset Price Bubbles?hatanoloveNo ratings yet

- Homework Assignment 6Document1 pageHomework Assignment 6hatanoloveNo ratings yet

- Governor Frederic S. Mishkin: How Should We Respond To Asset Price Bubbles?Document10 pagesGovernor Frederic S. Mishkin: How Should We Respond To Asset Price Bubbles?hatanoloveNo ratings yet

- Cognizant Company FAQDocument4 pagesCognizant Company FAQManojChowdary100% (1)

- Labor LawDocument6 pagesLabor LawElden Cunanan BonillaNo ratings yet

- Experiment No 9 - Part1Document38 pagesExperiment No 9 - Part1Nipun GosaiNo ratings yet

- 2010 LeftySpeed Oms en 0Document29 pages2010 LeftySpeed Oms en 0Discord ShadowNo ratings yet

- HTTP ProtocolDocument16 pagesHTTP ProtocolHao NguyenNo ratings yet

- INCOME TAX AND GST. JURAZ-Module 4Document8 pagesINCOME TAX AND GST. JURAZ-Module 4TERZO IncNo ratings yet

- Geography Cba PowerpointDocument10 pagesGeography Cba Powerpointapi-489088076No ratings yet

- LINDE Spare Parts ListDocument2 pagesLINDE Spare Parts Listsharafudheen_s100% (2)

- Important Dates (PG Students View) Semester 1, 2022-2023 - All Campus (As of 2 October 2022)Document4 pagesImportant Dates (PG Students View) Semester 1, 2022-2023 - All Campus (As of 2 October 2022)AFHAM JAUHARI BIN ALDI (MITI)No ratings yet

- MBA CurriculumDocument93 pagesMBA CurriculumkaranNo ratings yet

- Mechanical FPD P.sanchezDocument9 pagesMechanical FPD P.sanchezHailley DensonNo ratings yet

- Resistor 1k - Vishay - 0.6wDocument3 pagesResistor 1k - Vishay - 0.6wLEDNo ratings yet

- Coding Guidelines-CDocument71 pagesCoding Guidelines-CKishoreRajuNo ratings yet

- Marketing For Hospitality & TourismDocument5 pagesMarketing For Hospitality & Tourismislahu56No ratings yet

- Risk Management GuidanceDocument9 pagesRisk Management GuidanceHelen GouseNo ratings yet

- PRU03Document4 pagesPRU03Paul MathewNo ratings yet

- The Man Who Knew Too Much: The JFK Assassination TheoriesDocument4 pagesThe Man Who Knew Too Much: The JFK Assassination TheoriesedepsteinNo ratings yet

- Drafting Foundation PlanDocument24 pagesDrafting Foundation Planerol bancoroNo ratings yet

- Notes in Train Law PDFDocument11 pagesNotes in Train Law PDFJanica Lobas100% (1)

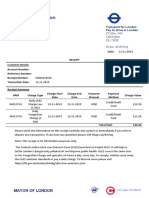

- Transport For London Pay To Drive in London: PO Box 344 Darlington Dl1 9qe TFL - Gov.uk/drivingDocument1 pageTransport For London Pay To Drive in London: PO Box 344 Darlington Dl1 9qe TFL - Gov.uk/drivingDanyy MaciucNo ratings yet

- Reflection of The Movie Informant - RevisedDocument3 pagesReflection of The Movie Informant - RevisedBhavika BhatiaNo ratings yet

- Status Of: Philippine ForestsDocument11 pagesStatus Of: Philippine ForestsAivy Rose VillarbaNo ratings yet

- Pepsi IMCDocument19 pagesPepsi IMCMahi Teja0% (2)

- Windows Crash Dump AnalysisDocument11 pagesWindows Crash Dump Analysisbetatest12No ratings yet

- 1654403-1 Press Fit ConnectorsDocument40 pages1654403-1 Press Fit ConnectorsRafael CastroNo ratings yet

- Aperio CS2 BrochureDocument3 pagesAperio CS2 BrochurelailaNo ratings yet

- 7779 19506 1 PBDocument24 pages7779 19506 1 PBAyessa FerrerNo ratings yet

- Tales of Mystery Imagination and Humour Edgar Allan Poe PDFDocument289 pagesTales of Mystery Imagination and Humour Edgar Allan Poe PDFmatildameisterNo ratings yet

- Hippa and ISO MappingDocument13 pagesHippa and ISO Mappingnidelel214No ratings yet

- Intermediate Microeconomics and Its Application 12th Edition Nicholson Solutions ManualDocument9 pagesIntermediate Microeconomics and Its Application 12th Edition Nicholson Solutions Manualchiliasmevenhandtzjz8j100% (27)