You might also like

- 2018 Article Iv Consultation-MyanmarDocument91 pages2018 Article Iv Consultation-MyanmarLet's Save MyanmarNo ratings yet

- Code Standard For Rice 198-1995Document6 pagesCode Standard For Rice 198-1995Let's Save MyanmarNo ratings yet

- Lemon Law in Singapore:Consumer Protection (Fair Trading) ActDocument55 pagesLemon Law in Singapore:Consumer Protection (Fair Trading) ActLet's Save MyanmarNo ratings yet

- The Regime S Cronies List June 27 2011 FinalDocument14 pagesThe Regime S Cronies List June 27 2011 FinalLet's Save Myanmar100% (1)

- Yangon Circular Railway Line Upgrading Project !Document274 pagesYangon Circular Railway Line Upgrading Project !THAN HAN100% (1)

- MYANMAR SELECTED ISSUES (International Monetary Fund)Document34 pagesMYANMAR SELECTED ISSUES (International Monetary Fund)Let's Save MyanmarNo ratings yet

- Strategic Environmental Assessment of The Myanmar Hydropower Sector IFCDocument152 pagesStrategic Environmental Assessment of The Myanmar Hydropower Sector IFCBhamotharNo ratings yet

- Recent Developments of The Myanmar Economy - Nov 6,2018Document9 pagesRecent Developments of The Myanmar Economy - Nov 6,2018Let's Save MyanmarNo ratings yet

- Six Billion Dollar Timber Corruption Black Hole Revealed by Official Data - EIA Data CorruptionDocument6 pagesSix Billion Dollar Timber Corruption Black Hole Revealed by Official Data - EIA Data CorruptionLet's Save MyanmarNo ratings yet

- Singapore CPFDocument1 pageSingapore CPFLet's Save MyanmarNo ratings yet

- Myanmar Tourism Statistics 2016 1Document2 pagesMyanmar Tourism Statistics 2016 1Let's Save MyanmarNo ratings yet

- Myanmar Travel & Tourism Economic Impact 2017Document24 pagesMyanmar Travel & Tourism Economic Impact 2017Let's Save MyanmarNo ratings yet

- The Study of SME's Contribution To Myanmar's Economic DevelopmentDocument8 pagesThe Study of SME's Contribution To Myanmar's Economic DevelopmentTHAN HANNo ratings yet

- UNDP MM Perception Survey EnglishDocument47 pagesUNDP MM Perception Survey EnglishLet's Save MyanmarNo ratings yet

- 2016 Pwint Thit Sa enDocument48 pages2016 Pwint Thit Sa enYe PhoneNo ratings yet

- Myanmar Investment Law Official Translation 3-1-2017Document32 pagesMyanmar Investment Law Official Translation 3-1-2017THAN HANNo ratings yet

- 2018-PTS enDocument2 pages2018-PTS enLet's Save MyanmarNo ratings yet

- Press Release For Tea Briefing Paper in English VersionDocument1 pagePress Release For Tea Briefing Paper in English VersionLet's Save MyanmarNo ratings yet

- Myanmar Finincal Report 2102Document114 pagesMyanmar Finincal Report 2102Let's Save MyanmarNo ratings yet

- SMEs Situation Myanamr 2016Document12 pagesSMEs Situation Myanamr 2016Let's Save MyanmarNo ratings yet

- Myanmar Companies Law 2017Document188 pagesMyanmar Companies Law 2017Let's Save Myanmar100% (1)

- Tea Briefing Paper by Burmese VersionDocument13 pagesTea Briefing Paper by Burmese VersionAung Myo TheinNo ratings yet

- Articles CompanyDocument45 pagesArticles CompanyLet's Save MyanmarNo ratings yet

- RaportiDocument245 pagesRaportiFlorenc StafaNo ratings yet

- SME Financing in Myanmar (8 September 2013)Document19 pagesSME Financing in Myanmar (8 September 2013)THAN HANNo ratings yet

- Set Myanmar Final 170404Document83 pagesSet Myanmar Final 170404THAN HANNo ratings yet

- Quarterly Financial Statistics Bulletin (Volume I 2017)Document98 pagesQuarterly Financial Statistics Bulletin (Volume I 2017)Let's Save MyanmarNo ratings yet

- Myanamr Yearly Approved Amount of Foreign Investment (By Country)Document1 pageMyanamr Yearly Approved Amount of Foreign Investment (By Country)Let's Save MyanmarNo ratings yet

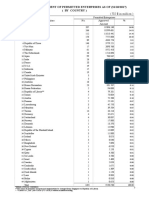

- Myanmar Foreign Investment of Permitted Enterprises As of (31/10/2017) (By Country)Document4 pagesMyanmar Foreign Investment of Permitted Enterprises As of (31/10/2017) (By Country)Let's Save MyanmarNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Spring 2009 Mgt201 3 VuabidDocument5 pagesSpring 2009 Mgt201 3 Vuabidsaeedsjaan100% (3)

- Dynamic Risk ParityDocument18 pagesDynamic Risk ParityRohit ChandraNo ratings yet

- Delta Marketing TrendsDocument7 pagesDelta Marketing TrendsCandy SaberNo ratings yet

- ACC702 International Corporate ReportingDocument16 pagesACC702 International Corporate ReportingShazana KhanNo ratings yet

- Case 52 Sanofi-Aventis's - Analysis GuidanceDocument2 pagesCase 52 Sanofi-Aventis's - Analysis Guidancebaworanan46No ratings yet

- Nirmal Bang Securities Pvt. LTD Company ProfileDocument7 pagesNirmal Bang Securities Pvt. LTD Company ProfileTeja Choudhary Medarametla100% (2)

- FF Full Eng PDFDocument146 pagesFF Full Eng PDFAnonymous YgBIdKxvNo ratings yet

- SAFE PrimerDocument8 pagesSAFE PrimerJaap FrölichNo ratings yet

- Deepak Nitrite by Edelweiss (From BIGBULLS)Document5 pagesDeepak Nitrite by Edelweiss (From BIGBULLS)Ranjan BeheraNo ratings yet

- Forex 1 PDFDocument3 pagesForex 1 PDFgatNo ratings yet

- Unpaid Sheet 2014Document234 pagesUnpaid Sheet 2014Jagadamba RealtorNo ratings yet

- Buscom SPDocument16 pagesBuscom SPCatherine Joy Vasaya100% (1)

- Qoul Quo Srai Sek 7 2603201401Document6 pagesQoul Quo Srai Sek 7 2603201401hafiz091201No ratings yet

- This Study Resource Was: Logo HereDocument5 pagesThis Study Resource Was: Logo HereMarcus MonocayNo ratings yet

- 02 - Price Action StrategiesDocument82 pages02 - Price Action Strategiesvvpvarun94% (63)

- Five Day Trading Programme Amplify Trading 2014Document7 pagesFive Day Trading Programme Amplify Trading 2014RahulNo ratings yet

- Larry Steffen Case StudyDocument4 pagesLarry Steffen Case StudyRicky ZhaiNo ratings yet

- Foreign Exchange Markets and TransactionsDocument9 pagesForeign Exchange Markets and TransactionsAli khanNo ratings yet

- Nippon India Growth Fund: (Mid Cap Fund-An Open Ended Equity Scheme Predominantly Investing in Mid Cap Stocks)Document29 pagesNippon India Growth Fund: (Mid Cap Fund-An Open Ended Equity Scheme Predominantly Investing in Mid Cap Stocks)Saif MansooriNo ratings yet

- Multi Time Frame Structure Breakdown for Identifying High Probability Trade SetupsDocument6 pagesMulti Time Frame Structure Breakdown for Identifying High Probability Trade SetupsFX IINo ratings yet

- Equity Linked Notes (ELNs) DBS TreasuresDocument1 pageEquity Linked Notes (ELNs) DBS Treasuresspecul8tor10No ratings yet

- Financial Market Risks & ManagementDocument73 pagesFinancial Market Risks & Managementakhilyerawar7013No ratings yet

- Day 1Document28 pagesDay 1CHENAB WEST100% (1)

- Goal Assure BrochureDocument20 pagesGoal Assure BrochureBharat19No ratings yet

- Gemini Electronics: US LCD TV Giant's Growth & Financial AnalysisDocument1 pageGemini Electronics: US LCD TV Giant's Growth & Financial AnalysisSreeda PerikamanaNo ratings yet

- Bloomberg - Performance Attribution ModelDocument17 pagesBloomberg - Performance Attribution Modelde deNo ratings yet

- Exchange Rate MechanismDocument42 pagesExchange Rate Mechanismpriya nNo ratings yet

- Hedge Funds Presentation Apr 08Document31 pagesHedge Funds Presentation Apr 08Marina BoldinaNo ratings yet

- Good-bye original sin, hello risk on-off, financial fragility, and crises? Analysis of EM sovereign bond issuanceDocument14 pagesGood-bye original sin, hello risk on-off, financial fragility, and crises? Analysis of EM sovereign bond issuanceNadia Cenat CenutNo ratings yet

- Modul Lab. Akuntansi Menengah 2 - P 20.21Document54 pagesModul Lab. Akuntansi Menengah 2 - P 20.21Ivonie NursalimNo ratings yet