You might also like

- IACS Technical BackgroudDocument552 pagesIACS Technical BackgroudSeong Ju KangNo ratings yet

- SHIPOWNERS Sampling Procedures For TankersDocument5 pagesSHIPOWNERS Sampling Procedures For TankersErsin SaltNo ratings yet

- CDI 9th Edition SIR Consolidated Gas - Amendments June 2020Document5 pagesCDI 9th Edition SIR Consolidated Gas - Amendments June 2020AlexandrosNo ratings yet

- Tugs - Developments For PDFDocument28 pagesTugs - Developments For PDFP Venkata SureshNo ratings yet

- Effective Fuel Cost On Liner Service ConfDocument13 pagesEffective Fuel Cost On Liner Service ConfOlga RegevNo ratings yet

- 2009 IAME Notteboom & CariouDocument26 pages2009 IAME Notteboom & CarioupravanthbabuNo ratings yet

- Seca PDFDocument20 pagesSeca PDFAleksanrd MihailovNo ratings yet

- Job Description Fleet ManagerDocument3 pagesJob Description Fleet ManagerdevivovincenzoNo ratings yet

- Difference Between Bulk and Break BulkDocument17 pagesDifference Between Bulk and Break BulkHarun Kınalı0% (1)

- Battery Room Ventilationa and Proper UpkeepingDocument2 pagesBattery Room Ventilationa and Proper Upkeepingdassi99No ratings yet

- Oil LossesDocument12 pagesOil Lossesrenkli100% (2)

- Law Relating To Maritime Wrecks in India.Document5 pagesLaw Relating To Maritime Wrecks in India.Syam Kumar V.M.No ratings yet

- Amends To SDs 2011Document214 pagesAmends To SDs 2011duaankushNo ratings yet

- Engine Management - Concept For LNG Carriers PDFDocument20 pagesEngine Management - Concept For LNG Carriers PDFKarim Sowley DelgadoNo ratings yet

- How To Become Member of IACS: Class Does So by Issuing A "Condition of Class", Which Means That To Be Able To RetainDocument2 pagesHow To Become Member of IACS: Class Does So by Issuing A "Condition of Class", Which Means That To Be Able To RetainPrasoon SharmaNo ratings yet

- Ocimf 2014年第5版 船靠船作业指南 介绍 20-Tech-feb-2014Document2 pagesOcimf 2014年第5版 船靠船作业指南 介绍 20-Tech-feb-2014xingangNo ratings yet

- 2020 IMO Fuel Sulphur RegulationDocument7 pages2020 IMO Fuel Sulphur Regulationlucas100% (1)

- OCIMF High Risk' Observations ListDocument7 pagesOCIMF High Risk' Observations ListFerdinand ArsolonNo ratings yet

- 27snii15 Week27 2015Document151 pages27snii15 Week27 2015Kunal SinghNo ratings yet

- Iacs Ship Structure Access ManualDocument18 pagesIacs Ship Structure Access ManualKordalhs Kyriakos100% (1)

- UK P I Bunkers and BunkeringDocument48 pagesUK P I Bunkers and BunkeringGeorgios PapakostasNo ratings yet

- Convention For The Safe and Environmentally Sound RecyclingDocument23 pagesConvention For The Safe and Environmentally Sound RecyclingDharam TripathyNo ratings yet

- Part W Navigation Bridge VisibilityDocument9 pagesPart W Navigation Bridge VisibilityDian Nafi' AhmadNo ratings yet

- ASM Masters Solved Past Question Papers Solved Numericals From Sept16 Till Nov21Document302 pagesASM Masters Solved Past Question Papers Solved Numericals From Sept16 Till Nov21arivarasanNo ratings yet

- Marpol Annex 6Document11 pagesMarpol Annex 6tripuraridheerajNo ratings yet

- SireDocument3 pagesSireAmit MishraNo ratings yet

- MSJ41503 - Intro To Maritime ManagementDocument6 pagesMSJ41503 - Intro To Maritime ManagementkjNo ratings yet

- Guide To Vetting Proceed 2017 - Part74 PDFDocument2 pagesGuide To Vetting Proceed 2017 - Part74 PDFQuang Hòa LưuNo ratings yet

- Change of Cargo Grades or Preparation For DrydockDocument3 pagesChange of Cargo Grades or Preparation For DrydockAlice Mano JiamaNo ratings yet

- Procedures and Requirements For Bunker DeliveryDocument1 pageProcedures and Requirements For Bunker DeliveryNano WibowoNo ratings yet

- Cargo Handling Manual - SOE 12k LEG (01-TECHNICAL - 1304275 - 1 - 01) PDFDocument283 pagesCargo Handling Manual - SOE 12k LEG (01-TECHNICAL - 1304275 - 1 - 01) PDFМаксим Шабатын100% (2)

- Bunker Calculation Excel SheetDocument1 pageBunker Calculation Excel SheetJay Narayan TiwariNo ratings yet

- Certificate of Bollard Pull - TRICAHUE IDocument2 pagesCertificate of Bollard Pull - TRICAHUE IRuben Rodriguez100% (1)

- DNV BQS - tcm4-482822Document8 pagesDNV BQS - tcm4-482822captkcNo ratings yet

- A Complete Guide of Loading TDI Onboard A Chemical TankerDocument19 pagesA Complete Guide of Loading TDI Onboard A Chemical TankerKunal Singh100% (1)

- Oldendorff 75 Years PDFDocument242 pagesOldendorff 75 Years PDFJerzy IdzikowskiNo ratings yet

- Gasasa Marine Fuel: Recommendations For Linked Emergency Shutdown (ESD) Arrangements For LNG BunkeringDocument14 pagesGasasa Marine Fuel: Recommendations For Linked Emergency Shutdown (ESD) Arrangements For LNG Bunkeringmhientb100% (1)

- IBS - IMO SEEMP Part II - Template (Blank Form)Document10 pagesIBS - IMO SEEMP Part II - Template (Blank Form)sakis papasNo ratings yet

- International Navigation Limits (Inl) - WarrantiesDocument5 pagesInternational Navigation Limits (Inl) - WarrantiesKonstantinVallasteNo ratings yet

- HSE-07.24 - Appendix XVI - Exhaust Gas Scrubber Management PlanDocument68 pagesHSE-07.24 - Appendix XVI - Exhaust Gas Scrubber Management PlanAndriy100% (1)

- LR - Class - News - 02.2022 MARPOL Ann VI Fuel Oil Sampling PointDocument3 pagesLR - Class - News - 02.2022 MARPOL Ann VI Fuel Oil Sampling PointTomas CasisNo ratings yet

- Imo 2020 Comprehensive Guide v17 PDFDocument28 pagesImo 2020 Comprehensive Guide v17 PDFTianhui HothNo ratings yet

- Act 515 Merchant Shipping Oil Pollution Act 1994Document34 pagesAct 515 Merchant Shipping Oil Pollution Act 1994Adam Haida & Co100% (1)

- SIRE Observations For 2018, 02 Jan'19Document14 pagesSIRE Observations For 2018, 02 Jan'19Romāns BogdanovsNo ratings yet

- Sea Transport of Liquid Chemicals in Bulk PDFDocument131 pagesSea Transport of Liquid Chemicals in Bulk PDFDiana MoralesNo ratings yet

- Classification Society - Capt - Saujanya SinhaDocument3 pagesClassification Society - Capt - Saujanya SinhaJitender MalikNo ratings yet

- MARPOL 12aDocument12 pagesMARPOL 12agmarinovNo ratings yet

- Asian VettingDocument13 pagesAsian Vettingkhaled1160No ratings yet

- Emergency SMPEP SamplePlanDocument36 pagesEmergency SMPEP SamplePlanrigelNo ratings yet

- OsdDocument39 pagesOsdVaishnavi JayakumarNo ratings yet

- Marine Commercial PracticeDocument26 pagesMarine Commercial Practicekukuriku13No ratings yet

- NOx Technical Code 2008Document101 pagesNOx Technical Code 2008Joshua LindsayNo ratings yet

- Pilot CardJuayanh 2Document2 pagesPilot CardJuayanh 2sarora_usNo ratings yet

- 5.16 Vegetable OilsDocument10 pages5.16 Vegetable OilsHimanshu KumarNo ratings yet

- Understanding Conventions, Protocols & Amendments: International Maritime Organization (IMO)Document3 pagesUnderstanding Conventions, Protocols & Amendments: International Maritime Organization (IMO)sbdmanNo ratings yet

- From T-2 to Supertanker: Development of the Oil Tanker, 1940 - 2000, RevisedFrom EverandFrom T-2 to Supertanker: Development of the Oil Tanker, 1940 - 2000, RevisedNo ratings yet

- North Korea Conflict: International Industry Research and Economics DepartmentDocument9 pagesNorth Korea Conflict: International Industry Research and Economics DepartmentPeter PandaNo ratings yet

- 2017 MIP Report China Online EdtechDocument29 pages2017 MIP Report China Online EdtechPeter PandaNo ratings yet

- What Happens To Chinese Oil If US-North Korea War Erupts - This Week in Asia - South China Morning PostDocument6 pagesWhat Happens To Chinese Oil If US-North Korea War Erupts - This Week in Asia - South China Morning PostPeter PandaNo ratings yet

- BVCA Guide To Corporate Venture CapitalDocument16 pagesBVCA Guide To Corporate Venture CapitalPeter PandaNo ratings yet

- IO Ethanol 2018 enDocument7 pagesIO Ethanol 2018 enPeter PandaNo ratings yet

- Characteristics: C5 Petrochemical ProductDocument3 pagesCharacteristics: C5 Petrochemical ProductPeter PandaNo ratings yet

- News Articles 2018-01-16 The-Flow-OfDocument5 pagesNews Articles 2018-01-16 The-Flow-OfPeter PandaNo ratings yet

- Thai NessDocument17 pagesThai NessPeter PandaNo ratings yet

- mati08-2537 มติคณะกรรมการสิ่งแวดล้อมDocument4 pagesmati08-2537 มติคณะกรรมการสิ่งแวดล้อมPeter PandaNo ratings yet

- Role Play Scenario 1:: Group No. .Document1 pageRole Play Scenario 1:: Group No. .Peter PandaNo ratings yet

- Evaluation Form For MassageDocument1 pageEvaluation Form For MassagePeter PandaNo ratings yet

- Christie's Launches Sale of Western Art in Hong Kong To Test Asian Demand - South China Morning PostDocument3 pagesChristie's Launches Sale of Western Art in Hong Kong To Test Asian Demand - South China Morning PostPeter PandaNo ratings yet

- LucerneDocument52 pagesLucernePeter PandaNo ratings yet

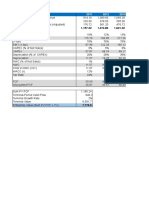

- Total Revenue 1,157.32 1,374.80 1,621.32: (Unit: Million USD)Document6 pagesTotal Revenue 1,157.32 1,374.80 1,621.32: (Unit: Million USD)Peter PandaNo ratings yet

- Brexit: A Look at The Repercussions of Britain's Possible Exit From The European UnionDocument17 pagesBrexit: A Look at The Repercussions of Britain's Possible Exit From The European UnionPeter PandaNo ratings yet

- EMS Final-Printing PDFDocument16 pagesEMS Final-Printing PDFJason SmithNo ratings yet

- Data Logging Test Commisioning: Intake-Raw Water Out ClarifierDocument1 pageData Logging Test Commisioning: Intake-Raw Water Out ClarifierIevans SopianNo ratings yet

- Expository Essay - Global Warming 2Document4 pagesExpository Essay - Global Warming 2Ong Szechuan67% (9)

- Personal StatementDocument2 pagesPersonal Statementapi-31804529371% (7)

- 04.4 (English) Judgement T-291-09 of The Constitutional Court of ColombiaDocument109 pages04.4 (English) Judgement T-291-09 of The Constitutional Court of ColombiaCIVISOL : Fundación para el Cambio SistémicoNo ratings yet

- LIST OF REGISTERED TSDs PDFDocument12 pagesLIST OF REGISTERED TSDs PDFAJ SalazarNo ratings yet

- Economic Sustainability PosterDocument1 pageEconomic Sustainability Posterapi-306606068No ratings yet

- Chemical Sector Life Cycle Metrics GuidanceDocument120 pagesChemical Sector Life Cycle Metrics GuidanceMitziHeresNo ratings yet

- Palm Oil Study Kh0218208enn NewDocument396 pagesPalm Oil Study Kh0218208enn NewAdji Darsoyo100% (1)

- Environmental ProtectionDocument13 pagesEnvironmental ProtectionbekkuNo ratings yet

- Review Mastermind 1, Unit 5 and 6. A) Rewrite The Sentences in The Passive Form. If The Agent Is Not Important, Do Not Include ItDocument4 pagesReview Mastermind 1, Unit 5 and 6. A) Rewrite The Sentences in The Passive Form. If The Agent Is Not Important, Do Not Include ItPaulina AguirreNo ratings yet

- REMU ScreeningBucketDocument12 pagesREMU ScreeningBucketScott GuimondNo ratings yet

- Athish E BA0140011 Role of The Ministry of Environment & ForestsDocument2 pagesAthish E BA0140011 Role of The Ministry of Environment & Forestsaswin don100% (1)

- Presentation On Pre Bid MeetingDocument23 pagesPresentation On Pre Bid MeetinghiveNo ratings yet

- BUNDocument10 pagesBUNJermain BarbadosNo ratings yet

- Mu01 8Document1 pageMu01 8manju.aalawakaNo ratings yet

- Biofilm RemovalDocument5 pagesBiofilm Removaledo wijayantoNo ratings yet

- Ajidew NL-50 AjinomotoDocument3 pagesAjidew NL-50 Ajinomotofajry_uhNo ratings yet

- Environmental Science Draft UpDocument40 pagesEnvironmental Science Draft Uplauriston maraghNo ratings yet

- The Bounty of The SeaDocument3 pagesThe Bounty of The SeaWest Nation100% (2)

- STEM and Sustainablitity in Asia, (Nurul Asyiqin)Document4 pagesSTEM and Sustainablitity in Asia, (Nurul Asyiqin)Nurul Asyiqin Muhd FaizalNo ratings yet

- PROJECTDocument2,449 pagesPROJECTmadhuresh.guptaNo ratings yet

- Hyderabad Heritage RegulationsDocument15 pagesHyderabad Heritage RegulationsIbinshah Shahnavaskhan0% (2)

- Exploring Opportunities For Commercially Sustainable and Climate-Smart Advisory ServicesDocument7 pagesExploring Opportunities For Commercially Sustainable and Climate-Smart Advisory ServicesKushal WaliaNo ratings yet

- Desalting Water Treatment Membrane Manual PDFDocument172 pagesDesalting Water Treatment Membrane Manual PDFCelenia BejaranoNo ratings yet

- NPK SimulatorDocument3 pagesNPK SimulatorEmanuel PataquivaNo ratings yet

- Alkaclean Safety R PDFDocument4 pagesAlkaclean Safety R PDFChetanNo ratings yet

- Concrete Batch CONCRETE BATCH PLANTSPlantsDocument23 pagesConcrete Batch CONCRETE BATCH PLANTSPlantsemorider100% (4)

- Sedicell PDFDocument2 pagesSedicell PDFVineet ChaudharyNo ratings yet

- Proposal For Recycling of Plastic WasteDocument21 pagesProposal For Recycling of Plastic WasteHabiba KhababNo ratings yet