You might also like

- Lone Pine CafeDocument4 pagesLone Pine CafeRahul TiwariNo ratings yet

- Solution For Lone Pine Cafe CaseDocument5 pagesSolution For Lone Pine Cafe CaseShammika Krishna75% (4)

- Lone Pine CafeDocument13 pagesLone Pine CafeCynthia Anggi Maulina100% (1)

- Accounting-Lone Pine Cafe CaseDocument28 pagesAccounting-Lone Pine Cafe CaseMuadz Akbar100% (1)

- Accounting:Text and Cases 2-1 & 2-3Document3 pagesAccounting:Text and Cases 2-1 & 2-3Mon Louie Ferrer100% (5)

- Lone Pine Cafe QuestionDocument2 pagesLone Pine Cafe QuestionSahil JainNo ratings yet

- Case 2-2 Music Mart Balance Sheet 1 OctDocument5 pagesCase 2-2 Music Mart Balance Sheet 1 OctAnubhav Jha100% (3)

- 2-1 Maynard Company (A)Document1 page2-1 Maynard Company (A)Tarry Berry75% (4)

- Maynard Company (A & B)Document9 pagesMaynard Company (A & B)akashnathgarg0% (1)

- 01 Ribbons N' Bows - SolutionDocument4 pages01 Ribbons N' Bows - SolutionShivam Kanojia100% (2)

- ACCOUNTING STERN CORPORATION (A) AnswerDocument4 pagesACCOUNTING STERN CORPORATION (A) AnswerPradina RachmadiniNo ratings yet

- Case Music MartDocument23 pagesCase Music MartDarwin Dionisio Clemente75% (4)

- Lone Pine Cafe SolutionDocument5 pagesLone Pine Cafe SolutionRitu ChhipaNo ratings yet

- QED Electronics - Problem 3.7Document1 pageQED Electronics - Problem 3.7ivanyongforexNo ratings yet

- Case Study 4 - 3 Copies ExpressDocument8 pagesCase Study 4 - 3 Copies ExpressJZ0% (1)

- Case 3.1Document2 pagesCase 3.1Sandeep Agrawal100% (6)

- CASE 4-1 PC DepotDocument7 pagesCASE 4-1 PC Depotkimhyunna75% (4)

- Lewis Corporation Case 6-2 - Group 5Document8 pagesLewis Corporation Case 6-2 - Group 5Om Prakash100% (1)

- Case Study 4 3 Copies ExpressDocument7 pagesCase Study 4 3 Copies Expressamitsemt100% (2)

- Waltham Oil Lube Centre Inc - FinalDocument10 pagesWaltham Oil Lube Centre Inc - Finalerarun2267% (3)

- Case 4 2Document5 pagesCase 4 2Marjorie Morada67% (3)

- Case Report - Grenell FarmDocument5 pagesCase Report - Grenell Farmajsibal100% (1)

- Case 4-4 Waltham Oil & Lube Center, Inc.: $40,000 Deposit With NationalDocument5 pagesCase 4-4 Waltham Oil & Lube Center, Inc.: $40,000 Deposit With NationalCyd Marie VictorianoNo ratings yet

- Campus PizzeriaDocument12 pagesCampus PizzeriaSHIVAM SRIVASTAVANo ratings yet

- Maynard CompanyDocument5 pagesMaynard CompanyNikitha Andrea SaldanhaNo ratings yet

- Maria Hernandez Chemalite and Thumbs Up Case Study FinancialsDocument7 pagesMaria Hernandez Chemalite and Thumbs Up Case Study FinancialsTara AkinteweNo ratings yet

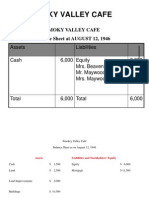

- Smoky Valley CafeDocument3 pagesSmoky Valley Cafemohit_namanNo ratings yet

- Case Forest City Tennis ClubDocument9 pagesCase Forest City Tennis ClubAhmedNiaz100% (1)

- Dispensers of CaliforniaDocument4 pagesDispensers of CaliforniaShweta GautamNo ratings yet

- Problem 2-2: J.L. Gregory CompanyDocument5 pagesProblem 2-2: J.L. Gregory CompanyKAPIL MBA 2021-23 (Delhi)No ratings yet

- Lewis Corporation Assignment Case 6-2 KTMDocument7 pagesLewis Corporation Assignment Case 6-2 KTMSudeep ShahNo ratings yet

- Problem 4-4 Dindorf CompanyDocument5 pagesProblem 4-4 Dindorf Companymelati50% (4)

- Maynard Company (A) : EXHIBIT 1 Account BalancesDocument2 pagesMaynard Company (A) : EXHIBIT 1 Account Balancesriya lakhotiaNo ratings yet

- Income Statements 2010Document10 pagesIncome Statements 2010Shivam GoelNo ratings yet

- Case Baron CoburgDocument8 pagesCase Baron CoburgDarwin Dionisio Clemente100% (2)

- Waltham Oil and Lube CentreDocument5 pagesWaltham Oil and Lube CentreAnirudh Singh0% (2)

- Music Mart SolutionDocument6 pagesMusic Mart SolutionStranger Sinha50% (2)

- Assumptions - : Cash Flow From Operations $ 0Document4 pagesAssumptions - : Cash Flow From Operations $ 0Krish HegdeNo ratings yet

- Waltham Oil and Lube WorkingsDocument5 pagesWaltham Oil and Lube WorkingsGaurav Sahu100% (1)

- Case 9-2 Innovative Engineering CoDocument4 pagesCase 9-2 Innovative Engineering CoFaizal PradhanaNo ratings yet

- Octane Service StationDocument8 pagesOctane Service StationKalyan Kumar83% (6)

- Marion Boats Assignment 2 LatestDocument2 pagesMarion Boats Assignment 2 LatestRakesh SkaiNo ratings yet

- WCM QuestionsDocument5 pagesWCM QuestionsBhavin BaxiNo ratings yet

- Maria HernandezDocument2 pagesMaria HernandezUjwal Suri100% (1)

- Case1 1,1 2,2 1,2 2,2 3,3 1,3 2,4 1,4 2,5 1 pb2 6,3 9Document20 pagesCase1 1,1 2,2 1,2 2,2 3,3 1,3 2,4 1,4 2,5 1 pb2 6,3 9amyth_dude_9090100% (2)

- Problem 3-1Document2 pagesProblem 3-1Omar CirunayNo ratings yet

- Ram Traders - NidhiDocument5 pagesRam Traders - NidhinidhidNo ratings yet

- Dispensers of California Case AnalysisDocument10 pagesDispensers of California Case AnalysisAvinash Singh100% (1)

- Cash Flow StatementDocument4 pagesCash Flow StatementRavina Singh100% (1)

- Problem CH 11 Alfi Dan Yessy AKT 18-MDocument4 pagesProblem CH 11 Alfi Dan Yessy AKT 18-MAna Kristiana100% (1)

- Case 5 Joan Holtz Answer KeyDocument5 pagesCase 5 Joan Holtz Answer KeyVira CastroNo ratings yet

- Grennell Farm SolutionDocument6 pagesGrennell Farm SolutionMichael TorresNo ratings yet

- Case 2-3 Lone Pine Café (A)Document15 pagesCase 2-3 Lone Pine Café (A)Cynthia Anggi Maulina100% (1)

- Lone - Pine - Cafe - Case - Study Final XXDocument25 pagesLone - Pine - Cafe - Case - Study Final XXRamesh SinghNo ratings yet

- Lone Pine CafeDocument16 pagesLone Pine CafeJayraj KhuntiNo ratings yet

- Lone Pine CafeDocument16 pagesLone Pine CafeJayraj KhuntiNo ratings yet

- Basic Concepts of Accounting (Balance Sheet)Document12 pagesBasic Concepts of Accounting (Balance Sheet)badtzmaru0506No ratings yet

- Prepare A Balance Sheet For The Lone Pine Café As of November 2, 2009Document2 pagesPrepare A Balance Sheet For The Lone Pine Café As of November 2, 2009Lynnard Philip PanesNo ratings yet

- Case Study On "The Lone Pine Cafe": Guided by Dr. Ashish MehtaDocument30 pagesCase Study On "The Lone Pine Cafe": Guided by Dr. Ashish MehtaParmvir SinghNo ratings yet

- BD21060 Aman Assignment3Document3 pagesBD21060 Aman Assignment3Aman KundraBD21060No ratings yet

- Label BiruDocument1 pageLabel BiruNadya RizkitaNo ratings yet

- Lone Pine Cafe-CaseDocument28 pagesLone Pine Cafe-CaseNadya Rizkita100% (2)

- Capital Budgeting DCFDocument38 pagesCapital Budgeting DCFNadya Rizkita100% (4)

- Risk FinalDocument26 pagesRisk FinalNadya Rizkita100% (1)

- LaporanmagangDocument46 pagesLaporanmagangNadya RizkitaNo ratings yet

- Euro Land Case SolutionDocument12 pagesEuro Land Case SolutionNadya RizkitaNo ratings yet

- Conclusion: Nadya Rizkita Putri ADocument10 pagesConclusion: Nadya Rizkita Putri ANadya RizkitaNo ratings yet

- Case 2 DCF Analysis - Sindikat 2 (Final - Rev)Document22 pagesCase 2 DCF Analysis - Sindikat 2 (Final - Rev)Nadya RizkitaNo ratings yet

- Investment - LeasingDocument5 pagesInvestment - LeasingNadya RizkitaNo ratings yet

- Primus Case SolutionDocument28 pagesPrimus Case SolutionNadya Rizkita100% (1)

- Resource Allocation and Negotiation ProblemsDocument2 pagesResource Allocation and Negotiation ProblemsNadya RizkitaNo ratings yet

- Investment DetectiveDocument5 pagesInvestment DetectiveNadya Rizkita100% (1)

- Case Selecting SupplierDocument4 pagesCase Selecting SupplierNadya RizkitaNo ratings yet

- Compute and Account For The Initial Capital Contribution of The Partners in The PartnershipDocument5 pagesCompute and Account For The Initial Capital Contribution of The Partners in The PartnershipKathleenNo ratings yet

- Overall Summary:: SAP MM Certified Associate & SAP Certification ID: 0019350978Document6 pagesOverall Summary:: SAP MM Certified Associate & SAP Certification ID: 0019350978Ganapathi RajNo ratings yet

- Capital Gains Tax (Ampongan)Document11 pagesCapital Gains Tax (Ampongan)didit.canonNo ratings yet

- Entrep Q2 SLM Lesson-1Document12 pagesEntrep Q2 SLM Lesson-1akiqt68No ratings yet

- Annexure-VII-GCC - Composite Orders1Document105 pagesAnnexure-VII-GCC - Composite Orders1Bhageerathi SahuNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument7 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalancePDRK BABIUNo ratings yet

- (123doc) Xuat Khau Sua Dau Nanh Vinasoy Sang NhatDocument26 pages(123doc) Xuat Khau Sua Dau Nanh Vinasoy Sang NhatChâu Đặng Thị MinhNo ratings yet

- R15 Firm and Market Structures - Q BankDocument12 pagesR15 Firm and Market Structures - Q Bankakshay mouryaNo ratings yet

- 2 Accounting For MaterialsDocument13 pages2 Accounting For MaterialsZenCamandangNo ratings yet

- ENPL To MSIPL-ENPL SiranchowkDocument1 pageENPL To MSIPL-ENPL SiranchowkDeepak SinghNo ratings yet

- Sample SEP Project ProposalDocument110 pagesSample SEP Project ProposalTonish LangthasaNo ratings yet

- AGM Presentation 2023Document13 pagesAGM Presentation 2023Pratik SankheNo ratings yet

- Fact-Sheet 20191230 08 Idxbumn20 PDFDocument1 pageFact-Sheet 20191230 08 Idxbumn20 PDFvivafatma92No ratings yet

- Henry Sy's SM - History of Shoemart's SupermallsDocument5 pagesHenry Sy's SM - History of Shoemart's SupermallsJen AlvaradeNo ratings yet

- 1 Analysis of FRS 138 Intangible AssetsDocument12 pages1 Analysis of FRS 138 Intangible AssetsWilber Loh100% (1)

- RGPPSEZ - Annual Report - 2022 - ENGDocument149 pagesRGPPSEZ - Annual Report - 2022 - ENGsteveNo ratings yet

- Protigam Food PDFDocument1 pageProtigam Food PDFRay FirdausiNo ratings yet

- TUTORIAL SOLUTIONS (Week 4A)Document8 pagesTUTORIAL SOLUTIONS (Week 4A)Peter100% (1)

- ProjectsDocument4 pagesProjectsMegha KochharNo ratings yet

- Consideration LectureDocument26 pagesConsideration LectureOsamah BakhshNo ratings yet

- Corporate Governance and Bank Performance: Evidence From ZimbabweDocument32 pagesCorporate Governance and Bank Performance: Evidence From ZimbabweMichael NyamutambweNo ratings yet

- FR ACCA Test FullDocument16 pagesFR ACCA Test Fullduducchi2308No ratings yet

- On-Market Cash Offer Text-ONLY ScriptsDocument5 pagesOn-Market Cash Offer Text-ONLY ScriptsHenry100% (1)

- Solved Woldenga Equipment Inc Reported The Figures Shown Below For 2017Document1 pageSolved Woldenga Equipment Inc Reported The Figures Shown Below For 2017Anbu jaromiaNo ratings yet

- Increased Decreased: Sample: Cash in Bank Account Was DebitedDocument3 pagesIncreased Decreased: Sample: Cash in Bank Account Was DebitedAtty Cpa100% (2)

- Individual-Asm3 Pham-Chung ss181258Document3 pagesIndividual-Asm3 Pham-Chung ss181258hoantkss181354No ratings yet

- PNJ Final 2Document22 pagesPNJ Final 2Nguyễn Quỳnh HươngNo ratings yet

- 1 Unit 49 5131 Assignment 1 Brief 2022 FinalDocument8 pages1 Unit 49 5131 Assignment 1 Brief 2022 FinalNguyen HungNo ratings yet

- Company Analysis ReportDocument32 pagesCompany Analysis ReportATREYA NAYAKNo ratings yet

- Entrepreneurship DevelopmentDocument94 pagesEntrepreneurship Developmentashish9dubey-16No ratings yet