You might also like

- TSP 536Document8 pagesTSP 536Dakota WoodwardNo ratings yet

- Special Tax Notice - 999999023Document2 pagesSpecial Tax Notice - 999999023LmoorjaniNo ratings yet

- Certificate of Deposit Account Agreement 2023may31Document12 pagesCertificate of Deposit Account Agreement 2023may31acescamerNo ratings yet

- Fidelity IRA RolloverDocument12 pagesFidelity IRA Rolloverpistolp68No ratings yet

- SSS Webinar Short Term LoanDocument12 pagesSSS Webinar Short Term Loanmelvanne tamboboyNo ratings yet

- LBP6030Document4 pagesLBP6030ismadiNo ratings yet

- Your Rollover OptionsDocument16 pagesYour Rollover OptionsBen SaltzmanNo ratings yet

- Consoloan Application Form 4Document3 pagesConsoloan Application Form 4bhon20No ratings yet

- Oracle FAQsDocument15 pagesOracle FAQsjhakanchanjsrNo ratings yet

- Tax - Questio AnswersDocument7 pagesTax - Questio AnswersAnamika VatsaNo ratings yet

- E Demandnotice 411 A 11Document10 pagesE Demandnotice 411 A 11llukelawrenceNo ratings yet

- E Demandnotice 411 A 11Document10 pagesE Demandnotice 411 A 11Leonardo Zikri ArmandaNo ratings yet

- Special Tax Notice Regarding Plan Payments: Amerco Employee Savings, Profit Sharing, and Employee Stock Ownership PlansDocument2 pagesSpecial Tax Notice Regarding Plan Payments: Amerco Employee Savings, Profit Sharing, and Employee Stock Ownership PlansLarry HosslerNo ratings yet

- Retirement BenefitsDocument8 pagesRetirement Benefitsramineedi6No ratings yet

- Participant Distribution Notice: Plan Name: Spire Savings Plan Plan Number: 75525 Date Generated: December 7, 2022Document10 pagesParticipant Distribution Notice: Plan Name: Spire Savings Plan Plan Number: 75525 Date Generated: December 7, 2022TJ JanssenNo ratings yet

- Thrift Savings Plan TSP-1-C: Catch-Up Contribution ElectionDocument2 pagesThrift Savings Plan TSP-1-C: Catch-Up Contribution ElectionIonut NeacsuNo ratings yet

- TSP Modernization Fact Sheet - May 30, 2019Document3 pagesTSP Modernization Fact Sheet - May 30, 2019FedSmith Inc.60% (5)

- Application For Modified General Purpose Loan: Under Res. No. 21, Series of 2014Document3 pagesApplication For Modified General Purpose Loan: Under Res. No. 21, Series of 2014nemo_nadalNo ratings yet

- Special Tax NoticeDocument6 pagesSpecial Tax Noticeus511No ratings yet

- Amended Salary Loan GuidelinesDocument43 pagesAmended Salary Loan GuidelinesKrizia Iris De MesaNo ratings yet

- Lums Employee Contributory Provident Fund Frequently Asked Questions (Faqs)Document4 pagesLums Employee Contributory Provident Fund Frequently Asked Questions (Faqs)impresiv MNo ratings yet

- Tax Info TSP WithdrawlsDocument8 pagesTax Info TSP WithdrawlsstmccannNo ratings yet

- Compendium For RetireCompendium For Retirees - PdfesDocument64 pagesCompendium For RetireCompendium For Retirees - PdfesGujuNo ratings yet

- Retirement Planning: Iifp - VashiDocument91 pagesRetirement Planning: Iifp - VashiSachin BhoirNo ratings yet

- Know Your Retirement BookletDocument21 pagesKnow Your Retirement BookletPushparajan GunasekaranNo ratings yet

- TCG - 401 (A) Plan Distribution Election Info & FormDocument11 pagesTCG - 401 (A) Plan Distribution Election Info & FormOfficemanager EJNo ratings yet

- TR 0026Document3 pagesTR 0026Cor LeonisNo ratings yet

- Accounting 202 Notes - David HornungDocument28 pagesAccounting 202 Notes - David HornungAvi Goodstein100% (1)

- Fidelity 401kDocument7 pagesFidelity 401kTom BiusoNo ratings yet

- Financial Hardship Benefit Payment Application: ImportantDocument4 pagesFinancial Hardship Benefit Payment Application: Importantkevin mccormacNo ratings yet

- Loan TermsDocument4 pagesLoan TermsNorman FloresNo ratings yet

- General OTSDocument29 pagesGeneral OTSAshish SinghNo ratings yet

- Same For Everyone.: WWW - Sba.govDocument4 pagesSame For Everyone.: WWW - Sba.govScott AtkinsonNo ratings yet

- Description: Tags: cb0113cNDSLClosedEndnewDocument4 pagesDescription: Tags: cb0113cNDSLClosedEndnewanon-854316No ratings yet

- Description: Tags: cb0113cNDSLClosedEndnewDocument4 pagesDescription: Tags: cb0113cNDSLClosedEndnewanon-818545No ratings yet

- NATP TaxPro Monthly September2013Document16 pagesNATP TaxPro Monthly September2013Concha Burciaga HurtadoNo ratings yet

- Pre-EMI CheckDocument5 pagesPre-EMI Checkniraj55singh55No ratings yet

- General Purpose Distribution Request FormDocument19 pagesGeneral Purpose Distribution Request FormWilliamNo ratings yet

- Pention and GratuityDocument19 pagesPention and GratuitygopubooNo ratings yet

- Borrower Information: Disclosure Statement William D. Ford Federal Direct Loan ProgramDocument3 pagesBorrower Information: Disclosure Statement William D. Ford Federal Direct Loan Programthom_evans_2No ratings yet

- Iv. Computation of The Amount of ContributionDocument11 pagesIv. Computation of The Amount of ContributionYoan Baclig BuenoNo ratings yet

- Description: Tags: cb0113dNDSLopenendnewDocument4 pagesDescription: Tags: cb0113dNDSLopenendnewanon-477798No ratings yet

- Citibank - CREDITCARD CONDITIONSDocument8 pagesCitibank - CREDITCARD CONDITIONSkrishna_1238No ratings yet

- Borrower Information: Disclosure Statement William D. Ford Federal Direct Loan ProgramDocument3 pagesBorrower Information: Disclosure Statement William D. Ford Federal Direct Loan ProgramNathan BurrisNo ratings yet

- Information SheetDocument5 pagesInformation SheetShrishNo ratings yet

- Terminal Benefit - Nilam ShahDocument24 pagesTerminal Benefit - Nilam ShahRaghava NarayanaNo ratings yet

- Withdrawals From The EPF AccountDocument2 pagesWithdrawals From The EPF AccountKarunaNo ratings yet

- Salary and Medal New Form2Document3 pagesSalary and Medal New Form2diamajolu gaygons100% (1)

- FORBDocument2 pagesFORBjotav11No ratings yet

- EPF For Construction WorkersDocument10 pagesEPF For Construction WorkersBIJAY KRISHNA DASNo ratings yet

- Same For Everyone.: WWW - Sba.govDocument4 pagesSame For Everyone.: WWW - Sba.govBrady MosherNo ratings yet

- FORMS Conso - Loan PDFDocument3 pagesFORMS Conso - Loan PDFMaramina Matias Roxas - MallariNo ratings yet

- Can NGO Founder Draw A SalaryDocument2 pagesCan NGO Founder Draw A SalaryBibhu Prasad SahuNo ratings yet

- Social Security System: Terms and Conditions For Salary LoanDocument2 pagesSocial Security System: Terms and Conditions For Salary LoanMichael NavosNo ratings yet

- Personal Loan Pre-Approval LetterDocument3 pagesPersonal Loan Pre-Approval LetterJoeLuisAndradeNo ratings yet

- b98324 NikitNavinMistry Offer Letter 20240207 112915Document11 pagesb98324 NikitNavinMistry Offer Letter 20240207 112915nikitnavinmistryNo ratings yet

- Pension Related Q and ADocument2 pagesPension Related Q and Avidhyaa1011No ratings yet

- Direct Tax ProjectDocument18 pagesDirect Tax ProjectShivani Singh ChandelNo ratings yet

- Measuring, Monitoring, and Improving Organizational Health and Organizational Performance in The Context of Evolving Agency Work EnvironmentsDocument19 pagesMeasuring, Monitoring, and Improving Organizational Health and Organizational Performance in The Context of Evolving Agency Work EnvironmentsFedSmith Inc.No ratings yet

- Ernst Letter Re: Remote and TeleworkDocument5 pagesErnst Letter Re: Remote and TeleworkSpencer BrownNo ratings yet

- 2024 Republican Study Committee BudgetDocument167 pages2024 Republican Study Committee BudgetFedSmith Inc.No ratings yet

- 2023.08.01 BRW Letter To OPM Re. Vaccine MandateDocument3 pages2023.08.01 BRW Letter To OPM Re. Vaccine MandateNew York PostNo ratings yet

- 5/18/2023 Letter To Agencies Regarding Expanded TeleworkDocument150 pages5/18/2023 Letter To Agencies Regarding Expanded TeleworkFedSmith Inc.No ratings yet

- 2023.08.01 BRW Letter To DoD Re. Vaccine MandateDocument3 pages2023.08.01 BRW Letter To DoD Re. Vaccine MandateNew York PostNo ratings yet

- Defense Secretary Lloyd Austin Memo Formally Rescinding Military Vaccine MandateDocument2 pagesDefense Secretary Lloyd Austin Memo Formally Rescinding Military Vaccine MandateFedSmith Inc.No ratings yet

- House Committee Raises Concerns About Continued Telework at NASADocument3 pagesHouse Committee Raises Concerns About Continued Telework at NASAFedSmith Inc.No ratings yet

- Kristof v. Air Force 2021-2033Document7 pagesKristof v. Air Force 2021-2033FedSmith Inc.No ratings yet

- No TikTok On Government Devices Implementation GuidanceDocument4 pagesNo TikTok On Government Devices Implementation GuidanceFedSmith Inc.No ratings yet

- Payne Vs BidenDocument16 pagesPayne Vs BidenFedSmith Inc.No ratings yet

- FSC WG Report For 2023 Loc PayDocument29 pagesFSC WG Report For 2023 Loc PayFedSmith Inc.No ratings yet

- Mungo v. Department of The Army CAFC No. 2022-1266Document7 pagesMungo v. Department of The Army CAFC No. 2022-1266FedSmith Inc.No ratings yet

- Senator Joni Ernst Letter Re: Federal Employees Defrauding COVID Relief ProgramsDocument3 pagesSenator Joni Ernst Letter Re: Federal Employees Defrauding COVID Relief ProgramsFedSmith Inc.No ratings yet

- Senators Ask For Commitment From FRTIB Nominees To Withhold TSP Investments in ChinaDocument2 pagesSenators Ask For Commitment From FRTIB Nominees To Withhold TSP Investments in ChinaFedSmith Inc.100% (1)

- 2022 Dismissal and Closure ProceduresDocument54 pages2022 Dismissal and Closure ProceduresFedSmith Inc.No ratings yet

- 2023 GS Pay TablesDocument55 pages2023 GS Pay TablesFedSmith Inc.100% (1)

- Federal Benefits Open Season Highlights 2023 Plan YearDocument12 pagesFederal Benefits Open Season Highlights 2023 Plan YearFedSmith Inc.100% (1)

- 2023 FEHB Plans Where Self Plus One Is Higher Than Self and FamilyDocument5 pages2023 FEHB Plans Where Self Plus One Is Higher Than Self and FamilyFedSmith Inc.No ratings yet

- 2022 Federal Employee Viewpoint Survey ResultsDocument51 pages2022 Federal Employee Viewpoint Survey ResultsFedSmith Inc.100% (1)

- Initial Implementation Guidance For Federal Agencies On Updates To Federal Agency COVID-19 Workplace Safety ProtocolsDocument11 pagesInitial Implementation Guidance For Federal Agencies On Updates To Federal Agency COVID-19 Workplace Safety ProtocolsFedSmith Inc.No ratings yet

- Coy v. Department of The Treasury 2021-2098Document12 pagesCoy v. Department of The Treasury 2021-2098FedSmith Inc.No ratings yet

- Carter v. DOD 2022-1305Document11 pagesCarter v. DOD 2022-1305FedSmith Inc.No ratings yet

- Johnson v. Air Force 2021-1579Document9 pagesJohnson v. Air Force 2021-1579FedSmith Inc.No ratings yet

- 2022 Fehb Significant Plan ChangesDocument11 pages2022 Fehb Significant Plan ChangesFedSmith Inc.100% (1)

- Availability of Sick Leave For Travel To Access Medical CareDocument3 pagesAvailability of Sick Leave For Travel To Access Medical CareFedSmith Inc.No ratings yet

- House Lawmakers Want Federal Facilities To Offer Vegetarian OptionsDocument4 pagesHouse Lawmakers Want Federal Facilities To Offer Vegetarian OptionsFedSmith Inc.No ratings yet

- OPM Guidelines On Parental Bereavement LeaveDocument9 pagesOPM Guidelines On Parental Bereavement LeaveFedSmith Inc.No ratings yet

- The Thrift Savings Plan and IRAsDocument1 pageThe Thrift Savings Plan and IRAsFedSmith Inc.No ratings yet

- United States District Court For The District of ColumbiaDocument15 pagesUnited States District Court For The District of ColumbiaFedSmith Inc.No ratings yet

- Infosys - Q4FY22 - Result Update - Investor ReportDocument10 pagesInfosys - Q4FY22 - Result Update - Investor ReportSavil GuptaNo ratings yet

- Chapter 3 SDocument19 pagesChapter 3 SLê Đăng Cát NhậtNo ratings yet

- IBISWorld Executive Summary Landscaping Services in The USDocument6 pagesIBISWorld Executive Summary Landscaping Services in The USScott LeeNo ratings yet

- FAR - Learning Assessment 2 - For PostingDocument6 pagesFAR - Learning Assessment 2 - For PostingDarlene JacaNo ratings yet

- 1 Latest Latest Manual LatestDocument9 pages1 Latest Latest Manual LatestRohanMohapatraNo ratings yet

- Econ Old Test 2Document7 pagesEcon Old Test 2Homer ViningNo ratings yet

- Bài kiểm tra trắc nghiệm chủ đề - Thanh toán bằng cổ phiếu - - Xem lại bài làmDocument13 pagesBài kiểm tra trắc nghiệm chủ đề - Thanh toán bằng cổ phiếu - - Xem lại bài làmAh TuanNo ratings yet

- 1701A Annual Income Tax ReturnDocument3 pages1701A Annual Income Tax ReturnWa37354No ratings yet

- Poverty in AmericaDocument15 pagesPoverty in Americaapi-481873358100% (1)

- AICPA Newly Released MCQs July'20Document60 pagesAICPA Newly Released MCQs July'20Daljeet Singh100% (1)

- GST - Introduction To GST & Concept of SupplyDocument40 pagesGST - Introduction To GST & Concept of Supplydeepak singhalNo ratings yet

- Earnings Management: A Review of Selected Cases: July 2018Document15 pagesEarnings Management: A Review of Selected Cases: July 2018Andre SetiawanNo ratings yet

- Practice Test 6.7 Revaluation and Impairment 945am Attempt ReviewDocument8 pagesPractice Test 6.7 Revaluation and Impairment 945am Attempt ReviewKRISTINA DENISSE SAN JOSENo ratings yet

- 40 - Section 9 of The Indian Income Tax ActDocument18 pages40 - Section 9 of The Indian Income Tax ActDhirendra SinghNo ratings yet

- Notre Dame Educational Association: Mock Board Examination TaxationDocument10 pagesNotre Dame Educational Association: Mock Board Examination TaxationirishjadeNo ratings yet

- Lecture 6 - Capital Gain 66666Document22 pagesLecture 6 - Capital Gain 66666Malik Muhammad SufyanNo ratings yet

- Gemh 108Document20 pagesGemh 108rekshanaNo ratings yet

- Eldama Ravine Technical: and Vocational CollegeDocument2 pagesEldama Ravine Technical: and Vocational CollegeBen ChelagatNo ratings yet

- 3 Floor, Business & Engineering Building, Matina, Davao City Telefax: (082) 300-1496 Phone No.: (082) 244-34-00 Local 137Document13 pages3 Floor, Business & Engineering Building, Matina, Davao City Telefax: (082) 300-1496 Phone No.: (082) 244-34-00 Local 137Abigail Ann PasiliaoNo ratings yet

- Ahrpv0731f 2013-14Document2 pagesAhrpv0731f 2013-14Shiva KumarNo ratings yet

- ACC202 Principles of Managerial AccountingDocument14 pagesACC202 Principles of Managerial AccountingG JhaNo ratings yet

- Government of Philippine Islands vs. El Hogar FilipinoDocument3 pagesGovernment of Philippine Islands vs. El Hogar FilipinoCharmila SiplonNo ratings yet

- Bessrawl Corporation Is A U S Based Company That Prepares Its ConsolidatedDocument1 pageBessrawl Corporation Is A U S Based Company That Prepares Its ConsolidatedFreelance WorkerNo ratings yet

- Retained EarningsDocument72 pagesRetained EarningsItronix MohaliNo ratings yet

- J Crew LBODocument15 pagesJ Crew LBOTom HoughNo ratings yet

- Sample Document For Practical Training ReportDocument32 pagesSample Document For Practical Training ReportChai Yung Ken100% (1)

- Building Strategy and Performance Through Time: The Critical PathDocument19 pagesBuilding Strategy and Performance Through Time: The Critical PathBusiness Expert PressNo ratings yet

- Int03 Midterm QuizDocument3 pagesInt03 Midterm QuizVincent Larrie MoldezNo ratings yet

- Dhaka Bank ( - ) MTO - 29.09.2017Document6 pagesDhaka Bank ( - ) MTO - 29.09.2017sahadatNo ratings yet

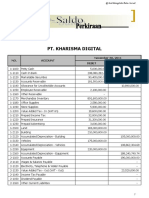

- Kunci Jawaban Pt. Kharisma DigitalDocument91 pagesKunci Jawaban Pt. Kharisma DigitalSanti Mulya100% (3)