You might also like

- Deductiblity of Certain Expenses:: Tax Reference Materials Updated As of 6 February 2014 A. Income TaxDocument1 pageDeductiblity of Certain Expenses:: Tax Reference Materials Updated As of 6 February 2014 A. Income TaxColleen GuimbalNo ratings yet

- REB CoverageDocument2 pagesREB CoverageFlor100% (1)

- Coverage of Examination (Broker)Document2 pagesCoverage of Examination (Broker)Jasielle Leigh UlangkayaNo ratings yet

- Tax II Part 2.1Document3 pagesTax II Part 2.1Gillian Caye Geniza BrionesNo ratings yet

- IAS 12 TaxationDocument158 pagesIAS 12 TaxationAphelele GqadaNo ratings yet

- Diverse - 2023 BIR Form No. 1702RT - REVISED - Page1Document1 pageDiverse - 2023 BIR Form No. 1702RT - REVISED - Page1MOBarcenasNo ratings yet

- Tennessee Valley Authority: FORM 10-KDocument203 pagesTennessee Valley Authority: FORM 10-KDhruba RCNo ratings yet

- Hemant Kumar Agarwal Coi Ay 21-22Document2 pagesHemant Kumar Agarwal Coi Ay 21-22Deepanshu AgarwalNo ratings yet

- Finance Bill 2010Document51 pagesFinance Bill 2010riddhivakhariaNo ratings yet

- Standalone Financial Results, Limited Review Report For June 30, 2016 (Result)Document3 pagesStandalone Financial Results, Limited Review Report For June 30, 2016 (Result)Shyam SunderNo ratings yet

- 1pg Itr SMIIDocument2 pages1pg Itr SMIIRic Dela CruzNo ratings yet

- Tahir Hussain Shah 236 K 12000Document1 pageTahir Hussain Shah 236 K 12000mazharehsan08No ratings yet

- Pa Tax Brief - November 2019Document10 pagesPa Tax Brief - November 2019Teresita TibayanNo ratings yet

- Citizens Charter Mto Arta MC 2020-04 Editable Template 2Document7 pagesCitizens Charter Mto Arta MC 2020-04 Editable Template 2api-541795421No ratings yet

- STX4000 - General Deduction Module - April 2022Document5 pagesSTX4000 - General Deduction Module - April 2022Odzulaho DemanaNo ratings yet

- LAPD-VAT-G03 - VAT 409 Guide For Fixed Property and Construction - External GuideDocument87 pagesLAPD-VAT-G03 - VAT 409 Guide For Fixed Property and Construction - External GuideUrvashi KhedooNo ratings yet

- It 000132223866 2023 01Document1 pageIt 000132223866 2023 01mazharehsan08No ratings yet

- Indian Income Tax Return Acknowledgement: Acknowledgement Number:380069251021023 Date of Filing: 02-Oct-2023Document78 pagesIndian Income Tax Return Acknowledgement: Acknowledgement Number:380069251021023 Date of Filing: 02-Oct-2023Mohit DuhanNo ratings yet

- Mumtaz Khan 236 K 6000Document1 pageMumtaz Khan 236 K 6000mazharehsan08No ratings yet

- Coi 21-22Document2 pagesCoi 21-22Ruloans VaishaliNo ratings yet

- Sales Tax Department: Payment Date CollectorateDocument1 pageSales Tax Department: Payment Date CollectorateSAWERA TEXTILES PVT LTDNo ratings yet

- WHT Plot2Document1 pageWHT Plot2saeed abbasiNo ratings yet

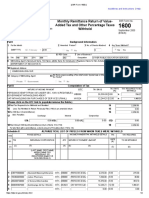

- Bir1600 July52019 - 2 PDFDocument2 pagesBir1600 July52019 - 2 PDFMaureen AlapaapNo ratings yet

- Pa Tax Brief - February 2020Document12 pagesPa Tax Brief - February 2020Teresita TibayanNo ratings yet

- It 000147087234 2024 12Document1 pageIt 000147087234 2024 12Revenue sectionNo ratings yet

- Ifrs 1Document4 pagesIfrs 1SAI TEJANo ratings yet

- Tax ReturnDocument7 pagesTax Returnsyedfaisal_sNo ratings yet

- 1702RT SYNERGETIC TRADING 2023 pg1Document1 page1702RT SYNERGETIC TRADING 2023 pg1RACHEL DAMALERIONo ratings yet

- PDF - 06-12-22 11-19-08Document4 pagesPDF - 06-12-22 11-19-08Jay SharmaNo ratings yet

- Inv 558 PDFDocument4 pagesInv 558 PDFIndia clipNo ratings yet

- Random RelatedDocument2 pagesRandom RelateddurgaNo ratings yet

- Com 22 23Document2 pagesCom 22 23SiddharthNo ratings yet

- Form No. 16A: From ToDocument2 pagesForm No. 16A: From ToAstro Shalleneder GoyalNo ratings yet

- UYLC Income Tax Return For 2022 (1702RT 2018C) - DraftDocument4 pagesUYLC Income Tax Return For 2022 (1702RT 2018C) - DraftVirgelio AbarquezNo ratings yet

- Q1B Memo Without Marks PDFDocument3 pagesQ1B Memo Without Marks PDFFolaNo ratings yet

- Form 20FDocument398 pagesForm 20FNguyen KyNo ratings yet

- It 000147088862 2024 12Document1 pageIt 000147088862 2024 12Revenue sectionNo ratings yet

- It 000142262613 2024 09Document1 pageIt 000142262613 2024 09MUHAMMAD TABRAIZNo ratings yet

- Income Tax Payment Challan: PSID #: 48978159Document1 pageIncome Tax Payment Challan: PSID #: 48978159Abdul SattarNo ratings yet

- Citi Bank 8-Sep-11 17457071 DE1510150 AP1131-9559 Sri Sai RamanaagenciesDocument6 pagesCiti Bank 8-Sep-11 17457071 DE1510150 AP1131-9559 Sri Sai RamanaagenciesEdukondalu PoolaNo ratings yet

- AFFINMAX-AutoPay Template - OkDocument17 pagesAFFINMAX-AutoPay Template - OkPohYeeLiewNo ratings yet

- Chronological OrderDocument5 pagesChronological OrderPhani PitchikaNo ratings yet

- Income Tax Payment Challan: PSID #: 48979834Document1 pageIncome Tax Payment Challan: PSID #: 48979834Abdul SattarNo ratings yet

- It 000147370507 2024 12Document1 pageIt 000147370507 2024 12Revenue sectionNo ratings yet

- AFFINMAX-IBG v2.1 - OkDocument17 pagesAFFINMAX-IBG v2.1 - OkPohYeeLiewNo ratings yet

- It 000147370701 2024 12Document1 pageIt 000147370701 2024 12Revenue sectionNo ratings yet

- AcknowledgementDocument1 pageAcknowledgementaditya_kavangalNo ratings yet

- It 000147370452 2024 12Document1 pageIt 000147370452 2024 12Revenue sectionNo ratings yet

- GSBHDocument2 pagesGSBHSanty Kataria67% (3)

- Forms in GSTDocument11 pagesForms in GSTsagayNo ratings yet

- It 000147370616 2024 12Document1 pageIt 000147370616 2024 12Revenue sectionNo ratings yet

- Nation: MarketDocument9 pagesNation: MarketDebashis MitraNo ratings yet

- Bir Form 1702-RtDocument8 pagesBir Form 1702-RtJonalyn Lapidario100% (2)

- Income Tax Payment Challan: PSID #: 42125287Document1 pageIncome Tax Payment Challan: PSID #: 42125287Muhammad Qaisar LatifNo ratings yet

- It 2023072601012252139Document1 pageIt 2023072601012252139M.TayyabNo ratings yet

- DirectTaxesPaymentPSID UpdateNatureDocument1 pageDirectTaxesPaymentPSID UpdateNatureSkjhkjhkjhNo ratings yet

- EFPS Home - EFiling and Payment SystemDocument2 pagesEFPS Home - EFiling and Payment SystemJinkieNo ratings yet

- Encumbrance FormDocument1 pageEncumbrance FormSree Hari BalajiNo ratings yet

- RR No. 6-2022Document3 pagesRR No. 6-2022chato law officeNo ratings yet

- J.K. Lasser's Your Income Tax 2024: For Preparing Your 2023 Tax ReturnFrom EverandJ.K. Lasser's Your Income Tax 2024: For Preparing Your 2023 Tax ReturnNo ratings yet

- Civil Procedure Cases - Rule 9 To 14Document177 pagesCivil Procedure Cases - Rule 9 To 14Colleen GuimbalNo ratings yet

- Re: Amendment To The DPO Registration Form/s: Organization IndividualDocument1 pageRe: Amendment To The DPO Registration Form/s: Organization Individualbaliao100% (1)

- Our Best Practices - Seeking Legal OpinionDocument1 pageOur Best Practices - Seeking Legal OpinionColleen GuimbalNo ratings yet

- Privacy PolicyDocument5 pagesPrivacy PolicyColleen GuimbalNo ratings yet

- Nature of Work Determines Status As Managerial EmployeeDocument1 pageNature of Work Determines Status As Managerial EmployeeColleen GuimbalNo ratings yet

- Confidentiality and Non-Disclosure Agreement - 0Document2 pagesConfidentiality and Non-Disclosure Agreement - 0Lemuel Bryan Gonzales DenteNo ratings yet

- Barfel CaseDocument2 pagesBarfel CaseColleen GuimbalNo ratings yet

- Begun and Held in Metro Manila, On Monday, The Twenty-Third Day of July, Two Thousand EighteenDocument2 pagesBegun and Held in Metro Manila, On Monday, The Twenty-Third Day of July, Two Thousand EighteenColleen GuimbalNo ratings yet

- (2019) Smuggled Notes - Dimaampao Lecture On Tax Principles and Remedies PDFDocument58 pages(2019) Smuggled Notes - Dimaampao Lecture On Tax Principles and Remedies PDFSteph100% (8)

- BESRDocument16 pagesBESRColleen GuimbalNo ratings yet

- Under The Republic Act 11165Document5 pagesUnder The Republic Act 11165Colleen GuimbalNo ratings yet

- Tax Exemption For Religious InstitutionsDocument1 pageTax Exemption For Religious InstitutionsColleen GuimbalNo ratings yet

- 9A Visa Extension and ProceduresDocument4 pages9A Visa Extension and ProceduresColleen GuimbalNo ratings yet

- Deceptive: AdvertisementDocument10 pagesDeceptive: AdvertisementColleen GuimbalNo ratings yet

- Trusts SyllabusDocument1 pageTrusts SyllabusColleen GuimbalNo ratings yet

- STExDocument6 pagesSTExColleen GuimbalNo ratings yet

- Pollution and Resource DepletionDocument9 pagesPollution and Resource DepletionColleen GuimbalNo ratings yet

- 119242-2003-China Banking Corp. v. Court of AppealsDocument17 pages119242-2003-China Banking Corp. v. Court of AppealsColleen GuimbalNo ratings yet

- Application For Use of FacilitiesDocument2 pagesApplication For Use of FacilitiesColleen GuimbalNo ratings yet

- Job DiscriDocument11 pagesJob DiscriColleen GuimbalNo ratings yet

- Social Responsibility and BusinessDocument35 pagesSocial Responsibility and BusinessColleen GuimbalNo ratings yet

- Felx Go ChanDocument14 pagesFelx Go ChanColleen GuimbalNo ratings yet

- Trusts SyllabusDocument14 pagesTrusts SyllabusColleen GuimbalNo ratings yet

- NotesDocument4 pagesNotesColleen GuimbalNo ratings yet

- Trusts SyllabusDocument1 pageTrusts SyllabusColleen GuimbalNo ratings yet

- Maekk's Leather Organization: 7781 St. Paul Road, San Antonio Village, Makati City 0977 - 008 - 4045Document1 pageMaekk's Leather Organization: 7781 St. Paul Road, San Antonio Village, Makati City 0977 - 008 - 4045Colleen GuimbalNo ratings yet

- 2017 CSCPDSDocument4 pages2017 CSCPDSGillian Bitong AlejandroNo ratings yet

- 2017 CSCPDSDocument1 page2017 CSCPDSColleen GuimbalNo ratings yet

- Start-Up Sample BPDocument54 pagesStart-Up Sample BPsteven100% (1)

- Social Responsibility and BusinessDocument35 pagesSocial Responsibility and BusinessColleen GuimbalNo ratings yet

- Damodaram Sanjivayya National Law University, Sabbavaram, VisakhapatnamDocument21 pagesDamodaram Sanjivayya National Law University, Sabbavaram, VisakhapatnamShruti YadavNo ratings yet

- Principle of Mutuality - A Study: Taxation (Hons.)Document9 pagesPrinciple of Mutuality - A Study: Taxation (Hons.)Ankitha ReddyNo ratings yet

- Notes On Taxation by Ravi-1Document58 pagesNotes On Taxation by Ravi-1akshay yadavNo ratings yet

- Right and Duty of Tax PayerDocument11 pagesRight and Duty of Tax PayerIrshad ShahNo ratings yet

- Questionnaires 1Document143 pagesQuestionnaires 1Renz Joshua Quizon MunozNo ratings yet

- The Impact of Tax Audit and Investigation On Revenue Generation in NigeriaDocument7 pagesThe Impact of Tax Audit and Investigation On Revenue Generation in NigeriaAlexander DeckerNo ratings yet

- BLJPM3369M 2014-15Document2 pagesBLJPM3369M 2014-15jackproewildNo ratings yet

- An Answered Prayer: Ca. Ajay Jain 1 (RTP - Nov 2010 - IPCC)Document18 pagesAn Answered Prayer: Ca. Ajay Jain 1 (RTP - Nov 2010 - IPCC)fansforever9125No ratings yet

- TP StatDocument7 pagesTP Statமணிகண்டன் பிரியாNo ratings yet

- Lowering Personal Income Tax (PIT) : Tax Reform For Acceleration and InclusionDocument4 pagesLowering Personal Income Tax (PIT) : Tax Reform For Acceleration and InclusionChristine Joy RamirezNo ratings yet

- Tax Ordinance-Books 1-30 FCTBDocument51 pagesTax Ordinance-Books 1-30 FCTBRaiha MoriyomNo ratings yet

- Avon Products Manufacturing, Inc. VS CirDocument25 pagesAvon Products Manufacturing, Inc. VS CirEthel Joi Manalac MendozaNo ratings yet

- 0 - Income-Tax-Calculator-FY-2018-19 Final ProformaaDocument9 pages0 - Income-Tax-Calculator-FY-2018-19 Final ProformaaSrinivas PulimamidiNo ratings yet

- Endencia vs. DavidDocument7 pagesEndencia vs. DavidJerry SerapionNo ratings yet

- Theory and Concept o TaxatonDocument18 pagesTheory and Concept o TaxatonDARLENENo ratings yet

- Pre-Test 1 - ProblemsDocument3 pagesPre-Test 1 - ProblemsKenneth Bryan Tegerero TegioNo ratings yet

- Chapter 1 Introduction To Income Tax Act PDFDocument66 pagesChapter 1 Introduction To Income Tax Act PDFRISHI SHAHNo ratings yet

- TyBCom Unipune SyllabusDocument71 pagesTyBCom Unipune SyllabusSangitaNo ratings yet

- Intro To Regular Income TaxationDocument2 pagesIntro To Regular Income TaxationhotgirlsummerNo ratings yet

- Ast TX 901 Fringe Benefits Tax (Batch 22)Document8 pagesAst TX 901 Fringe Benefits Tax (Batch 22)Julious CaalimNo ratings yet

- Mayuri Project 21-8-2019Document54 pagesMayuri Project 21-8-2019amit sharmaNo ratings yet

- Acc 313Document231 pagesAcc 313Bankole MatthewNo ratings yet

- Capital Budgeting - FinmarDocument3 pagesCapital Budgeting - FinmarnerieroseNo ratings yet

- CTA Crim. Case No. O-454Document48 pagesCTA Crim. Case No. O-454Rieland CuevasNo ratings yet

- Tax Review QuestionsDocument11 pagesTax Review QuestionsAbigail Regondola BonitaNo ratings yet

- BC Liberal 2001 Platform CompleteDocument36 pagesBC Liberal 2001 Platform CompleteNRF_VancouverNo ratings yet

- Osmania LLB 3 YDC VI Sem SyllabusDocument8 pagesOsmania LLB 3 YDC VI Sem SyllabusganrgmaNo ratings yet

- 2008 Spring Audit State Developments 2Document285 pages2008 Spring Audit State Developments 2rashidsfNo ratings yet

- Income Taxation 01 Chapter 1 Summary - CompressDocument7 pagesIncome Taxation 01 Chapter 1 Summary - CompressALTHEA REN'EE LIMPAONo ratings yet

- 2 Authority of The Commissioner of Internal RevenueDocument12 pages2 Authority of The Commissioner of Internal RevenueAngel MarieNo ratings yet