You might also like

- Chapter 5 SolutionsDocument16 pagesChapter 5 Solutionshassan.murad60% (5)

- Solutions To Problems: BasicDocument22 pagesSolutions To Problems: BasicSyed AshikNo ratings yet

- Calculating portfolio beta, variance, standard deviation and expected returnsDocument5 pagesCalculating portfolio beta, variance, standard deviation and expected returnsManuel BoahenNo ratings yet

- Chapter 8 Part 2Document7 pagesChapter 8 Part 2abdulraufdghaybeejNo ratings yet

- Principles of Corporate Finance 10th Edition Brealey Solutions ManualDocument14 pagesPrinciples of Corporate Finance 10th Edition Brealey Solutions Manualbrainykabassoullw100% (22)

- Solutions Manual Chapter 22 Estimating Risk Return AssetsDocument13 pagesSolutions Manual Chapter 22 Estimating Risk Return AssetsRonieOlarteNo ratings yet

- Question RISK & RETURNDocument2 pagesQuestion RISK & RETURNQaisar BasheerNo ratings yet

- Solutions For Credit RiskDocument3 pagesSolutions For Credit RiskTuan Tran VanNo ratings yet

- Systematic Risk and The Equity Risk Premium: ER W ER W ERDocument12 pagesSystematic Risk and The Equity Risk Premium: ER W ER W ERLeanne TehNo ratings yet

- E) Investors Demand Higher Expected Rates of Return From Stocks With Returns That Are VeryDocument4 pagesE) Investors Demand Higher Expected Rates of Return From Stocks With Returns That Are Veryssunday giftNo ratings yet

- CH 8 Solutions To Selected End of Chapter Problems4Document9 pagesCH 8 Solutions To Selected End of Chapter Problems4bobhamilton3489No ratings yet

- Company Financial ManagementDocument8 pagesCompany Financial ManagementMiconNo ratings yet

- Return, Risk, and The Security Market LineDocument62 pagesReturn, Risk, and The Security Market LineTushar AroraNo ratings yet

- Investment Assign 2 - QuestionsDocument7 pagesInvestment Assign 2 - QuestionsYuhan KENo ratings yet

- Risk and Rates of Return: Stand-Alone Risk Portfolio Risk Risk & Return: CAPMDocument49 pagesRisk and Rates of Return: Stand-Alone Risk Portfolio Risk Risk & Return: CAPMNazmus Sakib RahatNo ratings yet

- Af 212 - Review Questions 2022 2Document3 pagesAf 212 - Review Questions 2022 2Mwamba HarunaNo ratings yet

- Chapter 5Document23 pagesChapter 5Kenya HunterNo ratings yet

- Tutorial Solutions2-1Document9 pagesTutorial Solutions2-1Yilin YANGNo ratings yet

- Financial Markets Week 2 3Document9 pagesFinancial Markets Week 2 3Jericho DupayaNo ratings yet

- Calculate Portfolio Beta After Stock SaleDocument8 pagesCalculate Portfolio Beta After Stock SaleMiconNo ratings yet

- Examination Paper Portfolio TheoryDocument5 pagesExamination Paper Portfolio TheoryApeksha netlizNo ratings yet

- A01683999 T7Document10 pagesA01683999 T7Bryam CárdenasNo ratings yet

- Tutorial 5 - SolutionDocument6 pagesTutorial 5 - SolutionNg Chun SenfNo ratings yet

- HW5 SolnDocument7 pagesHW5 SolnZhaohui Chen100% (1)

- Risk and ReturnDocument7 pagesRisk and Returnsofia garcinesNo ratings yet

- Total 5 Marks: Question 1 BDocument8 pagesTotal 5 Marks: Question 1 Bshaneice_lewisNo ratings yet

- Ch06 Tool KitDocument36 pagesCh06 Tool KitRoy HemenwayNo ratings yet

- Chapter 06 - Risk & ReturnDocument42 pagesChapter 06 - Risk & Returnmnr81No ratings yet

- CH5 Tutorial ManagementDocument18 pagesCH5 Tutorial ManagementSam Sa100% (1)

- 11 Risks and Rates of Return KEYDocument12 pages11 Risks and Rates of Return KEYkNo ratings yet

- Assignment 3 AnswersDocument8 pagesAssignment 3 Answerstrangnth92No ratings yet

- FIN 301 B Porter Rachna Chapter 8-3 Soln.Document2 pagesFIN 301 B Porter Rachna Chapter 8-3 Soln.Hà My Trần HoàngNo ratings yet

- TUGAS 4 ACCOUNTING FINANCE CHAPTER 8 & 9Document5 pagesTUGAS 4 ACCOUNTING FINANCE CHAPTER 8 & 9safira larasNo ratings yet

- Reading 1 Estimating Market Risk Measures - An Introduction and Overview - AnswersDocument22 pagesReading 1 Estimating Market Risk Measures - An Introduction and Overview - AnswersDivyansh ChandakNo ratings yet

- Lecture 5 - OptimizationDocument6 pagesLecture 5 - Optimizationmzhao8No ratings yet

- Modern Portfolio Theory CH 2Document44 pagesModern Portfolio Theory CH 2preetaNo ratings yet

- Unit 2.1 & 2.2 Risk & ReturnDocument43 pagesUnit 2.1 & 2.2 Risk & ReturnHamdan SheikhNo ratings yet

- FBL5Document12 pagesFBL5FaleeNo ratings yet

- Chapter 8 Portfolio TheoryDocument23 pagesChapter 8 Portfolio TheoryManish ParmarNo ratings yet

- Economy Probability ReturnDocument9 pagesEconomy Probability ReturnMichael CavucaNo ratings yet

- Chapter 11 P7 P10 1617252729Document7 pagesChapter 11 P7 P10 1617252729Dawson Dela CruzNo ratings yet

- Chapter 8 Solutions GitmanDocument22 pagesChapter 8 Solutions GitmanCat Valentine100% (3)

- W2 II C12 Systematic Risk and Equity Risk PremiumDocument12 pagesW2 II C12 Systematic Risk and Equity Risk PremiumSophie LimNo ratings yet

- Risk and Rates of Return: Answers To End-Of-Chapter QuestionsDocument28 pagesRisk and Rates of Return: Answers To End-Of-Chapter QuestionsRizza Mae RodriguezNo ratings yet

- Price (RS.) Probability: Expected Return ERDocument6 pagesPrice (RS.) Probability: Expected Return ERShoaib with rNo ratings yet

- FIN 435 - Exam 2 SlidesDocument157 pagesFIN 435 - Exam 2 SlidesMd. Mehedi HasanNo ratings yet

- Risk and Return AnalysisDocument19 pagesRisk and Return AnalysisFISH JELLYNo ratings yet

- Chapter 5: Risk and ReturnDocument31 pagesChapter 5: Risk and ReturnEyobedNo ratings yet

- Chapter 6: Risk Aversion and Capital Allocation To Risky AssetsDocument14 pagesChapter 6: Risk Aversion and Capital Allocation To Risky AssetsNatalie OngNo ratings yet

- Risk and Return The Capital Asset Pricing Model (Capm)Document47 pagesRisk and Return The Capital Asset Pricing Model (Capm)Bussines LearnNo ratings yet

- Financial Management - 2 Return and Risk: Beg EndDocument6 pagesFinancial Management - 2 Return and Risk: Beg EndYoseph WooNo ratings yet

- Portfolio ManagementDocument4 pagesPortfolio ManagementMahedi HasanNo ratings yet

- Solutions Manual to accompany Introduction to Linear Regression AnalysisFrom EverandSolutions Manual to accompany Introduction to Linear Regression AnalysisRating: 1 out of 5 stars1/5 (1)

- Financial Risk Management: Applications in Market, Credit, Asset and Liability Management and Firmwide RiskFrom EverandFinancial Risk Management: Applications in Market, Credit, Asset and Liability Management and Firmwide RiskNo ratings yet

- Advanced Portfolio Management: A Quant's Guide for Fundamental InvestorsFrom EverandAdvanced Portfolio Management: A Quant's Guide for Fundamental InvestorsNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- The xVA Challenge: Counterparty Credit Risk, Funding, Collateral and CapitalFrom EverandThe xVA Challenge: Counterparty Credit Risk, Funding, Collateral and CapitalNo ratings yet

- Risk-Adjusted Lending Conditions: An Option Pricing ApproachFrom EverandRisk-Adjusted Lending Conditions: An Option Pricing ApproachNo ratings yet

- Counterparty Credit Risk: The new challenge for global financial marketsFrom EverandCounterparty Credit Risk: The new challenge for global financial marketsRating: 2.5 out of 5 stars2.5/5 (2)

- Ch06 Solutions Manual 2015-07-16Document34 pagesCh06 Solutions Manual 2015-07-16Prema Khatwani KesariyaNo ratings yet

- Universiti Teknologi Mara Assignment 3 Project Delivery MethodDocument9 pagesUniversiti Teknologi Mara Assignment 3 Project Delivery MethodBICHAKA MELKAMUNo ratings yet

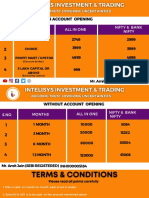

- Intelisys Pricing PlanDocument5 pagesIntelisys Pricing PlanregsNo ratings yet

- Findlay (1988)Document52 pagesFindlay (1988)Roberta Faccin FerreiraNo ratings yet

- Case Study Abstract MC DonaldDocument2 pagesCase Study Abstract MC DonaldpradipkumarpatilNo ratings yet

- Budgeting Problem Set SolutionDocument21 pagesBudgeting Problem Set SolutionJosephThomasNo ratings yet

- OMDocument11 pagesOMThiyagarajanSivaramanNo ratings yet

- Inventory Management in Reliance FreshDocument14 pagesInventory Management in Reliance FreshSabhaya Chirag0% (1)

- Quantity SurveyingDocument27 pagesQuantity SurveyingMagsino, Jubillee SantosNo ratings yet

- 4.export Channels of DistributionDocument24 pages4.export Channels of DistributionRayhan Atunu50% (2)

- EProcurement System Government of IndiaDocument2 pagesEProcurement System Government of IndiaavmrNo ratings yet

- Ias 12Document10 pagesIas 12ImrahNo ratings yet

- Araxxe Whitepaper Revenue Assurance and Digital RevolutionDocument21 pagesAraxxe Whitepaper Revenue Assurance and Digital RevolutionAli babaNo ratings yet

- Atta Hur LTD Prospectus FinalDocument135 pagesAtta Hur LTD Prospectus FinalSarosh NagraNo ratings yet

- Gitman Chapter 14 Divident PolicyDocument59 pagesGitman Chapter 14 Divident PolicyArif SharifNo ratings yet

- 02-2004 Vat Philippine Port Authority PpaDocument3 pages02-2004 Vat Philippine Port Authority Ppaapi-247793055No ratings yet

- Untitled Spreadsheet - Sheet1Document1 pageUntitled Spreadsheet - Sheet1api-430438622No ratings yet

- BAL1103, BBA1103, Principles of EconomicsDocument4 pagesBAL1103, BBA1103, Principles of EconomicsACADEMICS007No ratings yet

- SCA0425R480 (6x4) SpecSheet SAU2016-8-R480 6x4 WEBDocument4 pagesSCA0425R480 (6x4) SpecSheet SAU2016-8-R480 6x4 WEBMATIASNo ratings yet

- Green Marketing: An IntroductionDocument20 pagesGreen Marketing: An IntroductionAbhishek ChaddaNo ratings yet

- Silver Jewellery Market Entry StrategyDocument75 pagesSilver Jewellery Market Entry StrategyPaul Celen0% (2)

- Ciadmin, Journal Manager, 2756-11025-1-CEDocument8 pagesCiadmin, Journal Manager, 2756-11025-1-CEMark Lester MagnayeNo ratings yet

- Final Accounts QuestionsDocument6 pagesFinal Accounts QuestionsGandharva Shankara Murthy100% (1)

- Revisited - The Real Reasons For The Upcoming War in Iraq by William Clark, Updated - Jan 2004Document59 pagesRevisited - The Real Reasons For The Upcoming War in Iraq by William Clark, Updated - Jan 2004سید ہارون حیدر گیلانیNo ratings yet

- Standard Costing AnalysisDocument106 pagesStandard Costing AnalysisUsama RiazNo ratings yet

- 197408hr Intpetrodollar PDFDocument313 pages197408hr Intpetrodollar PDFSank TMNo ratings yet

- Capital Budgeting Techniques for Evaluating Investment ProjectsDocument15 pagesCapital Budgeting Techniques for Evaluating Investment ProjectsSpencer Tañada100% (1)

- James Alm 2Document41 pagesJames Alm 2Jsjs JsjsjjshshNo ratings yet

- Quality Double A4 Copy PaperDocument4 pagesQuality Double A4 Copy PaperStefan DimitrievskiNo ratings yet

- Maths WorksheetDocument7 pagesMaths Worksheetridridrid50% (4)