You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- AP Micro Unit I Practice QuestionsDocument4 pagesAP Micro Unit I Practice QuestionsSunny SinghNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- AP Macroeconomics Assignment: Apply Concepts of AD/AS: SlopingDocument7 pagesAP Macroeconomics Assignment: Apply Concepts of AD/AS: SlopingMadiNo ratings yet

- Personal Financial-PlanningDocument20 pagesPersonal Financial-PlanningGladz De Chavez100% (1)

- Keynes (1936) The General Theory of Employment, Interest and Money. Cambridge B PDFDocument450 pagesKeynes (1936) The General Theory of Employment, Interest and Money. Cambridge B PDFrhroca2762No ratings yet

- Romer Model of Endogenous GrowthDocument3 pagesRomer Model of Endogenous Growthrhroca2762No ratings yet

- Giacomini (2013) The Relationship Between DSGE and VAR Models. CeMMAPDocument30 pagesGiacomini (2013) The Relationship Between DSGE and VAR Models. CeMMAPrhroca2762No ratings yet

- Notes On Macro Economic TheoryDocument362 pagesNotes On Macro Economic TheoryAdrian Yarde BullerNo ratings yet

- Macroeconomic Theory and PolicyDocument320 pagesMacroeconomic Theory and Policymriley@gmail.com100% (17)

- Quao (1982) Asset Market Approach To Exchange Rate Determination. Iowa State UniversityDocument204 pagesQuao (1982) Asset Market Approach To Exchange Rate Determination. Iowa State Universityrhroca2762No ratings yet

- Macroeconomic Theory and Policy (2Nd Edition) : Munich Personal Repec ArchiveDocument247 pagesMacroeconomic Theory and Policy (2Nd Edition) : Munich Personal Repec ArchiveGad AttiasNo ratings yet

- Friedman, Mundell (2001) One World, One MoneyDocument21 pagesFriedman, Mundell (2001) One World, One Moneyrhroca2762No ratings yet

- Angeletos - Macro Intermedia MIT 2013 Geletos - Macro Intermedia MIT 2013-01-02 Introd Solow ModelDocument93 pagesAngeletos - Macro Intermedia MIT 2013 Geletos - Macro Intermedia MIT 2013-01-02 Introd Solow Modelrhroca2762No ratings yet

- Keynes (1936) The General Theory of Employment, Money and Interest Rates PDFDocument263 pagesKeynes (1936) The General Theory of Employment, Money and Interest Rates PDFrhroca2762No ratings yet

- ADM model of economyDocument6 pagesADM model of economyrhroca2762No ratings yet

- Whelan - Endogenous Technological Change. The Romer Model. School of Economics, UCD Autumn 2014 (S) PDFDocument26 pagesWhelan - Endogenous Technological Change. The Romer Model. School of Economics, UCD Autumn 2014 (S) PDFrhroca2762No ratings yet

- Pereyra - What Said The Neoclassical and Endogenous Growth Models About PortugalDocument6 pagesPereyra - What Said The Neoclassical and Endogenous Growth Models About Portugalrhroca2762No ratings yet

- Bah - MacroPrinciples 05 The Public SectorDocument19 pagesBah - MacroPrinciples 05 The Public Sectorrhroca2762No ratings yet

- Aghion Macro2005spring 01 Introd National AccountDocument5 pagesAghion Macro2005spring 01 Introd National Accountrhroca2762No ratings yet

- Annicchiarico (2011) Macroeconomic Modelling and The Effects of Policy Reforms. An Assessment For Italy Using ITEM and QUESTDocument36 pagesAnnicchiarico (2011) Macroeconomic Modelling and The Effects of Policy Reforms. An Assessment For Italy Using ITEM and QUESTrhroca2762No ratings yet

- Bah - MacroPrinciples 01 Economics. The World Around YouDocument5 pagesBah - MacroPrinciples 01 Economics. The World Around Yourhroca2762No ratings yet

- Bah - MacroPrinciples 05 The Public SectorDocument19 pagesBah - MacroPrinciples 05 The Public Sectorrhroca2762No ratings yet

- Bah - MacroPrinciples 03 Markets, Demand and SupplyDocument11 pagesBah - MacroPrinciples 03 Markets, Demand and Supplyrhroca2762No ratings yet

- Bah - MacroPrinciples 04 The Market System and The Private SectorDocument24 pagesBah - MacroPrinciples 04 The Market System and The Private Sectorrhroca2762No ratings yet

- Bah - MacroPrinciples 02 Opportunity Costs and The PPCDocument7 pagesBah - MacroPrinciples 02 Opportunity Costs and The PPCrhroca2762No ratings yet

- Federal Urdu University Islamabad Faculty of Management Sciences Consumption and Savings FunctionDocument14 pagesFederal Urdu University Islamabad Faculty of Management Sciences Consumption and Savings FunctionVampyy GalNo ratings yet

- The German Economic MiracleDocument2 pagesThe German Economic MiracleJonhmark AniñonNo ratings yet

- Practica M IcroDocument13 pagesPractica M Icroelvis ojedaNo ratings yet

- Leaving the Euro: A Practical Guide SummaryDocument3 pagesLeaving the Euro: A Practical Guide SummaryTee RexNo ratings yet

- Balance of Payment ConceptsDocument39 pagesBalance of Payment ConceptsVikku Agarwal100% (1)

- What Is Meant by Protectionism?: Chapter Three: Protectionism and Free TradeDocument4 pagesWhat Is Meant by Protectionism?: Chapter Three: Protectionism and Free TradeBenazir HitoishiNo ratings yet

- Structural Adjustment, Stabilization and Policy ReformDocument105 pagesStructural Adjustment, Stabilization and Policy ReformSumit ShekharNo ratings yet

- Clkassical TheoryDocument8 pagesClkassical Theoryhb proposalNo ratings yet

- Be QBDocument30 pagesBe QBSunny KumarNo ratings yet

- A Tale of Four EconomiesDocument3 pagesA Tale of Four EconomiesAnis NajwaNo ratings yet

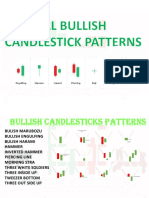

- All Bullish Candlestick Pattern by Optrading00 Telegram Optrading00Document25 pagesAll Bullish Candlestick Pattern by Optrading00 Telegram Optrading00Samitm TamhankarNo ratings yet

- GDP TransactionsDocument8 pagesGDP TransactionsMohamed FoulyNo ratings yet

- Economics Xi Unit-1 Chapter Wise Division of Marks Total TotalDocument10 pagesEconomics Xi Unit-1 Chapter Wise Division of Marks Total TotalPuja BhardwajNo ratings yet

- International Macroeconomics Homework: Fiscal Policy and TradeDocument2 pagesInternational Macroeconomics Homework: Fiscal Policy and TradeMehdi Ben SlimaneNo ratings yet

- The Contemporary World: 02 Worksheet 1Document3 pagesThe Contemporary World: 02 Worksheet 1Ashley AcuñaNo ratings yet

- Hist6ria Do Pensamento Econômico - Carlos AraújoDocument79 pagesHist6ria Do Pensamento Econômico - Carlos AraújoGabriel Soares de Oliveira SantosNo ratings yet

- Business Environment - Indian Economic ReformsDocument17 pagesBusiness Environment - Indian Economic Reformstheanuuradha1993gmaiNo ratings yet

- Global Financial ManagementDocument17 pagesGlobal Financial ManagementMamta GroverNo ratings yet

- Introduction To Applied EconomicsDocument23 pagesIntroduction To Applied EconomicsJfSernioNo ratings yet

- Privatization in IndiaDocument56 pagesPrivatization in IndiaManoj VermaNo ratings yet

- GDP, CPI, Interest Rates TestDocument10 pagesGDP, CPI, Interest Rates TestTrần Toàn100% (1)

- Course Outline in Macroeconomics ECON 122 MWF 2.30 - 3.30 PDFDocument4 pagesCourse Outline in Macroeconomics ECON 122 MWF 2.30 - 3.30 PDFDaphne E DucayNo ratings yet

- Commercial Application ProjectDocument12 pagesCommercial Application ProjectMridul MoolchandaniNo ratings yet

- Trade Invest 2011Document129 pagesTrade Invest 2011chekuswekuNo ratings yet

- © 2010 Pearson Addison-WesleyDocument45 pages© 2010 Pearson Addison-WesleyTariqul IslamNo ratings yet

- JAIBB SyllabusDocument7 pagesJAIBB SyllabuszubishuNo ratings yet

- The Business Cycle and Important Economic MeasuresDocument14 pagesThe Business Cycle and Important Economic Measuresፍቅር ያሸንፋልNo ratings yet