You might also like

- Taxation (Malaysia) : March/June 2018 - Sample QuestionsDocument13 pagesTaxation (Malaysia) : March/June 2018 - Sample QuestionsTeneswari RadhaNo ratings yet

- Taxation (Malaysia) : March/June 2017 - Sample QuestionsDocument12 pagesTaxation (Malaysia) : March/June 2017 - Sample QuestionsIntan SyuhadaNo ratings yet

- Taxation (Malaysia) : September/December 2016 - Sample QuestionsDocument12 pagesTaxation (Malaysia) : September/December 2016 - Sample QuestionsGary Danny Galiyang100% (1)

- Taxation - Malaysia (TX - Mys) : Applied SkillsDocument16 pagesTaxation - Malaysia (TX - Mys) : Applied SkillsPrincess GonzalesNo ratings yet

- m20 ATX MYS QPDocument13 pagesm20 ATX MYS QPizzahderhamNo ratings yet

- P6mys 2017 Sep Dec QDocument12 pagesP6mys 2017 Sep Dec QstacyyauNo ratings yet

- Advanced Taxation (Malaysia) : March/June 2017 - Sample QuestionsDocument12 pagesAdvanced Taxation (Malaysia) : March/June 2017 - Sample QuestionsKiyong TanNo ratings yet

- PYQ AT Sep-Dec2018 PDFDocument11 pagesPYQ AT Sep-Dec2018 PDF炜伦林No ratings yet

- Q-Atxmys-2019-Marjun Sample-Q PDFDocument11 pagesQ-Atxmys-2019-Marjun Sample-Q PDFkok kuan wongNo ratings yet

- Taxation (Malaysia) : Specimen Exam Applicable From December 2015Document22 pagesTaxation (Malaysia) : Specimen Exam Applicable From December 2015cytan828No ratings yet

- F6mys QPDocument14 pagesF6mys QPTenny LeeNo ratings yet

- F6MYS 2013 Dec QuestionDocument14 pagesF6MYS 2013 Dec QuestionChoo LeeNo ratings yet

- Taxation (Malaysia) : Tuesday 3 June 2014Document12 pagesTaxation (Malaysia) : Tuesday 3 June 2014Chan HF PktianNo ratings yet

- Atx June 2016 (Q)Document15 pagesAtx June 2016 (Q)amy najatNo ratings yet

- PT1 Sept 2022 Exams Question Paper G1, G2, G3 22 July 2022Document13 pagesPT1 Sept 2022 Exams Question Paper G1, G2, G3 22 July 2022stacyyauNo ratings yet

- P6mys 2015 Dec QDocument13 pagesP6mys 2015 Dec QMERINANo ratings yet

- J15 F6mys Q PDFDocument20 pagesJ15 F6mys Q PDFAgyeiNo ratings yet

- Taxation (Malaysia) : Tuesday 2 December 2014Document12 pagesTaxation (Malaysia) : Tuesday 2 December 2014cartoon anime انمي100% (1)

- Atx Mock QDocument12 pagesAtx Mock QstacyyauNo ratings yet

- Foundations in Taxation (Malaysia)Document20 pagesFoundations in Taxation (Malaysia)ShazwanieSazaliNo ratings yet

- F6mys Jun 2011 QuDocument10 pagesF6mys Jun 2011 Qutoushiga100% (1)

- Taxation Malaysia Home Acca GlobalDocument12 pagesTaxation Malaysia Home Acca GlobalLee Yee Mei100% (1)

- F6mys 2010 Dec QDocument12 pagesF6mys 2010 Dec QJeejuNo ratings yet

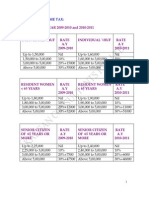

- Tax Rates and AllowancesDocument3 pagesTax Rates and AllowancesChing Seen WongNo ratings yet

- Atx PTDocument15 pagesAtx PTamy najatNo ratings yet

- Taxation (Malaysia) : Monday 7 June 2010Document10 pagesTaxation (Malaysia) : Monday 7 June 2010Saayesha RamNo ratings yet

- F6mys 2008 Jun QDocument9 pagesF6mys 2008 Jun QNik NasuhaNo ratings yet

- F6mys 2009 Dec QDocument10 pagesF6mys 2009 Dec QDave Loh Chong HowNo ratings yet

- Income Tax Rates YA2016Document4 pagesIncome Tax Rates YA2016Kelvin LeongNo ratings yet

- Tax Rates and AllowancesDocument3 pagesTax Rates and AllowancesJong HannahNo ratings yet

- P6mys 2009 Jun QDocument10 pagesP6mys 2009 Jun Qjieling7181No ratings yet

- Taxation (Mock Exam)Document16 pagesTaxation (Mock Exam)shahirah rahimNo ratings yet

- F6-Dec 2007 PYQDocument16 pagesF6-Dec 2007 PYQTan Wan ChingNo ratings yet

- 07 DEC QuestionDocument9 pages07 DEC QuestionkhengmaiNo ratings yet

- 2012 June Q ADocument20 pages2012 June Q AMRspooky321No ratings yet

- Advanced Taxation (Malaysia) : Friday 6 December 2013Document11 pagesAdvanced Taxation (Malaysia) : Friday 6 December 2013MRspooky321No ratings yet

- Advanced Taxation (Malaysia) : Professional Pilot Paper - Options ModuleDocument10 pagesAdvanced Taxation (Malaysia) : Professional Pilot Paper - Options ModuleTeneswari RadhaNo ratings yet

- Chap 6 Relief and RebateDocument15 pagesChap 6 Relief and RebateKelvin OngNo ratings yet

- Tax FinalDocument8 pagesTax FinalAssignments HelperNo ratings yet

- Tax267 AppendixDocument4 pagesTax267 AppendixJasne OczyNo ratings yet

- Notes For Topic 6 Format Tax Computation: Chargeable Income (RM) Calculation (RM) Rate (%) Tax (RM)Document7 pagesNotes For Topic 6 Format Tax Computation: Chargeable Income (RM) Calculation (RM) Rate (%) Tax (RM)Ifa ChanNo ratings yet

- (KMS1013) Assignment 2 by Group 19Document10 pages(KMS1013) Assignment 2 by Group 19Nur Sabrina AfiqahNo ratings yet

- Income Tax NotesDocument4 pagesIncome Tax NotesZaki KhairuddinNo ratings yet

- Example Tax PlanningDocument16 pagesExample Tax PlanningHAZIQ ZIKRI BAHARUDDINNo ratings yet

- Financial Inclusion & Microfinance For Laundry ServicesDocument8 pagesFinancial Inclusion & Microfinance For Laundry ServicesGuneet KohliNo ratings yet

- WK 4 Lecture 4 Personal Taxation Student2033Document10 pagesWK 4 Lecture 4 Personal Taxation Student2033Haananth SubramaniamNo ratings yet

- PFP T8Document7 pagesPFP T8stellaNo ratings yet

- Example 2 - Tax ComputationDocument19 pagesExample 2 - Tax ComputationAminul Islam RubelNo ratings yet

- TaxInformation AspxDocument7 pagesTaxInformation AspxRetno Indri AstutiNo ratings yet

- Question Bank: Errorless Taxation by Ca Pranav Chandak at Pranav Chandak Academy, PuneDocument5 pagesQuestion Bank: Errorless Taxation by Ca Pranav Chandak at Pranav Chandak Academy, PuneSimran MeherNo ratings yet

- 02 RebatesDocument53 pages02 RebatesughaniNo ratings yet

- Genesis 64-11 PDFDocument1 pageGenesis 64-11 PDFRebuild BoholNo ratings yet

- PFP Tutorial 8Document2 pagesPFP Tutorial 8stellaNo ratings yet

- Test 2Document7 pagesTest 2khowcatherine2000No ratings yet

- Examples Salary 2019Document18 pagesExamples Salary 2019Asma ZeeshanNo ratings yet

- Income Tax Calculator FY 2018-19 (AY 2019-20) : Head DescriptionDocument4 pagesIncome Tax Calculator FY 2018-19 (AY 2019-20) : Head DescriptionEr Amit JambhulkarNo ratings yet

- Income TaxDocument5 pagesIncome TaxAshish NarulaNo ratings yet

- Faculty - Accountancy - 2022 - Session 2 - Diploma - Tax317Document12 pagesFaculty - Accountancy - 2022 - Session 2 - Diploma - Tax317Lyana InaniNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Solution Cost and Management Nov 2010Document7 pagesSolution Cost and Management Nov 2010Samuel DwumfourNo ratings yet

- Exercise 6-3Document1 pageExercise 6-3Ammar TuahNo ratings yet

- CertAlarm Certificate FC460P FireClass Photoelectric DetectorDocument3 pagesCertAlarm Certificate FC460P FireClass Photoelectric DetectortbelayinehNo ratings yet

- 2 - m1 Sap OverviewDocument64 pages2 - m1 Sap OverviewOscar Edgar BarreraNo ratings yet

- Cocacola Term PaperDocument6 pagesCocacola Term PaperJanak UpadhyayNo ratings yet

- SMDocument3 pagesSMUmul Banin YousufNo ratings yet

- Material Handling and PackagingDocument30 pagesMaterial Handling and PackagingShivkarVishalNo ratings yet

- Economic Transformation and Governance in Oil Industry Benefits of Liquid Fuels CharterDocument18 pagesEconomic Transformation and Governance in Oil Industry Benefits of Liquid Fuels Charter11soccerdadNo ratings yet

- UTV India Investment CaseDocument3 pagesUTV India Investment CaseRohit ThapliyalNo ratings yet

- Life Cycle CostingDocument34 pagesLife Cycle Costingpednekar30No ratings yet

- Yusen PacketDocument19 pagesYusen PacketBobby Đones0% (2)

- EMPEA CaseStudy OlamDocument2 pagesEMPEA CaseStudy Olamcatiblacki420No ratings yet

- ConvertibleDocument14 pagesConvertibleAkansha JadhavNo ratings yet

- Chapter 16 - Intro To Managerial AccountingDocument46 pagesChapter 16 - Intro To Managerial AccountingEvan Horn0% (1)

- Arts Entrepreneurship, Richard S. ANDREWSDocument139 pagesArts Entrepreneurship, Richard S. ANDREWSRomina S. RomayNo ratings yet

- Quarter 1: Week 3 and 4: Senior High SchoolDocument21 pagesQuarter 1: Week 3 and 4: Senior High SchoolClareen JuneNo ratings yet

- RTM Company ProfileDocument10 pagesRTM Company ProfileBy StandNo ratings yet

- Expand Your Critical ThinkingDocument5 pagesExpand Your Critical ThinkingISLAM KHALED ZSCNo ratings yet

- Muthoot Finance LTDDocument17 pagesMuthoot Finance LTDTushar Dabhade33% (6)

- AR R12 Reversing A Remitted or Cleared ReceiptDocument3 pagesAR R12 Reversing A Remitted or Cleared ReceiptDharan Dhiwahar ManoharanNo ratings yet

- Ug Brochure Masters Union MarchDocument32 pagesUg Brochure Masters Union Marchjawadwafa795No ratings yet

- 0450 Y15 SM 1Document10 pages0450 Y15 SM 1nouraNo ratings yet

- RBL Mitc FinalDocument16 pagesRBL Mitc FinalVivekNo ratings yet

- The Competitive Profile Matrix (CPM) : TotalDocument2 pagesThe Competitive Profile Matrix (CPM) : TotalJay100% (1)

- Starbucks Coffee Company IndianDocument6 pagesStarbucks Coffee Company IndianLatifa Al FadhelNo ratings yet

- Submitted By: Dela Cruz, Janella T. Masters in Business AdministrationDocument21 pagesSubmitted By: Dela Cruz, Janella T. Masters in Business AdministrationAngelica AnneNo ratings yet

- From Complexity To SimplicityDocument48 pagesFrom Complexity To SimplicityJuanCamiloNo ratings yet

- 1 Overview of Project ManagementDocument25 pages1 Overview of Project ManagementDORINNo ratings yet

- Open Bionics LTD Open Bionics Financial Outlook 2023 To 2026Document2 pagesOpen Bionics LTD Open Bionics Financial Outlook 2023 To 2026Dragan SaldzievNo ratings yet

- Research Questionnaire On Indian Overseas Bank Credit Flow ToDocument5 pagesResearch Questionnaire On Indian Overseas Bank Credit Flow ToKrishna Kant PariharNo ratings yet