You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Payment Process Request Status ReportDocument1 pagePayment Process Request Status ReportNishant RanaNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

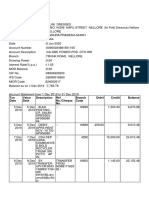

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument5 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalancedileepNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Lehman Brothers - Leverage AnalysisDocument16 pagesLehman Brothers - Leverage Analysisdeepshika kourNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- 49 - Advocates For Truth in Lending Act, Et Al. vs. Bangko Sentral Monetary Board, G.R. No. 192986, January 15, 2013Document2 pages49 - Advocates For Truth in Lending Act, Et Al. vs. Bangko Sentral Monetary Board, G.R. No. 192986, January 15, 2013Gio RuizNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Groupwork 13: Team Gorgeous 3 Chapter 13 Simple Ordinary AnnuityDocument4 pagesGroupwork 13: Team Gorgeous 3 Chapter 13 Simple Ordinary AnnuityAdliana ColinNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- NothingDocument4 pagesNothingSofia Louisse C. FernandezNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Types of Loan: Secured Loan Unsecured LoanDocument17 pagesTypes of Loan: Secured Loan Unsecured Loanadi809hereNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Bank Statement Processing - SAP B1 9.0Document23 pagesBank Statement Processing - SAP B1 9.0Satish Prabhakar DokeNo ratings yet

- MPBFDocument3 pagesMPBFfriendshp_rockzNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Lioyds Bank Statment 3Document4 pagesLioyds Bank Statment 3zainabNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Materi TVM 1 Dan TVM 2 PDFDocument73 pagesMateri TVM 1 Dan TVM 2 PDFamirah muthiaNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Banking Services OperationsDocument134 pagesBanking Services OperationsGuruKPONo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Origin of Rural CreditDocument23 pagesOrigin of Rural Creditnoaman39No ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Banking Laws SummaryDocument100 pagesBanking Laws SummaryJanetGraceDalisayFabreroNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Bank Reconciliation StatementDocument27 pagesBank Reconciliation Statementkimuli FreddieNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Ambit Brochure Core BankingDocument24 pagesAmbit Brochure Core BankingSwati SamantNo ratings yet

- Details of Statement: Tran Id Tran Date Remarks Amount (RS.) Balance (RS.)Document2 pagesDetails of Statement: Tran Id Tran Date Remarks Amount (RS.) Balance (RS.)Ayan DuttaNo ratings yet

- Digi 1306Document5 pagesDigi 1306Suria YSNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Statement PDFDocument3 pagesStatement PDFRodney PattersonNo ratings yet

- Black Slip Deutsche Bank Ag-99euroDocument3 pagesBlack Slip Deutsche Bank Ag-99eurohaleighcrissy49387No ratings yet

- AsDocument4 pagesAsPenchal SaiNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Bank Alfalah Internship Report 2018Document28 pagesBank Alfalah Internship Report 2018Hamza Butt100% (3)

- Development of Banking in NepalDocument4 pagesDevelopment of Banking in Nepaldipendra sharmaNo ratings yet

- Relationship Between Banker and CustomerDocument3 pagesRelationship Between Banker and CustomerEditor IJTSRDNo ratings yet

- Audit of Cash and Cash EquivalentsDocument1 pageAudit of Cash and Cash EquivalentsEmma Mariz Garcia50% (2)

- JC Ramos Law Office: Senior Legal OfficerDocument2 pagesJC Ramos Law Office: Senior Legal OfficerJudeRamosNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Travel Grant Application Form: Courtauld Institute of ArtDocument1 pageTravel Grant Application Form: Courtauld Institute of ArtDorota Jagoda MichalskaNo ratings yet

- Mercial BanksDocument24 pagesMercial BanksBharat ChoudharyNo ratings yet

- AOSRSDocument3 pagesAOSRSvinushasai100% (1)

- Landbank Iaccess Frequently Asked Questions A. Introduction 1. What Is Landbank Iaccess?Document13 pagesLandbank Iaccess Frequently Asked Questions A. Introduction 1. What Is Landbank Iaccess?allanjulesNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)