You might also like

- MCQ 100Document17 pagesMCQ 100Ankit Dubey76% (109)

- Ibbl Investment Portfolio ofDocument47 pagesIbbl Investment Portfolio ofঘুমন্ত বালক100% (2)

- How exchange rates and inflation affect company revenue and costsDocument2 pagesHow exchange rates and inflation affect company revenue and costsAhmed Jan Dahri100% (3)

- MANAGEMENT ADVISORY SERVICES ENGAGEMENTDocument12 pagesMANAGEMENT ADVISORY SERVICES ENGAGEMENTKim Cristian MaañoNo ratings yet

- THE FINANCIAL PERFORMANCE OF INTEREST (Raw Data)Document5 pagesTHE FINANCIAL PERFORMANCE OF INTEREST (Raw Data)Ahmed Jan DahriNo ratings yet

- Identifying The Competitive Strategies of Islamic BanksDocument26 pagesIdentifying The Competitive Strategies of Islamic BanksMohammad AbdullahNo ratings yet

- Irma Kasri Dan N. LukviarmanDocument29 pagesIrma Kasri Dan N. Lukviarmanjaharuddin.hannoverNo ratings yet

- Bakig PerformaceDocument15 pagesBakig PerformaceTahir HanifNo ratings yet

- 5 PDFDocument13 pages5 PDFVictoria MaciasNo ratings yet

- Researchproposalbytakkiddin 100708060115 Phpapp02Document42 pagesResearchproposalbytakkiddin 100708060115 Phpapp02Shikha SinghNo ratings yet

- Islamic Financial System and Conventional Banking: A ComparisonDocument13 pagesIslamic Financial System and Conventional Banking: A ComparisonDenis IoniţăNo ratings yet

- Y 110Document19 pagesY 110Zain Ul AbidinNo ratings yet

- First Security Islami Bank Internship ReportDocument65 pagesFirst Security Islami Bank Internship ReportDurantoDx100% (2)

- F Per 2012 InternationalDocument5 pagesF Per 2012 InternationalBrandy LeeNo ratings yet

- Prospects and Problems of Ibbl-Shahnur Azad Sir IiucDocument20 pagesProspects and Problems of Ibbl-Shahnur Azad Sir IiucZubair Tareq HassanNo ratings yet

- Concept of Profit Measurement and Comparative Study of Islamic FinanceDocument8 pagesConcept of Profit Measurement and Comparative Study of Islamic FinanceMuhammad Mazhar JavedNo ratings yet

- The Use of Discretionary Loan Loss Provisions by Islamic Banks and Conventional Banks in The Middle East RegionDocument23 pagesThe Use of Discretionary Loan Loss Provisions by Islamic Banks and Conventional Banks in The Middle East RegionBudy NuryuliantoNo ratings yet

- The Perfomance Measures of Selected Malaysian and Indonesian Islamic Banks Based On The Maqasid Al-Shari'ah ApproachDocument24 pagesThe Perfomance Measures of Selected Malaysian and Indonesian Islamic Banks Based On The Maqasid Al-Shari'ah ApproachHfz FikrialNo ratings yet

- Bankers' views on Islamic banking growthDocument66 pagesBankers' views on Islamic banking growthmaazwasifNo ratings yet

- Relevancy of Corporate Financial Policies and The Profit Maximization View of Islamic BanksDocument10 pagesRelevancy of Corporate Financial Policies and The Profit Maximization View of Islamic BanksJohn TaskinsoyNo ratings yet

- CCCCDocument27 pagesCCCCNaresh KumarNo ratings yet

- Impact of Interest Rates On Profitability of Islamic and Conventional Banks, PakistanDocument22 pagesImpact of Interest Rates On Profitability of Islamic and Conventional Banks, PakistansyedawwadNo ratings yet

- Age SizeDocument15 pagesAge Size5bwqk54bwhNo ratings yet

- Islamic Bank Retail Management Factors and Customer Knowledge ModelDocument5 pagesIslamic Bank Retail Management Factors and Customer Knowledge ModelasrielNo ratings yet

- Efficiency of Islamic and Conventional Banks in MalaysiaDocument17 pagesEfficiency of Islamic and Conventional Banks in MalaysiaRefky FielnandaNo ratings yet

- Investment Performance of AIBLDocument18 pagesInvestment Performance of AIBLAbu siddiqNo ratings yet

- Comparative Study of Profitability and Liquidity Analysis of Islamic Banks in BangladeshDocument19 pagesComparative Study of Profitability and Liquidity Analysis of Islamic Banks in BangladeshRashel MahmudNo ratings yet

- Ijafb 2019 24 12 07Document17 pagesIjafb 2019 24 12 07Annisa SophiaNo ratings yet

- Islamic Treasury IMALDocument11 pagesIslamic Treasury IMALPrashant VishwakarmaNo ratings yet

- Banking and Audit QualityDocument2 pagesBanking and Audit Qualitybabak84No ratings yet

- DownloadDocument9 pagesDownloadShaik AmanNo ratings yet

- Muslim Perspectives on CSR of Islamic Banks and SMEsDocument25 pagesMuslim Perspectives on CSR of Islamic Banks and SMEsCh ShehzadNo ratings yet

- Causal Relationship Between Islamic and Conventional Banking Instruments in MalaysiaDocument8 pagesCausal Relationship Between Islamic and Conventional Banking Instruments in MalaysiaSihem SissaouiNo ratings yet

- Comparative Analysis of Islamic & Conventional BankingDocument39 pagesComparative Analysis of Islamic & Conventional BankingSharier Mohammad MusaNo ratings yet

- Islamic Banks vs. Conventional Banks in Bangladesh: A Comparative Study Based On Its Efficiency in OperationDocument9 pagesIslamic Banks vs. Conventional Banks in Bangladesh: A Comparative Study Based On Its Efficiency in OperationRoman AhmadNo ratings yet

- The Performance of Malaysian Islamic Bank During 1984-1997: An Exploratory StudyDocument14 pagesThe Performance of Malaysian Islamic Bank During 1984-1997: An Exploratory StudySanorita ShyingNo ratings yet

- 1 PB PDFDocument19 pages1 PB PDFArafat SarderNo ratings yet

- Shariah Issues in The Conversion of Conventional Banking System Into Islamic Banking SystemDocument7 pagesShariah Issues in The Conversion of Conventional Banking System Into Islamic Banking SystemAthirah RazisNo ratings yet

- Islamic Governance, Maqashid Sharia Index Impact Islamic Social ReportingDocument11 pagesIslamic Governance, Maqashid Sharia Index Impact Islamic Social ReportingkautsarNo ratings yet

- 5 - 1 - The Governance, Risk-Taking, and Performance of Islamic Banks - Zscore and ROADocument29 pages5 - 1 - The Governance, Risk-Taking, and Performance of Islamic Banks - Zscore and ROAHarsono Edwin PuspitaNo ratings yet

- Factors Influencing The Profitability of Conventional and Islamic Commercial Banks in GCC CountriesDocument26 pagesFactors Influencing The Profitability of Conventional and Islamic Commercial Banks in GCC CountriesEcho Yang100% (1)

- A1 Fa18 Bba 185 Hamza Kayani BDocument5 pagesA1 Fa18 Bba 185 Hamza Kayani BMuhammad Ameer Hamza KayanNo ratings yet

- Article1380722222 Rehman PDFDocument7 pagesArticle1380722222 Rehman PDFMuhammad Irfan MalikNo ratings yet

- Neila Boulila Taktak (2010)Document18 pagesNeila Boulila Taktak (2010)Putri SariatiNo ratings yet

- Introduction FinalllDocument40 pagesIntroduction FinalllOld PagesNo ratings yet

- Efficiency and Performance PDFDocument17 pagesEfficiency and Performance PDFNadeemNo ratings yet

- Chapter # 1Document48 pagesChapter # 1Atiqul IslamNo ratings yet

- CG in Islamic FinanceDocument4 pagesCG in Islamic FinancehanyfotouhNo ratings yet

- Evaluating The Financial Performance of PDFDocument6 pagesEvaluating The Financial Performance of PDFMehwish ZahoorNo ratings yet

- Factors affecting growth of Islamic Banking in PakistanDocument25 pagesFactors affecting growth of Islamic Banking in PakistanRana AhsanNo ratings yet

- Governance Issues and Islamic BankingDocument8 pagesGovernance Issues and Islamic BankingTmr Gitu LoohNo ratings yet

- Islamic Banking AssignmentDocument3 pagesIslamic Banking AssignmentNadia BaigNo ratings yet

- Customer Satisfaction Towars Islamic BankingDocument9 pagesCustomer Satisfaction Towars Islamic BankingAli Raza SultaniNo ratings yet

- New PDFDocument13 pagesNew PDFRoza RahmanNo ratings yet

- Challenges Facing The Development of Islamic Banking PDFDocument10 pagesChallenges Facing The Development of Islamic Banking PDFAlexander DeckerNo ratings yet

- Isbf - Research Paper - 2021Document22 pagesIsbf - Research Paper - 2021Hurmat Ayub SardarNo ratings yet

- Asset Liability Management of ConventionalDocument20 pagesAsset Liability Management of Conventionalsyakirah-mustaphaNo ratings yet

- Analyse Critique Des Facteurs Bloquant Les Contrats PLS - ImportantDocument18 pagesAnalyse Critique Des Facteurs Bloquant Les Contrats PLS - ImportantyoussefNo ratings yet

- Shariah Governance For Islamic Capital Market: A Step ForwardDocument14 pagesShariah Governance For Islamic Capital Market: A Step ForwardAgustantya ThaibNo ratings yet

- Interet Free Islamic Banks Vs Interest Based Conventional BanksDocument15 pagesInteret Free Islamic Banks Vs Interest Based Conventional BanksabidhasanNo ratings yet

- Banking Governance, Performance and Risk-Taking: Conventional Banks vs Islamic BanksFrom EverandBanking Governance, Performance and Risk-Taking: Conventional Banks vs Islamic BanksNo ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Marketing of Consumer Financial Products: Insights From Service MarketingFrom EverandMarketing of Consumer Financial Products: Insights From Service MarketingNo ratings yet

- Chapter 01 & 02Document6 pagesChapter 01 & 02Ahmed Jan DahriNo ratings yet

- 0416Document4 pages0416Ahmed Jan DahriNo ratings yet

- Nestle coffee supply chain case studyDocument2 pagesNestle coffee supply chain case studyAhmed Jan Dahri100% (1)

- Types of Strategies and Their ExamplesDocument69 pagesTypes of Strategies and Their ExamplesTejashviNo ratings yet

- List of Standalone Islamic Banking Branches of Conventional BanksDocument1 pageList of Standalone Islamic Banking Branches of Conventional BanksAhmed Jan DahriNo ratings yet

- POS Business ExpoDocument2 pagesPOS Business ExpoAhmed Jan Dahri0% (1)

- List of Current Pakistani Federal Ministers and GovernorsDocument1 pageList of Current Pakistani Federal Ministers and GovernorsAhmed Jan DahriNo ratings yet

- Answers To Venn Diagram ProblemsDocument2 pagesAnswers To Venn Diagram ProblemsFelix LlameraNo ratings yet

- 0409Document4 pages0409Ahmed Jan DahriNo ratings yet

- Risk MarketingDocument2 pagesRisk MarketingAhmed Jan DahriNo ratings yet

- Functions of MarketingDocument3 pagesFunctions of MarketingAhmed Jan Dahri100% (1)

- List of Standalone Islamic Banking Branches of Conventional Banks of PakistanDocument1 pageList of Standalone Islamic Banking Branches of Conventional Banks of PakistanAhmed Jan DahriNo ratings yet

- MGT211 GDB SolutionDocument1 pageMGT211 GDB SolutionAhmed Jan DahriNo ratings yet

- Apple Inc., Current Ratio, Long-Term Trends, Comparison To Technology IndustryDocument1 pageApple Inc., Current Ratio, Long-Term Trends, Comparison To Technology IndustryAhmed Jan DahriNo ratings yet

- Sample Dataset 2014Document30 pagesSample Dataset 2014Ahmed Jan DahriNo ratings yet

- Sample Dataset 2014Document30 pagesSample Dataset 2014Ahmed Jan DahriNo ratings yet

- Financial Ratio Analysis of Himalayan Bank LimitedDocument23 pagesFinancial Ratio Analysis of Himalayan Bank LimitedAhmed Jan Dahri0% (1)

- Portersfiveforcestrategy 131215101901 Phpapp01Document9 pagesPortersfiveforcestrategy 131215101901 Phpapp01Ahmed Jan DahriNo ratings yet

- CocaDocument1 pageCocaAhmed Jan DahriNo ratings yet

- Microsoft's $25 Billion Money Market PresenceDocument43 pagesMicrosoft's $25 Billion Money Market PresenceAhmed Jan Dahri100% (1)

- Capital MarketDocument41 pagesCapital MarketAhmed Jan DahriNo ratings yet

- Lecture 9 PDFDocument54 pagesLecture 9 PDFAhmed Jan DahriNo ratings yet

- Chapter 11 explores money market instrumentsDocument34 pagesChapter 11 explores money market instrumentsAhmed Jan DahriNo ratings yet

- Lecture 9 PDFDocument54 pagesLecture 9 PDFAhmed Jan DahriNo ratings yet

- Chapter 11 explores money market instrumentsDocument34 pagesChapter 11 explores money market instrumentsAhmed Jan DahriNo ratings yet

- Conduct of Monetary Policy by MisikinDocument44 pagesConduct of Monetary Policy by MisikinAhmed Jan DahriNo ratings yet

- IIMMDocument24 pagesIIMMarun1974No ratings yet

- Accounting Chapter 2Document56 pagesAccounting Chapter 2hnhNo ratings yet

- Residual Land Valuation MethodDocument32 pagesResidual Land Valuation MethodNabilNo ratings yet

- Foundations of Financial Management 15th Edition Block Solutions ManualDocument35 pagesFoundations of Financial Management 15th Edition Block Solutions Manualwinifredholmesl39o6z100% (22)

- Home OfficeDocument4 pagesHome OfficeVenessa Lei Tricia G. JimenezNo ratings yet

- QUIZ W1 W3 MaterialsDocument11 pagesQUIZ W1 W3 MaterialsLady BirdNo ratings yet

- Annual Report: National Statistics Office, Malta 2012Document76 pagesAnnual Report: National Statistics Office, Malta 2012tomisnellmanNo ratings yet

- Income Tax Pointers for Finals TAX 301Document4 pagesIncome Tax Pointers for Finals TAX 301Jana RamosNo ratings yet

- ITC E-ChoupalDocument23 pagesITC E-ChoupalRick Ganguly100% (1)

- Notes in Business CombinationDocument5 pagesNotes in Business CombinationEllen BuenafeNo ratings yet

- Valuation ProblemsDocument2 pagesValuation ProblemsashviniNo ratings yet

- NPI Introduction W Energy AdvisoryDocument3 pagesNPI Introduction W Energy AdvisoryDev DuttNo ratings yet

- Buying and Selling: and Net Profit/LossDocument19 pagesBuying and Selling: and Net Profit/LossMarc Graham NacuaNo ratings yet

- Dividend Decision ExplainedDocument8 pagesDividend Decision ExplainedVishal TanwarNo ratings yet

- BS INFO-TECH Concrete Products Business PlanDocument27 pagesBS INFO-TECH Concrete Products Business Planvic2clarionNo ratings yet

- Cash Flow Statement: Final ExamDocument4 pagesCash Flow Statement: Final ExamAiman Abdul QadirNo ratings yet

- Ebook b291 Ab E3i1 Web027466Document40 pagesEbook b291 Ab E3i1 Web027466Graham Burns100% (1)

- Consolidation of Financial StatementsDocument2 pagesConsolidation of Financial StatementsmanojjecrcNo ratings yet

- 2013 - Form 990Document30 pages2013 - Form 990Fred MednickNo ratings yet

- Group Assignment - Questions - RevisedDocument6 pagesGroup Assignment - Questions - Revised31231023949No ratings yet

- Micro Economics Study GuideDocument74 pagesMicro Economics Study GuideAdam RNo ratings yet

- Presentation of FS & Its' AuditingDocument27 pagesPresentation of FS & Its' AuditingTeamAudit Runner GroupNo ratings yet

- Mobile AccessoriesDocument27 pagesMobile AccessoriesDiya BoppandaNo ratings yet

- CH 14Document77 pagesCH 14hartinahNo ratings yet

- Advacc Midterm AssignmentsDocument11 pagesAdvacc Midterm AssignmentsAccounting MaterialsNo ratings yet

- 3D HologramDocument12 pages3D HologramRiza ArdinaNo ratings yet

- CFL's Financial Performance and Corporate Governance AnalysisDocument11 pagesCFL's Financial Performance and Corporate Governance AnalysisHugsNo ratings yet

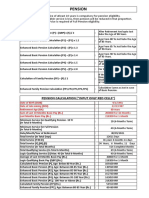

- Pension and Other Retirement BenifitsDocument8 pagesPension and Other Retirement BenifitsVikas GuptaNo ratings yet

- Certain Government Payments: Copy B For RecipientDocument2 pagesCertain Government Payments: Copy B For RecipientDylan Bizier-Conley100% (1)