You might also like

- ACCT203 LeaseDocument4 pagesACCT203 LeaseSweet Emme100% (1)

- CH16HW TrierweilerDocument5 pagesCH16HW TrierweilerMax Trierweiler100% (1)

- Financial PlanningDocument10 pagesFinancial PlanningMuhammad Abbas SandhuNo ratings yet

- Equity Invest - MC Quest.w AnsDocument3 pagesEquity Invest - MC Quest.w AnsElaineJrV-Igot0% (1)

- Latihan PAK Pert 5Document3 pagesLatihan PAK Pert 5Yudi HallimNo ratings yet

- Skye Computer SolutionDocument3 pagesSkye Computer SolutionAashay Shah0% (2)

- Intermediate Accounting 2 Quiz 2: You AnsweredDocument10 pagesIntermediate Accounting 2 Quiz 2: You AnsweredRayman MamakNo ratings yet

- Exercise 7-3 To 7-6Document6 pagesExercise 7-3 To 7-6Nhel AlvaroNo ratings yet

- CH 14Document39 pagesCH 14Iris MaNo ratings yet

- Group 8Document31 pagesGroup 8Jessa E. FabilaneNo ratings yet

- P1 2ND Preboard PDFDocument9 pagesP1 2ND Preboard PDFmaria evangelistaNo ratings yet

- Chapter 7 Test Bank: ©2009 Pearson Education, Inc. Publishing As Prentice Hall 7-1Document29 pagesChapter 7 Test Bank: ©2009 Pearson Education, Inc. Publishing As Prentice Hall 7-1Alfred ValenzuelaNo ratings yet

- Purchase 66,000 Freight-In 1,400 Accounts Payable 67,400Document7 pagesPurchase 66,000 Freight-In 1,400 Accounts Payable 67,400Rhea OraaNo ratings yet

- Inter Branch Transactions: BC - BR 2 HOC Cash BC-BR 1 Cash HOCDocument4 pagesInter Branch Transactions: BC - BR 2 HOC Cash BC-BR 1 Cash HOCCarl Dhaniel Garcia SalenNo ratings yet

- LeasesDocument5 pagesLeasesCamille BacaresNo ratings yet

- Illustrative Problem On Acquisition of Net Assets: Entity XY Entity ABDocument2 pagesIllustrative Problem On Acquisition of Net Assets: Entity XY Entity ABjerald cerezaNo ratings yet

- S SdfafdafdafdafDocument8 pagesS SdfafdafdafdafMark Domingo MendozaNo ratings yet

- Hmcost3e SM Ch19Document32 pagesHmcost3e SM Ch19jhouvan100% (1)

- Chapter 8-10 Test BankDocument80 pagesChapter 8-10 Test BankELSA SYAFIRA ANANTANo ratings yet

- Quiz AppliedDocument12 pagesQuiz AppliedLharissa Ballesteros100% (1)

- Business Combination - GROUP 1Document4 pagesBusiness Combination - GROUP 1Ejoyce KimNo ratings yet

- Estate Tax Pre TestDocument7 pagesEstate Tax Pre TestAldrin ZolinaNo ratings yet

- Audprob Answer 5 and 6Document2 pagesAudprob Answer 5 and 6venice cambryNo ratings yet

- Review of The Accounting Process Straight Problems Problem 1Document13 pagesReview of The Accounting Process Straight Problems Problem 1angielynNo ratings yet

- Quiz - FA2 Current Liab AP NP With QuestionsDocument1 pageQuiz - FA2 Current Liab AP NP With Questionsjanus lopezNo ratings yet

- Identify The Letter of The Choice That Best Completes The Statement or Answers The QuestionDocument171 pagesIdentify The Letter of The Choice That Best Completes The Statement or Answers The QuestionRengeline LucasNo ratings yet

- 08 Sales Variances StudentDocument11 pages08 Sales Variances StudentWilsonNo ratings yet

- Accounting Sample ProblemsDocument9 pagesAccounting Sample Problemsjoong wanNo ratings yet

- Far (Q)Document14 pagesFar (Q)Jee Pare100% (1)

- 23232424Document15 pages23232424JV De Vera100% (1)

- FAR Preweek (B44)Document10 pagesFAR Preweek (B44)Haydy AntonioNo ratings yet

- Problems: Final Review Intermediate 1Document33 pagesProblems: Final Review Intermediate 1Nguyên NguyễnNo ratings yet

- Chapter 13Document45 pagesChapter 13Léo AudibertNo ratings yet

- Quiz 1 - Midterm ReviewerDocument4 pagesQuiz 1 - Midterm ReviewerJack HererNo ratings yet

- Chapter05 QuestionsDocument28 pagesChapter05 QuestionsaskNo ratings yet

- Acctg. 9 Prefi Quiz 1 KeyDocument3 pagesAcctg. 9 Prefi Quiz 1 KeyRica CatanguiNo ratings yet

- Investments in Equity Securities Problems (Victoria Corporation) Year 1Document12 pagesInvestments in Equity Securities Problems (Victoria Corporation) Year 1Xyza Faye Regalado100% (2)

- Far Review - Notes and Receivable AssessmentDocument6 pagesFar Review - Notes and Receivable AssessmentLuisa Janelle BoquirenNo ratings yet

- Uts - Akm3 - Suci Purnama Devi - F0318108 - E17.9 & P21.13 PDFDocument4 pagesUts - Akm3 - Suci Purnama Devi - F0318108 - E17.9 & P21.13 PDFSuci Purnama Devi100% (1)

- Stocks 142-146Document5 pagesStocks 142-146Rej Patnaan100% (1)

- Accounting Management - Transfer Pricing ExerciseDocument8 pagesAccounting Management - Transfer Pricing ExerciseQueenielyn TagraNo ratings yet

- Reviewer Mas5Document26 pagesReviewer Mas5Joyce Anne MananquilNo ratings yet

- Lessor Discussion U PDFDocument4 pagesLessor Discussion U PDFadmiral spongebobNo ratings yet

- Advanced Accounting PDFDocument14 pagesAdvanced Accounting PDFMarie Christine RamosNo ratings yet

- Use The Following Information To Answer Items 1 To 3:: FARQ 218 Page 1 of 3Document3 pagesUse The Following Information To Answer Items 1 To 3:: FARQ 218 Page 1 of 3Irvin LevieNo ratings yet

- Auditing - MIDTERM EXAMDocument9 pagesAuditing - MIDTERM EXAMmoNo ratings yet

- Cash and Cash Equivalents: Answer: CDocument142 pagesCash and Cash Equivalents: Answer: CGarp BarrocaNo ratings yet

- RESA FAR PreWeek (B43)Document10 pagesRESA FAR PreWeek (B43)MellaniNo ratings yet

- Use The Following Information To Answer Items 1 To 4Document4 pagesUse The Following Information To Answer Items 1 To 4Chris Jay LatibanNo ratings yet

- Major Assessment - Current Liab-MahusayDocument5 pagesMajor Assessment - Current Liab-MahusayJeth Mahusay100% (1)

- All About Cash: Name: Section: Score: ProblemsDocument7 pagesAll About Cash: Name: Section: Score: ProblemsAira Mae Hernandez CabaNo ratings yet

- 2019 100,000 2 200,000 Eps (2020) 410,00/230,000 Eps (2019) 350,000/200,000 2020 100,000 3/12 25,000 120,000 9/12 90,000 115,000 2 230,000Document5 pages2019 100,000 2 200,000 Eps (2020) 410,00/230,000 Eps (2019) 350,000/200,000 2020 100,000 3/12 25,000 120,000 9/12 90,000 115,000 2 230,000XienaNo ratings yet

- What A ProblemDocument4 pagesWhat A ProblemEleazar SalazarNo ratings yet

- P2Document18 pagesP2Robert Jayson UyNo ratings yet

- PQ3 BondsDocument2 pagesPQ3 BondsElla Mae MagbatoNo ratings yet

- Accounting 30 For SetDocument7 pagesAccounting 30 For SetJennywel CaputolanNo ratings yet

- Tugas Pert.1Document3 pagesTugas Pert.1Hari YantoNo ratings yet

- Nisha Nur Aini - 43219110183 - TM 02 - AKM IIDocument11 pagesNisha Nur Aini - 43219110183 - TM 02 - AKM IInisha nuraini100% (1)

- Exercise 18Document9 pagesExercise 18raihan aqilNo ratings yet

- Final Practice ProblemsDocument9 pagesFinal Practice ProblemsQian ZhangNo ratings yet

- Deposits Deposits: IndividualsDocument5 pagesDeposits Deposits: IndividualskaushikNo ratings yet

- Bölümlere Göre Ki̇tap Li̇stesi̇Document94 pagesBölümlere Göre Ki̇tap Li̇stesi̇NanaNanaNo ratings yet

- Kelompok 2 - BITCOIN - TemplatesDocument11 pagesKelompok 2 - BITCOIN - TemplatesSofhiaaaNo ratings yet

- The Adjusting Process: Accounting 26eDocument12 pagesThe Adjusting Process: Accounting 26eVĩnh TríNo ratings yet

- Drawings 4,500: Financial AccountiDocument3 pagesDrawings 4,500: Financial AccountiShamNo ratings yet

- AF210 Final Exam SolutionsDocument17 pagesAF210 Final Exam SolutionsSmriti LalNo ratings yet

- Ss11 646 Corporate FinanceDocument343 pagesSs11 646 Corporate Financed-fbuser-32825803100% (12)

- Axtel IndustriesDocument10 pagesAxtel Industriesmanish jangidNo ratings yet

- BRMDocument211 pagesBRMParthNo ratings yet

- 1.0 Executive Summary: 1.1 ObjectivesDocument5 pages1.0 Executive Summary: 1.1 Objectivesethnan lNo ratings yet

- SolutionsDocument22 pagesSolutionsapi-3817072100% (1)

- 55 - Chapter 6 Exercises With AnswersDocument4 pages55 - Chapter 6 Exercises With Answersgio gioNo ratings yet

- Assignment 001: Fundamentals of Accounting/Answer KeyDocument65 pagesAssignment 001: Fundamentals of Accounting/Answer Keymoncarla lagon83% (6)

- Namra State BankDocument27 pagesNamra State BankNoor MahmoodNo ratings yet

- Shantanu Raj: Seeking Middle Level Assignments in ANY Sector With An Organization of High ReputeDocument2 pagesShantanu Raj: Seeking Middle Level Assignments in ANY Sector With An Organization of High ReputeSushama VermaNo ratings yet

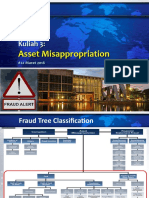

- Asset MisappropriationDocument15 pagesAsset MisappropriationKelas 7-02 D-IV AKTNo ratings yet

- AUDT271+SU+12+ +questions+ +2018Document10 pagesAUDT271+SU+12+ +questions+ +2018ilona gabrielNo ratings yet

- Akuntansi Tugas 4Document2 pagesAkuntansi Tugas 4Biyan ArdanaNo ratings yet

- M/s Auto India Case StudyDocument3 pagesM/s Auto India Case Studyashrin67% (3)

- Grade 09 Paper 2 Mid-Term ExaminationDocument7 pagesGrade 09 Paper 2 Mid-Term ExaminationSarrah ShabbirNo ratings yet

- Chapter 3 FMDocument79 pagesChapter 3 FMHananNo ratings yet

- Chapter2 Statement of Comprehensive IncomeDocument46 pagesChapter2 Statement of Comprehensive IncomeRonald De La Rama100% (1)

- CSIT Problem QuestionsDocument3 pagesCSIT Problem QuestionsQweku TeyeNo ratings yet

- Transfer Pricing ThesisDocument72 pagesTransfer Pricing Thesisfahadsiddiqui100% (1)

- Option PDFDocument4 pagesOption PDFjallwynaldrinNo ratings yet

- Roman Affidavit and Estoppel by Deed ExampleDocument4 pagesRoman Affidavit and Estoppel by Deed Exampleagray43No ratings yet

- This Study Resource Was: MASPW-TheoriesDocument1 pageThis Study Resource Was: MASPW-TheoriesMicaela EncinasNo ratings yet

- Prova Do 2º Ano Present Continuous 3º BiDocument2 pagesProva Do 2º Ano Present Continuous 3º BiRaphael RodriguesNo ratings yet

- The Macroeconomic Impact of Remittances in The Philippines: Lecture No. 8Document41 pagesThe Macroeconomic Impact of Remittances in The Philippines: Lecture No. 8bazgukNo ratings yet