You might also like

- Fault Code 195 Coolant Level Sensor Circuit - Voltage Above Normal or Shorted To High SourceDocument13 pagesFault Code 195 Coolant Level Sensor Circuit - Voltage Above Normal or Shorted To High SourceAhmedmah100% (1)

- Crude DistillationDocument35 pagesCrude DistillationraisNo ratings yet

- Crankpin Failure Study PDFDocument12 pagesCrankpin Failure Study PDFΑθανασιος ΜπεργελεςNo ratings yet

- Definition of Terms - Plumbing2Document15 pagesDefinition of Terms - Plumbing2Gels GenovaNo ratings yet

- 01 - Introduction To Refinery Energy Management NOTE PAGESDocument15 pages01 - Introduction To Refinery Energy Management NOTE PAGESAhmed ElhadyNo ratings yet

- Hysys 2Document85 pagesHysys 2Erick SaLaNo ratings yet

- 2 Stroke Diesel Engine Components-1Document72 pages2 Stroke Diesel Engine Components-1EdemNo ratings yet

- Thermal Oxidiser HazardsDocument14 pagesThermal Oxidiser HazardsMohammed AlShammasiNo ratings yet

- Vessels & Column Tower PipingDocument47 pagesVessels & Column Tower Pipingامین کاظمیNo ratings yet

- Nema Ab 4Document39 pagesNema Ab 4Asif SajwaniNo ratings yet

- MSDS Crude Oil 201311051Document9 pagesMSDS Crude Oil 201311051Hanif Tareq AzierNo ratings yet

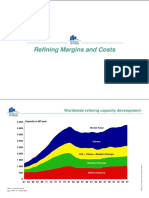

- 20 - Refining Margins and CostsDocument9 pages20 - Refining Margins and CostsBogdanAlinNo ratings yet

- Energy Optimization of Crude Oil Distillation Using Different Designs of Pre-Flash Drums PDFDocument7 pagesEnergy Optimization of Crude Oil Distillation Using Different Designs of Pre-Flash Drums PDFGabriela Urdaneta100% (1)

- 12 - Reforming Catalyst RegenerationDocument17 pages12 - Reforming Catalyst RegenerationCarlos Andres PerezNo ratings yet

- Material Data Safety Sheet Jet A1 ShellDocument10 pagesMaterial Data Safety Sheet Jet A1 ShellAdnan Haji HarbiNo ratings yet

- Chapter13 - ValvblendingDocument28 pagesChapter13 - ValvblendingMarcosNo ratings yet

- NALCO® EC9149A: Section 1. Identification of The Substance/Mixture and of The Company/UndertakingDocument14 pagesNALCO® EC9149A: Section 1. Identification of The Substance/Mixture and of The Company/UndertakingDonatas BertasiusNo ratings yet

- Blending Fuel Gas To Optimize Use of Off-Spec Natural GasDocument13 pagesBlending Fuel Gas To Optimize Use of Off-Spec Natural Gassevero97100% (1)

- Natural Gas Liquefaction Technology For Floating LNG FacilitiesDocument12 pagesNatural Gas Liquefaction Technology For Floating LNG FacilitieshortalemosNo ratings yet

- Heat Transfer Equipment 1. Heat Exchangers: Chemical Engineering DesignDocument45 pagesHeat Transfer Equipment 1. Heat Exchangers: Chemical Engineering DesignMuthuNo ratings yet

- Em FlexicokingDocument8 pagesEm FlexicokingHenry Saenz0% (1)

- Catalyst Passivation For Safer, More Efficient TurnaroundsDocument4 pagesCatalyst Passivation For Safer, More Efficient TurnaroundsAltif AboodNo ratings yet

- Vapor Phase Pressure Drop MethodsDocument32 pagesVapor Phase Pressure Drop MethodsjamestppNo ratings yet

- Getting The Most Out of Data SheetsDocument3 pagesGetting The Most Out of Data SheetskronafNo ratings yet

- Catalytic Reforming PDFDocument7 pagesCatalytic Reforming PDFVu100% (1)

- ML II Application Ethanol BlendingDocument2 pagesML II Application Ethanol BlendingJavierfox98No ratings yet

- DCU Trainingfor New EngineersDocument44 pagesDCU Trainingfor New EngineersDipankar Phukan50% (2)

- 13 - J Gas Purification Sulfur RDocument7 pages13 - J Gas Purification Sulfur RBogdanAlinNo ratings yet

- Visbreaking Unit PDFDocument17 pagesVisbreaking Unit PDFMarcos Maldonado100% (1)

- 19 - Inter Petroleum Markets PDFDocument13 pages19 - Inter Petroleum Markets PDFBogdanAlinNo ratings yet

- Hydrocarbon Recovery v1 0Document39 pagesHydrocarbon Recovery v1 0Adam ShandyNo ratings yet

- Revamps For Ageing Methanol Plants: by Gerard B. Hawkins Managing Director, CEODocument39 pagesRevamps For Ageing Methanol Plants: by Gerard B. Hawkins Managing Director, CEOthirumalaiNo ratings yet

- Vacuum Residue PDFDocument17 pagesVacuum Residue PDFMarcos MaldonadoNo ratings yet

- 2010 Catalysis PDFDocument60 pages2010 Catalysis PDFKevinNo ratings yet

- Environmental Impact Assessment by L.W. CanterDocument38 pagesEnvironmental Impact Assessment by L.W. CanterDewi Hadiwinoto33% (9)

- Fluid Catalytic CrackingDocument16 pagesFluid Catalytic Crackingbubalazi100% (1)

- Chemical Process Retrofitting and Revamping: Techniques and ApplicationsFrom EverandChemical Process Retrofitting and Revamping: Techniques and ApplicationsGade Pandu RangaiahNo ratings yet

- Cci LNG GuideDocument28 pagesCci LNG GuidesabinvargheseNo ratings yet

- 12 - I Hydrorefining ProcessesDocument17 pages12 - I Hydrorefining ProcessesBogdanAlin100% (1)

- 14 - K Overview ConversionDocument41 pages14 - K Overview ConversionBogdanAlinNo ratings yet

- 14 - K Overview ConversionDocument41 pages14 - K Overview ConversionBogdanAlinNo ratings yet

- Catalyst Stripper Improves FCC Unit Performance - PTQ 3Q12Document4 pagesCatalyst Stripper Improves FCC Unit Performance - PTQ 3Q12dionarasimNo ratings yet

- Flare SystemDocument29 pagesFlare SystemLuis EnriqueNo ratings yet

- Hydroprocessing DepropanizerDocument12 pagesHydroprocessing DepropanizerSathish KumarNo ratings yet

- FCC Wash Water SystemsDocument16 pagesFCC Wash Water SystemsBehnam RahzaniNo ratings yet

- Petroleum Economist - Delayed Coking Article PDFDocument4 pagesPetroleum Economist - Delayed Coking Article PDFabhishek kumarNo ratings yet

- Heat ExchangerDocument12 pagesHeat ExchangeremergingengineerNo ratings yet

- The Octane Numbers of Ethanol Blended With Gasoline and Its SurrogatesDocument13 pagesThe Octane Numbers of Ethanol Blended With Gasoline and Its Surrogatesely_hernandez2010No ratings yet

- Control Valve CoefficientsDocument2 pagesControl Valve CoefficientsjroperNo ratings yet

- SMID - 213 - Natural Gas Condensate Sour PDFDocument13 pagesSMID - 213 - Natural Gas Condensate Sour PDFmahdiscribdNo ratings yet

- Flu or Delayed Coking ExperienceDocument5 pagesFlu or Delayed Coking ExperienceLeon SanchezNo ratings yet

- Msdsisomerate Msds Mixed PentanesDocument10 pagesMsdsisomerate Msds Mixed PentanesEmman Patpert KnuckleheadsNo ratings yet

- Pressure-Relief Valve Selection and Transient Pressure ControlDocument8 pagesPressure-Relief Valve Selection and Transient Pressure ControlmaniazharNo ratings yet

- Enviromental Fluid Catalytic Cracking Technology PDFDocument43 pagesEnviromental Fluid Catalytic Cracking Technology PDFNoheilly VásquezNo ratings yet

- 1998 Irving Refinery Hydrocracker Furnace Accident ReportDocument18 pages1998 Irving Refinery Hydrocracker Furnace Accident Reportbazil17No ratings yet

- AFPMQA 2013 DayOneDocument20 pagesAFPMQA 2013 DayOneosmanyukseNo ratings yet

- Princeton Petroleum RefiningDocument30 pagesPrinceton Petroleum RefiningDaniel RedondoNo ratings yet

- Columns: An Introductory Guide To Columns For Chemical EngineersDocument53 pagesColumns: An Introductory Guide To Columns For Chemical EngineersHerawan Mulyanto100% (1)

- Delayed CokerDocument3 pagesDelayed Cokerreach_arindomNo ratings yet

- Bitumen Processing: Crude Unit RevampsDocument10 pagesBitumen Processing: Crude Unit Revampszubair1951No ratings yet

- W4V24 Plastics V2016 HandoutDocument7 pagesW4V24 Plastics V2016 HandoutJessica KingNo ratings yet

- PTQ PTQ: OptimisingDocument124 pagesPTQ PTQ: OptimisingTruth SeekerNo ratings yet

- Shot CokeDocument9 pagesShot CokeaminNo ratings yet

- Unit 3 Steam GenerationDocument30 pagesUnit 3 Steam GenerationkhalimnNo ratings yet

- Gas Processing Plant OperationsDocument15 pagesGas Processing Plant OperationschineduNo ratings yet

- Divided Wall Column 498Document3 pagesDivided Wall Column 498GeorgeNo ratings yet

- Fluid Catalytic Cracking Unit (FCCU)Document1 pageFluid Catalytic Cracking Unit (FCCU)Billy BlinksNo ratings yet

- Coking and Thermal ProcessesDocument8 pagesCoking and Thermal ProcessesWulandariNo ratings yet

- 1 - CL619 RPD - Properties Calculation PDFDocument166 pages1 - CL619 RPD - Properties Calculation PDFPankaj Kumar SainiNo ratings yet

- Mineral Oil and Gas Refineries PETROMDocument12 pagesMineral Oil and Gas Refineries PETROMClaudiu SarcaNo ratings yet

- 5 - B Main Constituents of PetrDocument25 pages5 - B Main Constituents of PetrBogdanAlin100% (1)

- 4 - A Petroleum StatisticsDocument9 pages4 - A Petroleum StatisticsBogdanAlinNo ratings yet

- 3 - Purpose of Refining SchemeDocument1 page3 - Purpose of Refining SchemeBogdanAlinNo ratings yet

- 2011 RefineryConfigurationsDocument8 pages2011 RefineryConfigurationsBogdanAlinNo ratings yet

- RefineryDocument105 pagesRefineryPedro PucheNo ratings yet

- Diesel Fuel Tech ReviewDocument116 pagesDiesel Fuel Tech ReviewLussy MosquedaNo ratings yet

- RefineryDocument105 pagesRefineryPedro PucheNo ratings yet

- RefineryDocument105 pagesRefineryPedro PucheNo ratings yet

- SAPPHIRE® PLUS 70-BarDocument2 pagesSAPPHIRE® PLUS 70-BarAyhan ÖZKALNo ratings yet

- NBC Gear Info.Document8 pagesNBC Gear Info.GLOCK35No ratings yet

- Surge Suppression Air ValvesDocument2 pagesSurge Suppression Air ValvesjyothiprakashNo ratings yet

- Manual-4 6 7Document412 pagesManual-4 6 7Nina Brown100% (1)

- EPIV ValvesDocument2 pagesEPIV ValvesstomakosNo ratings yet

- Will Electric Vehicles Really Create A Cleaner Planet - Thomson ReutersDocument27 pagesWill Electric Vehicles Really Create A Cleaner Planet - Thomson ReutersbsvseyNo ratings yet

- IB Chemistry - HL Topic 3 Questions 1.: (Total 1 Mark)Document11 pagesIB Chemistry - HL Topic 3 Questions 1.: (Total 1 Mark)Aimee KorantengNo ratings yet

- 2008 Product Catalogue PDFDocument255 pages2008 Product Catalogue PDFrenoyaboNo ratings yet

- EN ASFA AU Koplík UV - VIS - Spectrometry PDFDocument12 pagesEN ASFA AU Koplík UV - VIS - Spectrometry PDFJonathanPolaniaOsorioNo ratings yet

- Bombas Centrifugas 60HzDocument329 pagesBombas Centrifugas 60Hzluiscampos77No ratings yet

- PWMcircuit 08Document10 pagesPWMcircuit 08kcarringNo ratings yet

- Always The Right Fuse-LinkDocument38 pagesAlways The Right Fuse-Linke_NomadNo ratings yet

- Eurocode 8-1-3Document18 pagesEurocode 8-1-3joaoNo ratings yet

- Nhce Hydraulic Excavator E505c EvoDocument4 pagesNhce Hydraulic Excavator E505c EvoYew LimNo ratings yet

- Plate Heat Exchanger Model M15-MFG - ASTM B265 Gr1 TitaniumDocument1 pagePlate Heat Exchanger Model M15-MFG - ASTM B265 Gr1 TitaniumCardoso MalacaoNo ratings yet

- Nota Biologi Tingkatan 4 BAB 3Document12 pagesNota Biologi Tingkatan 4 BAB 3Firas Muhammad50% (4)

- Is 6547.1972Document34 pagesIs 6547.1972rajmarathiNo ratings yet

- Single Plane Balance 091401Document16 pagesSingle Plane Balance 091401ridzim4638No ratings yet

- Eg430ndt BrochureDocument2 pagesEg430ndt BrochurePrabha KaranNo ratings yet

- Manual - Ew-Combi Mk2Document8 pagesManual - Ew-Combi Mk2Trần Thùy LinhNo ratings yet

- Xylem Lowara FHE FHS FHF BrochureDocument136 pagesXylem Lowara FHE FHS FHF BrochureDanicaNo ratings yet

- JSW SteelDocument44 pagesJSW Steelauttyhubli100% (1)

- PART 74 Weldolet Sweepolet Something About WeldoletDocument9 pagesPART 74 Weldolet Sweepolet Something About Weldoletravindra_jivaniNo ratings yet