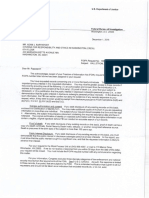

@ _ FEDERAL DEPOSIT INSURANCE CORPORATION, Washington, 0c 20829

SHEILA © BAIR

CHAIRMAN, February 17, 2010

CONFIDENTIAL

Honorable Bob Corker

United States Senate

Washington, D.C. 20510

Dear Senator Corker:

‘Thank you for the opportunity to review the proposed draft of Title {1 on

Enhanced Resolution Authority. | appreciate your willingness to work with me on our

shared goals of ending “too big to fail,” making sure that shareholders and other creditors

will absorb the losses from a failure, and protecting the public. Iam very pleased that the

draft provides the scope of powers necessary to accomplish the mission, while reaching

all market participants ~ including broker-dealers and insurance companies ~ that

contributed to the current crisis

We also support a focused and expedited judicial review process before initiation

ofa FDIC resolution of a large, interconnected non-bank financial firm. As the draft

provides, a review process could be created independent of the bankruptcy courts to

censure that u high hurdle was met before applying the new resolution system. As you

know, in a systemic crisis, quick and decisive action is essential to prevent further

damage to the system, and to ensure that there is never again pressure for a bail-out. This

‘means that any judicial review process must be completed within 24 hours without

further delays from any appeals and, once resolution is approved, the FDIC must be

empowered to act quickly and decisively.

However, | am concemed that the “Supervising Court” proposed in this draft yoes

much further. Instead, it effectively gives this court authority to second guess virtually

all decisions by the FDIC. The draft could empower judges to order specific actions in

the resolution, such as federal funding of creditors, require sales of assets to certain

Parties, and issue injunctions stopping the resolution or the bridge company's operations.

Ifthe new authority is going to be effective, the FDIC must be able to take decisive

action throughout the receivership and bridge company’s operations to limit systemic

risks, while controlling costs. To achieve this, the FDIC"s current process provides broad

authority to act and bars court orders to require or prohibit certain actions. It fully

protects creditors by providing a right to go to court and recover money damages for any

Hinancial losses under the statutory claims priority.

{belive the draft can be restructured relatively simply to provide for judicial

review of the decision to close the financial firm, while giving the FDIC the flexibility

needed to achieve an effective resolution process. To do this, I would recommend edits

to remove the Supervising Counts authority to enter orders stopping or directing the

resolution process (in Section 208(e)), and to clarify the role of the court. For example,

in discussions with bankruptcy attorneys which FDIC staff undertook at the request of

your office, evervone agreed there is parity of treatment of creditors between bankruptcy

and the resolution process. (I hope they are not telling you something different.) To

avoid misunderstandings, we should clarify that all claims against the FDIC, acting as

eceiver or operator for any bridge, be pursued through the claims procedure in Section

204, be limited to money damages, and that the flexibility provided in Section 208 is not

limited by the court approval process. Since it's covered by the claims procedures and

right 10 go to court, there is no need for a special grant of jurisdiction to the Supervising

Court over creditors’ claims in Section 204(a). A few other provisions should be

tightened to accomplish this. These edits can be completed quickly and would provide

full protection to creditors, but allow us to adopt a process that can achieve our shared

goals.

‘The FDIC process is designed to protect financial stability while minimizing costs,

to the government in an orderly wind down, My concem is that authorizing the

Supervising Court to truly supervise, and second guess, resolution decisions leads to a

process like bankruptcy that cannot achieve the speed and cost controls we all want. A

judicial process is designed to resolve competing claims of private parties without

consideration of the public interest and will inevitably be driven by the failed institution's

creditors and the attorneys who represent them, A perfect illustration of the problem is

the Lehman bankruptcy, which created massive market uncertainty, inequity among,

creditors, and has paid out more than $500 million to advisors and attomeys as valuable

assets remain in limbo under bankruptcy jurisdiction and thousands of claims remain

unresolved. If, instead, we provide for judicial approval for the use of the new resolution

process, but limit further court action to adjudication of claims by creditors for money

damages, we can accomplish the goals of a quick and decisive resolution, while

protecting creditors” legitimate interests

Judicial oversight is not needed to protect creditors” legitimate interests. Under

the FDIC's current process creditors have the immediate right to go to court after the

FDIC decides whether to pay or not within defined time periods. Once the creditor goos

to court, the court gives no deference to the FDIC's decision on the claim. [ understand

that some bankruptcy advocates are telling you that constant court oversight is necessary

for “transparency.” To provide additional transparency, we would certainly agree to

regular reporting to the Council, to Congress, and to the public. We already provide

extensive disclosures of our bank resolutions. We pride ourselves on transparency.

If'we limit the Supervising Court to approval of the initiation of the resolution, |

believe we will achieve better management of the financial costs. A court will not have

the same incentives to control costs because it will not be the steward for the fund. In

contrast, financial discipline will be provided by the FDIC as the statutory fund manager

and in its role in collecting risk-based assessments from the industry.

Finally, as a creation of Congress, the FDIC will be much more accountable to

Congress and the Treasury Department than will the judicial branch. In contrast, there

would be much less accountability by a court should it decide to give favored status to

certain creditors, fund certain types of loans, micromanage the bridge bank, or otherwise

pursue an activist agenda which could increase resolution costs. Congress, the FDIC, and

ultimately taxpayers will have no recourse

In summary, we are eager to work with you to streamline this process into one

involving an upfront judicial approval mechanism, while providing the resolution

authority with the flexibility to implement quick action to reduce costs and protect the

public. [have asked my staff to suggest amendments to your draft and will have them to

you shortly.

Jbent

Sincerely,

Cort Fu

Mate ee 7

me

Sheila C. Bair

@ _ FEDERAL DEPOSIT INSURANCE CORPORATION, Wastington, OC 20429

SHEILA ©. BAIR CONFIDENTIAL

CHAIRMAN January 21, 2010

Honorable Bob Corker

Honorable Mark R. Warner

United States Senate

Washington, D.C. 20510

Dear Senators Corker and Wamer:

It was great seeing you both last week. It was good (o hear your current thinking

ona resolution process to end “too big to fail.” 1 very much appreciate the way you have

embraced this as a priority issue. To restore market discipline and reduce the risk of

future failures, we must make clear-by statute-that shareholders and creditors-not the

government-will absorb the losses when large systemic institutions fail because of their

own mismanagement. It is essential that the statutory framework provides for a

“resolution” mechanism” not a “bailout” mechanism; and we will be happy to work with

‘you to avoid language in any legislation that would permit “open institution” support for

hailing firms

I think we all agree that bankruptey should continue to be the primary way to

resolve insolvent firms of all types. I think we also all recognize that in the event of a

failure of a large, inter-connected financial firm, it may be necessary to apply a FDIC-

style resolution to protect the public from systemic disruptions. The question becomes,

‘what should be the trigger for such a resolution and what safeguards would assure its

proper use? Approval by super majorities of the Fed, the FDIC, as well as the Treasury

and the President sets a high hurdle. However, ift is considered essential, | believe a

judicial review process could be created as a second step, pethaps through a special

circuit-court level review independent of the bankruptcy courts

fer careful consideration, I must strongly advise against trying to inject a

bankruptey process as a required “first step” in the resolution mechanism. If a

bankruptey filing must happen first, derivatives counterparties will use their rights under

the Bankruptcy Code to dump their contracts and their associated collateral immediately.

This is allowed by the Bankruptcy Code, and it could precipitate the market collapse we

are trying to avoid. By contrast, under the resolution authority proposals, and the FDI

Act, the FDIC has the ability to prevent termination and dumping of these contracts and

transfer them to another firm or to a bridge firm. This would prevent one of the major

causes of systemic collapses to the financial markets.

Second, the review process must be completed quickly. Financial firms,

particularly the largest financial firms, depend on access to market liquidity. The FDIC-

style resolution process allows immediate creation of a bridge firm to keep operations

going and maintain confidence. However, if action is delayed, funding would dry up,

asset valucs would be lost, and staff would flee. This would greatly reduce the franchise

value of the failed institution, meaning lower recoveries as the institution is broken up

and sold off.

Third, and related to the prior point, we should never provide temporary

‘government funding for a firm already in bankruptcy. (I understand we agree on that

point.) Bankruptcy is designed to protect creditors-not the public and not the

government. Even temporary government funding would allow for enrichment of

creditors and the attorneys who represent them, at the expense of the government, It is

important to note that bankruptcy advocates are on record calling for govemment

funding of a bankruptcy process through the Fed's 13(3) lending authority. I understand

‘you are both opposed to this, but the bankruptcy bar will likely advocate this in the

Judiciary Committee, their committee of jurisdiction. This raises a broader issue of why

the Banking Committee would want to cede jurisdiction to the Judiciary Committee on a

specific resolution mechanism for financial intermediaries. And as we discussed, I very

much fear that the entanglement of the Judiciary Committee on financial services reform

will add a new complication to what is already an uphill battle to get a bill done this year.

Fourth, the bankruptcy process can be inefficient and protracted and itis certainly

not designed to protect the public or the economy. The Lehman insolvency created

massive market uncertainty, inequity among creditors, and illiquidity across the financial

markets. And it continues to drag on, with more than $500 million having already been

paid out to advisors and attomeys. This cannot be our model. The FDIC process is more

efficient than bankruptcy, can be pre-planned unlike the litigated bankrupicy model, and

the FDIC can issue regulations to govern the process and provide even more certainty and

transparency. Perhaps most importantly, itis designed to protect the public from

financial loss and to prevent a systemic collapse.

Fifth, the rest of the global community is moving toward setting up special

resolution regimes for large, inter-connected financial firms. The Financial Stability

Forum (FSB) has made this a top priority, and the head of the FSB, Mario Draghi, tells

me that they are looking to the U.S. to set the model. Because of the thousands of

different, frequently conflicting bankruptcy rules in various jurisdictions throughout the

‘world, it is simply not feasible to resolve a large, multi-national financial institution using

the bankruptcy process. A special resolution mechanism is needed that can be globally

replicated, and the U.S. is uniquely situated to lead the way.

Finally, I must admit that I feet bankruptey advocates are at cross-purposes in

their arguments. On the one hand, they whisper that the FDIC-style process could lead to

‘a “bailout” (which we categorically reject); on the other hand, they argue that it is “too

harsh” on the creditors that they represent. We invite review of the thousands of orderly

resolutions we have conducted over the years. No process is perfect, but ours has worked

well for banks large and small. Large institutions should not escape the same process we

continue to use for smaller banks simply because they have grown their non-bank

activities.

can certainly support a prompt judicial review of whether to trigger a FDIC

resolution. I would be very concemed if we moved to some hybrid between a judicial

bankruptcy process and the more expeditious FDIC-style process. In many ways, and for

the reasons noted above, that would be the worst of all worlds

As always, thank you for the opportunity to share our views with you. I hope you

find these thoughts useful, and I look forward to our continued collaboration in ending

100 big to fail.

Sincerely,

Slate

Sheila C. Bair

You might also like

- 2016 12 30 Responsive DocumentsDocument15 pages2016 12 30 Responsive DocumentsCREWNo ratings yet

- Via Electronic Mail OnlyDocument2 pagesVia Electronic Mail OnlyCREWNo ratings yet

- 2016-12-21 FOIA Request (Communications With Trump and Congress)Document3 pages2016-12-21 FOIA Request (Communications With Trump and Congress)CREWNo ratings yet

- 2016 12 16 FOIA RequestDocument3 pages2016 12 16 FOIA RequestCREWNo ratings yet

- 2017-01-06 Documents Produced 2Document36 pages2017-01-06 Documents Produced 2CREWNo ratings yet

- New York Office of The Attorney General (Trump Foundation Investigation) Request 9-14-16Document2 pagesNew York Office of The Attorney General (Trump Foundation Investigation) Request 9-14-16CREWNo ratings yet

- 2017-01-06 Final ResponseDocument2 pages2017-01-06 Final ResponseCREWNo ratings yet

- 2016 12 28 Final ResponseDocument2 pages2016 12 28 Final ResponseCREWNo ratings yet

- 2017-01-06 Documents Produced 1Document365 pages2017-01-06 Documents Produced 1CREWNo ratings yet

- 2016-12-21 FOIA Request (Documents To Congress)Document3 pages2016-12-21 FOIA Request (Documents To Congress)CREWNo ratings yet

- 2016 12 16 FOIA RequestDocument3 pages2016 12 16 FOIA RequestCREWNo ratings yet

- 2016 12 16 FOIA RequestDocument3 pages2016 12 16 FOIA RequestCREWNo ratings yet

- FBN Materials 422.15Document64 pagesFBN Materials 422.15CREWNo ratings yet

- Florida Office of The Attorney General (Daily Schedules and Travel) Request 9-14-16Document5 pagesFlorida Office of The Attorney General (Daily Schedules and Travel) Request 9-14-16CREWNo ratings yet

- Final Installment 10-17-2016Document47 pagesFinal Installment 10-17-2016CREWNo ratings yet

- FOIA Request - OGE (Trump Tweets) 12-6-16Document3 pagesFOIA Request - OGE (Trump Tweets) 12-6-16CREWNo ratings yet

- Final Response Letter 10-17-2016Document2 pagesFinal Response Letter 10-17-2016CREWNo ratings yet

- FOIA Request - OGE (Trump Transition) 12-7-16Document3 pagesFOIA Request - OGE (Trump Transition) 12-7-16CREWNo ratings yet

- FBI Denial 12-1-2016Document2 pagesFBI Denial 12-1-2016CREWNo ratings yet

- FBI Denial 12-1-2016Document2 pagesFBI Denial 12-1-2016CREWNo ratings yet

- FBI (Giuliani Communications) 11-22-16Document3 pagesFBI (Giuliani Communications) 11-22-16CREWNo ratings yet

- FBI Denial 11-29-2016Document1 pageFBI Denial 11-29-2016CREWNo ratings yet

- Memorandum in Opposition To Plaintiffs' Motion For Temporary Injunction and Declaration of Amy Frederick With ExhibitsDocument19 pagesMemorandum in Opposition To Plaintiffs' Motion For Temporary Injunction and Declaration of Amy Frederick With ExhibitsCREWNo ratings yet

- FBI (Congress Communications Re Comey Letter) 11-22-16Document3 pagesFBI (Congress Communications Re Comey Letter) 11-22-16CREWNo ratings yet

- Plaintiffs' Memorandum in Support of Motion For Temporary InjunctionDocument6 pagesPlaintiffs' Memorandum in Support of Motion For Temporary InjunctionCREWNo ratings yet

- Second Declaration of James L. MartinDocument9 pagesSecond Declaration of James L. MartinCREWNo ratings yet

- FBI (Kallstrom Communications) 11-22-16Document3 pagesFBI (Kallstrom Communications) 11-22-16CREWNo ratings yet

- Plaintiffs' Reply in Support of Motion For Preliminary InjunctionDocument2 pagesPlaintiffs' Reply in Support of Motion For Preliminary InjunctionCREWNo ratings yet

- Amended Complaint For Declaratory Judgment, Temporary, and Permanent InjunctionDocument22 pagesAmended Complaint For Declaratory Judgment, Temporary, and Permanent InjunctionCREWNo ratings yet

- Complaint For Declaratory Judgment, Temporary and Permanent InjunctionDocument8 pagesComplaint For Declaratory Judgment, Temporary and Permanent InjunctionCREWNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)