You might also like

- Report On Macroeconomics & Banking 061110Document18 pagesReport On Macroeconomics & Banking 061110Dheeraj GoelNo ratings yet

- Economic Assessment of The Euro Area ForDocument90 pagesEconomic Assessment of The Euro Area ForAdrian BuțaNo ratings yet

- Crisil Global Economy - Dec21Document4 pagesCrisil Global Economy - Dec21HarshNo ratings yet

- An Interim Assessment: What Is The Economic Outlook For OECD Countries?Document23 pagesAn Interim Assessment: What Is The Economic Outlook For OECD Countries?Jim MiddlemissNo ratings yet

- Memo MacroeconomicsDocument4 pagesMemo Macroeconomicssinghshashank12tNo ratings yet

- Economic Outlook Feb 2010Document18 pagesEconomic Outlook Feb 2010André Le RouxNo ratings yet

- Economic Update October 2021Document17 pagesEconomic Update October 2021Karar HussainNo ratings yet

- Ashmore Weekly Commentary 5 Jan 2024Document3 pagesAshmore Weekly Commentary 5 Jan 2024bagus.dpbri6741No ratings yet

- 2024global Economic Report by World BankDocument50 pages2024global Economic Report by World Bankkellymeinhold327No ratings yet

- Global Economies: How The World Economies Are Expected To PerformDocument9 pagesGlobal Economies: How The World Economies Are Expected To Performca.deepaktiwariNo ratings yet

- South East Europe Regular Economic Report: Main Report Focus NotesDocument57 pagesSouth East Europe Regular Economic Report: Main Report Focus NotesIzabela MugosaNo ratings yet

- DR Nariman Behravesh WorldFlash0222Document3 pagesDR Nariman Behravesh WorldFlash0222Swapnil PatilNo ratings yet

- Convergence Programme November 2007 2 Macroeconomic ScenarioDocument10 pagesConvergence Programme November 2007 2 Macroeconomic Scenariocristi313No ratings yet

- FEL Newsletter January 2010Document4 pagesFEL Newsletter January 2010FirstEquityLtdNo ratings yet

- OECD's Interim AssessmentDocument23 pagesOECD's Interim AssessmentTheGlobeandMailNo ratings yet

- The Baltic Outlook: Update, July 2009Document10 pagesThe Baltic Outlook: Update, July 2009Swedbank AB (publ)No ratings yet

- Monitor Markets 20230908Document2 pagesMonitor Markets 20230908Kicki AnderssonNo ratings yet

- New Setbacks, Further Policy Action Needed: Figure 1. Global GDP GrowthDocument8 pagesNew Setbacks, Further Policy Action Needed: Figure 1. Global GDP GrowthumeshnihalaniNo ratings yet

- Economic Highlights: Inflation Rate Inched Up Marginally To +1.3% Yoy in March - 23/04/2010Document3 pagesEconomic Highlights: Inflation Rate Inched Up Marginally To +1.3% Yoy in March - 23/04/2010Rhb InvestNo ratings yet

- Report On Indonesia Financial Sector Development Q2 2023Document34 pagesReport On Indonesia Financial Sector Development Q2 2023Raymond SihotangNo ratings yet

- Mid-Year Economic Update: 2010: The United States and CaliforniaDocument29 pagesMid-Year Economic Update: 2010: The United States and CaliforniajddishotskyNo ratings yet

- Country Economic Forecasts - ThailandDocument10 pagesCountry Economic Forecasts - ThailandSireethus SaovaroNo ratings yet

- Global Recovery Stalls, Downside Risks Intensify: Figure 1. Global GDP GrowthDocument7 pagesGlobal Recovery Stalls, Downside Risks Intensify: Figure 1. Global GDP GrowthMichal ZelbaNo ratings yet

- Estonia 2021 Debt Report - 0Document4 pagesEstonia 2021 Debt Report - 0raresNo ratings yet

- FY 10 Monetary ReviewDocument4 pagesFY 10 Monetary ReviewVivek SarinNo ratings yet

- The Relationship Between Property Yields and Interest RatesDocument9 pagesThe Relationship Between Property Yields and Interest RatesAlex PalcovNo ratings yet

- The ECB Survey of Professional ForecastersDocument23 pagesThe ECB Survey of Professional ForecasterscesareNo ratings yet

- State of The Economy and Prospects: Website: Http://indiabudget - Nic.inDocument22 pagesState of The Economy and Prospects: Website: Http://indiabudget - Nic.insurajkumarjaiswal9454No ratings yet

- ScotiaBank AUG 06 Europe Weekly OutlookDocument3 pagesScotiaBank AUG 06 Europe Weekly OutlookMiir ViirNo ratings yet

- Week in Pictures 10 17 22 1666106256Document13 pagesWeek in Pictures 10 17 22 1666106256Barry HeNo ratings yet

- Individual Assignment 3Document21 pagesIndividual Assignment 3Giang ĐặngNo ratings yet

- Richard Koo - 20210720Document17 pagesRichard Koo - 20210720Vivien ZhengNo ratings yet

- (HSBC) MENA Economic Q1 2016Document107 pages(HSBC) MENA Economic Q1 2016Jeff McGinnNo ratings yet

- Global Economic Outlook1Document2 pagesGlobal Economic Outlook1Harry CerqueiraNo ratings yet

- Economic Survey PDFDocument373 pagesEconomic Survey PDFVaibhavChauhanNo ratings yet

- Contractionary Forces Receding But Weak Recovery Ahead: Figure 1. Global GDP GrowthDocument8 pagesContractionary Forces Receding But Weak Recovery Ahead: Figure 1. Global GDP Growthpeter_martin9335No ratings yet

- Economics WeeklyDocument5 pagesEconomics Weeklyapi-26590406No ratings yet

- April 2020Document9 pagesApril 2020Ren SuzakuNo ratings yet

- Europe Weekly FocusDocument7 pagesEurope Weekly FocusmuneebfateenNo ratings yet

- Global Economic Forecast Q1 2020 AnalysisDocument57 pagesGlobal Economic Forecast Q1 2020 AnalysisCoulibaly SékouNo ratings yet

- Global Prospects and PoliciesDocument64 pagesGlobal Prospects and PoliciesZerohedge100% (2)

- Consumer Outlook: September 2009Document23 pagesConsumer Outlook: September 2009Lynk CusNo ratings yet

- FitchRatings - Global Economic Outlook - Crisis Update 2 April 2020 Coronavirus Crisis Sparks Deep Global RecessionDocument17 pagesFitchRatings - Global Economic Outlook - Crisis Update 2 April 2020 Coronavirus Crisis Sparks Deep Global RecessionAryttNo ratings yet

- AUG 11 UOB Global MarketsDocument3 pagesAUG 11 UOB Global MarketsMiir ViirNo ratings yet

- Econ UKEconomicsInsights 01aug11Document6 pagesEcon UKEconomicsInsights 01aug11Nicola DukeNo ratings yet

- Global Economic Outlook: Crisis Update May 2020: Coronavirus Shock BroadensDocument17 pagesGlobal Economic Outlook: Crisis Update May 2020: Coronavirus Shock BroadensManas TiwariNo ratings yet

- Global Market Review Outlook-May 2023Document3 pagesGlobal Market Review Outlook-May 2023YasahNo ratings yet

- Second Quarterly ReportDocument67 pagesSecond Quarterly ReportsultanabidNo ratings yet

- Global Recovery Advances But Remains UnevenDocument9 pagesGlobal Recovery Advances But Remains UnevenPriyanka MundheNo ratings yet

- 2011-06-08 DBS Daily Breakfast SpreadDocument6 pages2011-06-08 DBS Daily Breakfast SpreadkjlaqiNo ratings yet

- NPA World Vs India (Page 73) CHP02201009Document18 pagesNPA World Vs India (Page 73) CHP02201009jholerNo ratings yet

- QET 2022Q4 ReportDocument21 pagesQET 2022Q4 ReportSNamNo ratings yet

- Economic Highlights - Inflation Picked Up in June and Will Likely Accelerate Following The Removal of Fuel and Sugar Subsidies - 22/07/2010Document3 pagesEconomic Highlights - Inflation Picked Up in June and Will Likely Accelerate Following The Removal of Fuel and Sugar Subsidies - 22/07/2010Rhb InvestNo ratings yet

- All ChapterDocument294 pagesAll ChapterManoj KNo ratings yet

- Ashmore Weekly Commentary 27 Jan 2023Document3 pagesAshmore Weekly Commentary 27 Jan 2023Jordanata TjiptarahardjaNo ratings yet

- Unloved Bull Markets: Getting Rich the Easy Way by Riding Bull MarketsFrom EverandUnloved Bull Markets: Getting Rich the Easy Way by Riding Bull MarketsNo ratings yet

- The Escape from Balance Sheet Recession and the QE Trap: A Hazardous Road for the World EconomyFrom EverandThe Escape from Balance Sheet Recession and the QE Trap: A Hazardous Road for the World EconomyRating: 5 out of 5 stars5/5 (1)

- Middle East and North Africa Quarterly Economic Brief, January 2014: Growth Slowdown Heightens the Need for ReformsFrom EverandMiddle East and North Africa Quarterly Economic Brief, January 2014: Growth Slowdown Heightens the Need for ReformsNo ratings yet

- Gross National ProductDocument1 pageGross National ProductJoy CaliaoNo ratings yet

- A 259Document1 pageA 259AnuranjanNo ratings yet

- BUSITAX (Final Output)Document5 pagesBUSITAX (Final Output)Ivan AnaboNo ratings yet

- Impact of WTO On Textile & Clothing IndustriesDocument14 pagesImpact of WTO On Textile & Clothing IndustriesAsjad JamshedNo ratings yet

- 1991 Indian Economic Crisis - WikipediaDocument4 pages1991 Indian Economic Crisis - WikipediaChasity WrightNo ratings yet

- Manufacturing Industries For Class 10Document9 pagesManufacturing Industries For Class 10V A Prem Kumar100% (9)

- Paddy Cultivation ProposalDocument20 pagesPaddy Cultivation ProposalKah HinNo ratings yet

- About ZambiaDocument2 pagesAbout ZambiaDingan NjobvuNo ratings yet

- Lecture Three: The Balance of Payment (Bop)Document30 pagesLecture Three: The Balance of Payment (Bop)Anisa MohamedNo ratings yet

- Convetibility of Indian RupeeDocument2 pagesConvetibility of Indian RupeeAmanSharmaNo ratings yet

- Econ 151 SyllabusDocument2 pagesEcon 151 SyllabusImmah SantosNo ratings yet

- Role of Taxation in Equal Distribution of The Economic Resources in A CountryDocument5 pagesRole of Taxation in Equal Distribution of The Economic Resources in A CountryAlextro MaxonNo ratings yet

- Period: Receipts Payments Net Receipts Export (F.o.b) Import (F.o.b) Trade BalanceDocument12 pagesPeriod: Receipts Payments Net Receipts Export (F.o.b) Import (F.o.b) Trade BalanceJannat TaqwaNo ratings yet

- LC Presentasion 2-Deri Firmansyah-Eks39 ADocument7 pagesLC Presentasion 2-Deri Firmansyah-Eks39 ADeri FirmansyahNo ratings yet

- History of International TradeDocument8 pagesHistory of International TradeShayanNo ratings yet

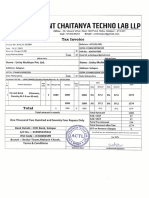

- Anant Chaitanya Techn0 Lab LLP: SalaltaDocument11 pagesAnant Chaitanya Techn0 Lab LLP: SalaltaGiridhari ChandrabansiNo ratings yet

- API BX - Gsr.gnfs - CD Ds2 en Excel v2 9944795Document83 pagesAPI BX - Gsr.gnfs - CD Ds2 en Excel v2 9944795raviNo ratings yet

- Revision ExcerciseDocument2 pagesRevision Excercise--bolabolaNo ratings yet

- GST Aug-19Document9 pagesGST Aug-19Harpreet Singh MongaNo ratings yet

- R.Chitra Devi 10MBA58: Click To Edit Master Subtitle StyleDocument17 pagesR.Chitra Devi 10MBA58: Click To Edit Master Subtitle StyleShyamala RajendranNo ratings yet

- Lucky Cement ReportDocument8 pagesLucky Cement ReportmoazzamkamranNo ratings yet

- Retail Industry in Dynamic Business EnvironmentDocument19 pagesRetail Industry in Dynamic Business EnvironmentkantimbaNo ratings yet

- Payment Methods in International TradeDocument26 pagesPayment Methods in International TradeVinod Bhat100% (8)

- Markets and Commodity Figures: Currency Cross RatesDocument1 pageMarkets and Commodity Figures: Currency Cross RatesTiso Blackstar GroupNo ratings yet

- Economic Globalization and Global Trade 1Document18 pagesEconomic Globalization and Global Trade 1Mayrell PanoncialNo ratings yet

- Press Release Dubai-Based Dodsal Group Strikes US$8bn Dollar Natural Gas Deposits in TanzaniaDocument4 pagesPress Release Dubai-Based Dodsal Group Strikes US$8bn Dollar Natural Gas Deposits in TanzaniaHussein BoffuNo ratings yet

- Cotton: World Markets and Trade: Record World Consumption Helps Lower Stocks in 2019/20Document29 pagesCotton: World Markets and Trade: Record World Consumption Helps Lower Stocks in 2019/20JigneshSaradavaNo ratings yet

- L3.3 - Comparative AdvantageDocument1 pageL3.3 - Comparative Advantage12A1-41- Nguyễn Cẩm VyNo ratings yet

- Myob - Chart of AccountsDocument4 pagesMyob - Chart of AccountsAr RaziNo ratings yet

- Rajiv Kumar S O Late Moti Prasad Sah C O Vivek Vishal Indraprasi Colony Ratu Road Ranchi Yamaha Service Cen RanchiDocument15 pagesRajiv Kumar S O Late Moti Prasad Sah C O Vivek Vishal Indraprasi Colony Ratu Road Ranchi Yamaha Service Cen RanchiNikhil KumarNo ratings yet