You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Money Psychology - Eben Pagan PDFDocument21 pagesMoney Psychology - Eben Pagan PDFSidharth Gummalla100% (2)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 2019 - Irs - Oid TableDocument141 pages2019 - Irs - Oid Table2PlusNo ratings yet

- Technical Analysis PresentationDocument73 pagesTechnical Analysis Presentationparvez ansariNo ratings yet

- DetailsDocument28 pagesDetailsNeerajNo ratings yet

- Kelompok 17 Stocks and SharesDocument6 pagesKelompok 17 Stocks and SharesishmidaNo ratings yet

- TemaDocument63 pagesTemaPashutza MalaiNo ratings yet

- INtern Foreign Exchange MarketDocument5 pagesINtern Foreign Exchange MarketPashutza MalaiNo ratings yet

- Moldova State University: Study CaseDocument34 pagesMoldova State University: Study CasePashutza MalaiNo ratings yet

- Information and Communication Technologies: Gavrilaș Natalia University LecturerDocument36 pagesInformation and Communication Technologies: Gavrilaș Natalia University LecturerPashutza MalaiNo ratings yet

- TemaDocument25 pagesTemaPashutza MalaiNo ratings yet

- The Sacrifice TheoryDocument2 pagesThe Sacrifice TheoryPashutza MalaiNo ratings yet

- Theme 11: Creating ReportsDocument15 pagesTheme 11: Creating ReportsPashutza MalaiNo ratings yet

- Tema 1 ENDocument10 pagesTema 1 ENPashutza MalaiNo ratings yet

- FINALMAYThe Validity of Wagner in UKDocument14 pagesFINALMAYThe Validity of Wagner in UKPashutza MalaiNo ratings yet

- Subtotals Are An Ideal Way To Get Totals of Several Columns of Data That The Subtotal Can Help You Insert The SUM, AVERAGE, COUNT, MIN, MAX andDocument6 pagesSubtotals Are An Ideal Way To Get Totals of Several Columns of Data That The Subtotal Can Help You Insert The SUM, AVERAGE, COUNT, MIN, MAX andPashutza MalaiNo ratings yet

- Case Study Investic Assembling The Founding TeamDocument13 pagesCase Study Investic Assembling The Founding Teamjames reichenbachNo ratings yet

- CRM Project Format Greated by Dharmarajan TrichyDocument46 pagesCRM Project Format Greated by Dharmarajan TrichydupakkurNo ratings yet

- Sesi 13 & 14Document15 pagesSesi 13 & 14Dian Permata SariNo ratings yet

- NAL Online Training Program Online Rapid Learning Series-VDocument7 pagesNAL Online Training Program Online Rapid Learning Series-VKripal SinghNo ratings yet

- CFA1 (2011) Corporate FinanceDocument9 pagesCFA1 (2011) Corporate FinancenilakashNo ratings yet

- Capitalisation AssignmentDocument5 pagesCapitalisation AssignmentFayis FYSNo ratings yet

- Article in Press: Role of Financial Regulation and Innovation in The Financial CrisisDocument11 pagesArticle in Press: Role of Financial Regulation and Innovation in The Financial CrisisLiem NguyenNo ratings yet

- Lecture 1 - Cash and Cash EquivalentsDocument18 pagesLecture 1 - Cash and Cash EquivalentsJim Carlo ChiongNo ratings yet

- 44484bos34356pm cp5 PDFDocument128 pages44484bos34356pm cp5 PDFshouvik palNo ratings yet

- On January 1 2014 Perini Company Purchased An 85 InterestDocument1 pageOn January 1 2014 Perini Company Purchased An 85 InterestMuhammad ShahidNo ratings yet

- Tpbank Annual Report 2014Document44 pagesTpbank Annual Report 2014Stella NguyenNo ratings yet

- Is Currency Trading of Interest To YouDocument1 pageIs Currency Trading of Interest To YouChung NguyenNo ratings yet

- FM I Test 2022Document5 pagesFM I Test 2022Hussien AdemNo ratings yet

- Ch2-3 Cash & Cash Equivalent and Bank Recon TablesDocument1 pageCh2-3 Cash & Cash Equivalent and Bank Recon TablesEUNICE NATASHA CABARABAN LIMNo ratings yet

- Redvest Financial Service Guide 2021 v1.0Document2 pagesRedvest Financial Service Guide 2021 v1.0Subang Jaya Youth ClubNo ratings yet

- 1-Introduction To Financial StatementsDocument95 pages1-Introduction To Financial Statementstibip12345100% (3)

- ACCA F5 Revision NotesDocument40 pagesACCA F5 Revision Notesclmc83No ratings yet

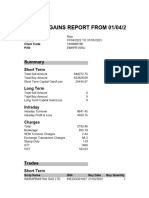

- Capital Gains - Stocks-GrowwDocument11 pagesCapital Gains - Stocks-Growwriyagupta10122000No ratings yet

- MAPFRE Insurance Brochure Ƒ PDFDocument16 pagesMAPFRE Insurance Brochure Ƒ PDFBayCreativeNo ratings yet

- YehDocument3 pagesYehDeneree Joi EscotoNo ratings yet

- Africa Startup Ecosystem Report 1gDocument118 pagesAfrica Startup Ecosystem Report 1gBongani SaidiNo ratings yet

- Chapter No.1: Banks and Scope of Banking: What Is Bank?Document58 pagesChapter No.1: Banks and Scope of Banking: What Is Bank?Manzoor HussainNo ratings yet

- Portfolio ManagementDocument36 pagesPortfolio Managementrajujaipur1234No ratings yet

- Mergers and AcquisitionsDocument81 pagesMergers and Acquisitionsleen_badiger911No ratings yet

- Report No. 6 Batoy Khey Heart N. Matano Naffy BDocument35 pagesReport No. 6 Batoy Khey Heart N. Matano Naffy BCamille EscoteNo ratings yet