You might also like

- Case Analysis: Cycles DevinciDocument1 pageCase Analysis: Cycles DevinciAritra Nandy100% (1)

- Tape Reading and Active TradingDocument97 pagesTape Reading and Active TradingOliver Bradley100% (3)

- ECON 201 Midterm 2012WDocument6 pagesECON 201 Midterm 2012WVaga boundedNo ratings yet

- Steno 2Document11 pagesSteno 2Aqib BazazNo ratings yet

- Forex Terminology Free PDFDocument7 pagesForex Terminology Free PDFKiran Krishna100% (1)

- Eco 30-10-18Document3 pagesEco 30-10-18Akki GalaNo ratings yet

- Sample - Question For HS 108Document5 pagesSample - Question For HS 108Anonymous 001No ratings yet

- Managerial Economics-2021 November (2019 Admission)Document6 pagesManagerial Economics-2021 November (2019 Admission)Nasiha PCNo ratings yet

- ECO2144 Micro Theory I 2007 Final ExamDocument5 pagesECO2144 Micro Theory I 2007 Final ExamTeachers OnlineNo ratings yet

- BHRM Test One Micro Final Marking GuideDocument6 pagesBHRM Test One Micro Final Marking GuideEsther NerimaNo ratings yet

- MTP Economics 11thDocument4 pagesMTP Economics 11thiamaarushdevsharmaNo ratings yet

- Bachelor'S of Arts (Economics Honours) Programme (Baech) : BECC-101Document6 pagesBachelor'S of Arts (Economics Honours) Programme (Baech) : BECC-101code tubeNo ratings yet

- Assignment One: Tutor Marked AssignmentsDocument25 pagesAssignment One: Tutor Marked Assignmentscode tubeNo ratings yet

- Xi Eco 2023Document4 pagesXi Eco 2023sindhuNo ratings yet

- Examination Paper: Do Not Open This Question Paper Until InstructedDocument9 pagesExamination Paper: Do Not Open This Question Paper Until InstructedNikesh MunankarmiNo ratings yet

- MicroEconomics Final ExamDocument6 pagesMicroEconomics Final ExamKanza IqbalNo ratings yet

- First AssignmentDocument7 pagesFirst AssignmentRafif RamadanNo ratings yet

- Buss 320 AssignmentDocument5 pagesBuss 320 AssignmentCaroline MwikalliNo ratings yet

- HS1340Document2 pagesHS1340Prarabdha SharmaNo ratings yet

- Eco Nov 2023 Test Paper With AnswersDocument6 pagesEco Nov 2023 Test Paper With Answersbaidshruti123No ratings yet

- Test Series: June, 2022 Mock Test Paper 2 Foundation Course Paper 4: Business Economics and Business and Commercial Knowledge Part-I: Business Economics QuestionsDocument15 pagesTest Series: June, 2022 Mock Test Paper 2 Foundation Course Paper 4: Business Economics and Business and Commercial Knowledge Part-I: Business Economics QuestionsShrwan SinghNo ratings yet

- Business LawDocument9 pagesBusiness Lawj.nikhiltrader01No ratings yet

- Test 2 Eco 1013 Sesi 1 2023 - 2024-QuestionDocument6 pagesTest 2 Eco 1013 Sesi 1 2023 - 2024-QuestionnaqeebsukriNo ratings yet

- Soal - UTS Microeconomics - MNJ1X - Kary - Kamis - 28 Okt 2021Document5 pagesSoal - UTS Microeconomics - MNJ1X - Kary - Kamis - 28 Okt 2021Lisa FebrianiNo ratings yet

- Assignment Econ 2021Document4 pagesAssignment Econ 2021bashatigabuNo ratings yet

- Microeconomics End Term Exam Academic Year: 2021-22 Time: 2 HoursDocument7 pagesMicroeconomics End Term Exam Academic Year: 2021-22 Time: 2 HoursKartik GurmuleNo ratings yet

- Eco100y5 Tt1 2012f MichaelhoDocument3 pagesEco100y5 Tt1 2012f MichaelhoexamkillerNo ratings yet

- Revision Test - Ii STD - Xii (Economics) : Seventh Day Adventist Higher Secondary SchoolDocument7 pagesRevision Test - Ii STD - Xii (Economics) : Seventh Day Adventist Higher Secondary SchoolbhavyaNo ratings yet

- Ca Foundation Economics Test - 2 Set-ADocument18 pagesCa Foundation Economics Test - 2 Set-AAshutosh BaberwalNo ratings yet

- Economics-XI-Set ADocument15 pagesEconomics-XI-Set AAkshad AroraNo ratings yet

- Eco2003f Exam 2010 PDFDocument10 pagesEco2003f Exam 2010 PDFSiphoNo ratings yet

- Ignouassignments - in 9891268050: Assignment OneDocument25 pagesIgnouassignments - in 9891268050: Assignment OneAjay KumarNo ratings yet

- Me - MidtermDocument3 pagesMe - MidtermsauravNo ratings yet

- Test Series: October, 2018 Foundation Course Mock Test Paper - 2 Paper - 4: Business Economics and Business and Commercial Knowledge Part I: Business Economics Max. Marks: 60 QuestionsDocument16 pagesTest Series: October, 2018 Foundation Course Mock Test Paper - 2 Paper - 4: Business Economics and Business and Commercial Knowledge Part I: Business Economics Max. Marks: 60 QuestionsKolkataKnightNo ratings yet

- Mec-001 Eng PDFDocument82 pagesMec-001 Eng PDFnitikanehiNo ratings yet

- Ignou Ma Eco Assignemnts July 2015 SessionDocument11 pagesIgnou Ma Eco Assignemnts July 2015 SessionAnonymous IL3nivBcNo ratings yet

- BF360 2017 Semester 2 Final ExamDocument11 pagesBF360 2017 Semester 2 Final Examlunarlove40No ratings yet

- MA Economics 2010Document19 pagesMA Economics 2010Kiran KumarNo ratings yet

- Imi611s - Intermediate Microeconomics - 2ND Opp - July 2019Document5 pagesImi611s - Intermediate Microeconomics - 2ND Opp - July 2019Smart Academic solutionsNo ratings yet

- Chapter 4 - Part 2Document17 pagesChapter 4 - Part 2dylanNo ratings yet

- Econ 2 Deg Exam 2016 - 2017 - FINAL PDFDocument11 pagesEcon 2 Deg Exam 2016 - 2017 - FINAL PDFAriel WangNo ratings yet

- HR - Bcom HBC 2104 Introduction To MicroeconomicsDocument13 pagesHR - Bcom HBC 2104 Introduction To MicroeconomicsChristopherNo ratings yet

- 4 5915484905189411272Document1 page4 5915484905189411272Henok Fikadu100% (1)

- Group AssignmDocument2 pagesGroup AssignmJibril JundiNo ratings yet

- CPT: Economics: Test Paper-1Document4 pagesCPT: Economics: Test Paper-1VirencarpediemNo ratings yet

- II Pu Economics QPDocument8 pagesII Pu Economics QPBharathi RNo ratings yet

- Assignment 1 Microeconomics (ECON101: Deadline For Students: (3/10/2022@ 23:59)Document5 pagesAssignment 1 Microeconomics (ECON101: Deadline For Students: (3/10/2022@ 23:59)Habib NasherNo ratings yet

- Chheev JJJDocument16 pagesChheev JJJrahulNo ratings yet

- Final Exam Revision - Econ 111-02-2011Document19 pagesFinal Exam Revision - Econ 111-02-2011Natalie KaruNo ratings yet

- ACCBP 100 - FINALS - 1stT - 1stS - 2019-2020Document4 pagesACCBP 100 - FINALS - 1stT - 1stS - 2019-2020Jazel Mae Celerinos100% (1)

- CBSE Sample Paper For Class 12 Economics With SolutionsDocument11 pagesCBSE Sample Paper For Class 12 Economics With SolutionsAritroy KunduNo ratings yet

- ECO 111 - Tutorial Questions - October 2021Document8 pagesECO 111 - Tutorial Questions - October 2021Nɩʜɩɭɩstic Ucʜɩʜʌ SʌsʋĸɘNo ratings yet

- Half Yearly Examination (2014 - 15) Retest Class - XII: Delhi Public School, Jodhpur Subject - EconomicsDocument4 pagesHalf Yearly Examination (2014 - 15) Retest Class - XII: Delhi Public School, Jodhpur Subject - Economicsmarudev nathawatNo ratings yet

- Becc 101Document6 pagesBecc 101Girish KumawatNo ratings yet

- ICAI CA Found. Eco & BCK Paper 30.07.2021Document14 pagesICAI CA Found. Eco & BCK Paper 30.07.2021Mitanshu MittalNo ratings yet

- Course Title: Micro EconomicsDocument6 pagesCourse Title: Micro EconomicsSalman QureshiNo ratings yet

- Business Economics 1Document9 pagesBusiness Economics 1Papa DeltaNo ratings yet

- Quantitative AssignmentDocument6 pagesQuantitative AssignmentAlemu Muleta KebedeNo ratings yet

- 1646795566Document3 pages1646795566RandomNo ratings yet

- Paper-3 Exercises-With Solutions - Bryce McBrideDocument55 pagesPaper-3 Exercises-With Solutions - Bryce McBridesamira2702100% (1)

- Economics 2 Model Question Papers by Tumkur-1 - 240202 - 225656Document6 pagesEconomics 2 Model Question Papers by Tumkur-1 - 240202 - 225656unknown.xyz.qwertNo ratings yet

- ECON 201 Midterm 2012WDocument6 pagesECON 201 Midterm 2012Wexamkiller100% (1)

- BB 107 Supplementary Exam Summer 2020 Q (Set A) (Online)Document6 pagesBB 107 Supplementary Exam Summer 2020 Q (Set A) (Online)Brewell CoNo ratings yet

- Let's Practise: Maths Workbook Coursebook 6From EverandLet's Practise: Maths Workbook Coursebook 6No ratings yet

- Business Studies - TimetableDocument15 pagesBusiness Studies - TimetableakmohideenNo ratings yet

- Guidelines For AssignmentDocument2 pagesGuidelines For AssignmentakmohideenNo ratings yet

- Online Shipping JuhaniaDocument19 pagesOnline Shipping JuhaniaakmohideenNo ratings yet

- Rania CorrectedDocument25 pagesRania CorrectedakmohideenNo ratings yet

- Communication Skill Development ProgramDocument1 pageCommunication Skill Development ProgramakmohideenNo ratings yet

- Business Research: Chapter-1 An Introduction To Marketing ResearchDocument18 pagesBusiness Research: Chapter-1 An Introduction To Marketing ResearchakmohideenNo ratings yet

- Rania CorrectedDocument32 pagesRania CorrectedakmohideenNo ratings yet

- Chapter-4: Analysis and Findings: 4.1: Demographic DescriptionDocument16 pagesChapter-4: Analysis and Findings: 4.1: Demographic DescriptionakmohideenNo ratings yet

- Respondents: 1-15 Years 16-25 Years 26-40 Years Abvoe 40 YearsDocument8 pagesRespondents: 1-15 Years 16-25 Years 26-40 Years Abvoe 40 YearsakmohideenNo ratings yet

- Questionnaire On Sales Promotion in FMCG CompaniesDocument3 pagesQuestionnaire On Sales Promotion in FMCG CompaniesakmohideenNo ratings yet

- الاستبيان 1Document2 pagesالاستبيان 1akmohideenNo ratings yet

- Explain One Reason Why Businesses Try To Take Ethical DecisionsDocument5 pagesExplain One Reason Why Businesses Try To Take Ethical DecisionsakmohideenNo ratings yet

- Age Five Different Groups Are Covered by Collected Data They Are Years Old (8%)Document16 pagesAge Five Different Groups Are Covered by Collected Data They Are Years Old (8%)akmohideenNo ratings yet

- A'Seeb Vocational College Commercial Studies DepartmentDocument9 pagesA'Seeb Vocational College Commercial Studies DepartmentakmohideenNo ratings yet

- Steno 1Document11 pagesSteno 1akmohideenNo ratings yet

- NO. Title NO. List of Tables List of Figures List of Abbreviations 1Document3 pagesNO. Title NO. List of Tables List of Figures List of Abbreviations 1akmohideenNo ratings yet

- Papers StudentDocument5 pagesPapers StudentakmohideenNo ratings yet

- Title: AuthorsDocument32 pagesTitle: AuthorsakmohideenNo ratings yet

- SM NotesDocument49 pagesSM NotesakmohideenNo ratings yet

- Marketing and Distribution of MushroomDocument1 pageMarketing and Distribution of MushroomakmohideenNo ratings yet

- Breifng PDFDocument28 pagesBreifng PDFakmohideenNo ratings yet

- BreifngDocument28 pagesBreifngakmohideenNo ratings yet

- Strategic Advertising DecisionsDocument24 pagesStrategic Advertising DecisionsakmohideenNo ratings yet

- Economic Implications of AdvertisementsDocument5 pagesEconomic Implications of AdvertisementsakmohideenNo ratings yet

- Chapter-1: Nature of Business: ObjectivesDocument2 pagesChapter-1: Nature of Business: ObjectivesakmohideenNo ratings yet

- Advertising Planning FrameworkDocument11 pagesAdvertising Planning Frameworkakmohideen100% (1)

- Creativity in AdvertisingDocument11 pagesCreativity in AdvertisingakmohideenNo ratings yet

- Measuring Advertising Effectivenes1Document17 pagesMeasuring Advertising Effectivenes1akmohideenNo ratings yet

- Final Exam-Key: Shinas Vocational CollegeDocument9 pagesFinal Exam-Key: Shinas Vocational CollegeakmohideenNo ratings yet

- Strategic Marketing Plan: Company: 99 Speedmart SDN BHDDocument22 pagesStrategic Marketing Plan: Company: 99 Speedmart SDN BHDKavita Subramaniam100% (1)

- Extra Credit - Supply and Demand Infographic - Answer KeyDocument6 pagesExtra Credit - Supply and Demand Infographic - Answer Keyrowena vocesNo ratings yet

- Definition of StrategyDocument5 pagesDefinition of StrategyAmit JainNo ratings yet

- Investor's Awareness and Perception About Commodity Market: With The Special Reference To SalemDocument6 pagesInvestor's Awareness and Perception About Commodity Market: With The Special Reference To Salemvirendra VEERU kumarNo ratings yet

- Monopolistic CompetitionDocument9 pagesMonopolistic Competitionpriyanka2303100% (2)

- Industrial Analysis: Personal Selling/ Direct SellingDocument2 pagesIndustrial Analysis: Personal Selling/ Direct Sellingshowhitee verangaNo ratings yet

- Safe Shop MarketingDocument37 pagesSafe Shop MarketingJohnsonNo ratings yet

- Study of Marketing Mix and Aida Model To Purchasing On Line Product in IndonesiaDocument14 pagesStudy of Marketing Mix and Aida Model To Purchasing On Line Product in IndonesiaIonela ConstantinNo ratings yet

- Managing New Products: The Power of InnovationDocument34 pagesManaging New Products: The Power of InnovationwaqaasrumaniNo ratings yet

- National Stock ExchangeDocument1 pageNational Stock ExchangeSachin YadavNo ratings yet

- VSA PrinciplesDocument4 pagesVSA PrinciplesCryptoFX82% (11)

- Vishal Pandey ResumeDocument3 pagesVishal Pandey ResumeAnant BhargavaNo ratings yet

- Questionnaire - Dealers CompanyDocument5 pagesQuestionnaire - Dealers Companygoomerneha100% (1)

- Parkin12e Economics Ch09Document39 pagesParkin12e Economics Ch09Lamia SiddiquiNo ratings yet

- Opportunities and Challenges in Rural MarketingDocument6 pagesOpportunities and Challenges in Rural MarketingMohammad Syafii100% (1)

- 01 Go To Market Powerpoint TemplateDocument31 pages01 Go To Market Powerpoint TemplateTarun Kumar JhaNo ratings yet

- Make My Trip Creative Brand CommunicationDocument5 pagesMake My Trip Creative Brand CommunicationPriya PahwaNo ratings yet

- 7-Supply Analysis - Introduction-06-Aug-2018 - Reference Material I - Supply AnalysisDocument5 pages7-Supply Analysis - Introduction-06-Aug-2018 - Reference Material I - Supply AnalysisEswarNo ratings yet

- Chapter 06 Consumers, Producers, and The Efficiency of MarketsDocument16 pagesChapter 06 Consumers, Producers, and The Efficiency of MarketsShabaz SharierNo ratings yet

- Summative Test in Entrepreneurship g10Document3 pagesSummative Test in Entrepreneurship g10Alodia Carlos PastorizoNo ratings yet

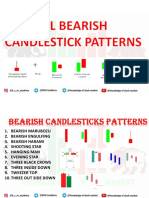

- All Bearish Candle Stick PatternsDocument18 pagesAll Bearish Candle Stick PatternsxhghdghNo ratings yet

- PLDT AcoDocument1 pagePLDT AcoWesNo ratings yet

- Presentation On Vim BarDocument12 pagesPresentation On Vim BarSourav MondalNo ratings yet

- Ballou, R. - Introduction To Business LogisticsDocument48 pagesBallou, R. - Introduction To Business LogisticsGhani RizkyNo ratings yet

- Understanding Life InsuranceDocument3 pagesUnderstanding Life InsuranceSasiNo ratings yet

- Shah Publicity Summer ProjectDocument88 pagesShah Publicity Summer ProjectVatsal MehtaNo ratings yet

- ............ May 21 U3 QP - 20Document28 pages............ May 21 U3 QP - 20Yuvipro gidwaniNo ratings yet