You might also like

- Market Makers Made SimpleDocument30 pagesMarket Makers Made SimpleJacob Shete93% (14)

- Financial Analysis - Molycorp, Inc. Produces Rare Earth Minerals. the Company Produces Rare Earth Products, Including Oxides, Metals, Alloys and Magnets for a Variety of Applications Including Clean Energy TechnologiesDocument8 pagesFinancial Analysis - Molycorp, Inc. Produces Rare Earth Minerals. the Company Produces Rare Earth Products, Including Oxides, Metals, Alloys and Magnets for a Variety of Applications Including Clean Energy TechnologiesQ.M.S Advisors LLCNo ratings yet

- December 2006 P4 QuestionDocument11 pagesDecember 2006 P4 QuestionKrishantha WeerasiriNo ratings yet

- Uestion ACK: S. No ACCA Exam Paper Syllabus AreaDocument74 pagesUestion ACK: S. No ACCA Exam Paper Syllabus AreaKalwanji K. Mtonga0% (1)

- Investment Appraisal QB 1-24Document20 pagesInvestment Appraisal QB 1-24Md. Rabiul HoqueNo ratings yet

- Aafr Ias 12 Icap Past Paper With SolutionDocument17 pagesAafr Ias 12 Icap Past Paper With SolutionAqib Sheikh100% (1)

- A Study On Investor's Perception Towards Online TradingDocument30 pagesA Study On Investor's Perception Towards Online Tradingvipin567879% (34)

- Candlestick Chart PatternsDocument9 pagesCandlestick Chart Patternssmitha100% (1)

- Corporate Reporting (International) : September/December 2016 - Sample QuestionsDocument9 pagesCorporate Reporting (International) : September/December 2016 - Sample Questionshumphrey daimonNo ratings yet

- Corporate Reporting (United Kingdom) : March/June 2018 - Sample QuestionsDocument7 pagesCorporate Reporting (United Kingdom) : March/June 2018 - Sample QuestionsMonirul Islam MoniirrNo ratings yet

- j16 Hybrid F7 QDocument7 pagesj16 Hybrid F7 QPatricia MinellyNo ratings yet

- F6mwi 2007 Dec QDocument8 pagesF6mwi 2007 Dec Qanga100% (1)

- Advanced Audit and Assurance (International) : March/June 2016 - Sample QuestionsDocument10 pagesAdvanced Audit and Assurance (International) : March/June 2016 - Sample QuestionsSyed RizviNo ratings yet

- P2 Mock Questions 201603Document9 pagesP2 Mock Questions 201603Đạt LêNo ratings yet

- MJ16 Hybrid P7UK Clean ProofDocument10 pagesMJ16 Hybrid P7UK Clean ProofvincentchanyurugwaNo ratings yet

- Lloyds Bank Q1 2019 interim resultsDocument6 pagesLloyds Bank Q1 2019 interim resultssaxobobNo ratings yet

- June 2017 - Answer To Q1 by Sir HamzaDocument4 pagesJune 2017 - Answer To Q1 by Sir HamzaHamza Abdul haqNo ratings yet

- SBR 2019 Mar-Jun QDocument6 pagesSBR 2019 Mar-Jun QmajasumNo ratings yet

- Corporate Reporting (International) : Tuesday 10 June 2008Document6 pagesCorporate Reporting (International) : Tuesday 10 June 2008Reem JavedNo ratings yet

- Corporate Reporting (International) : March/June 2017 - Sample QuestionsDocument10 pagesCorporate Reporting (International) : March/June 2017 - Sample QuestionsVinny Lu VLNo ratings yet

- June 2019 QuestionsDocument6 pagesJune 2019 QuestionsHuma SarfrazNo ratings yet

- 12 - Advanced Corporate Reporting For Strategic BusinessDocument3 pages12 - Advanced Corporate Reporting For Strategic BusinessFatima FXNo ratings yet

- Strategic Business Reporting - Irish (SBR - Irl)Document6 pagesStrategic Business Reporting - Irish (SBR - Irl)vaaniNo ratings yet

- CPA Ireland Corporate Reporting 2015-18Document174 pagesCPA Ireland Corporate Reporting 2015-18Ahmed Raza Tanveer100% (1)

- AME - 2022 - Tutorial 3 - SolutionsDocument23 pagesAME - 2022 - Tutorial 3 - SolutionsjjpasemperNo ratings yet

- Pentridge plc Consolidated Financial Statements for Year Ended 31 March 2016Document2 pagesPentridge plc Consolidated Financial Statements for Year Ended 31 March 2016Sims LauNo ratings yet

- Annual Report 2017-18Document190 pagesAnnual Report 2017-1823321gauravNo ratings yet

- Financial Reporting: March/June 2016 - Sample QuestionsDocument7 pagesFinancial Reporting: March/June 2016 - Sample QuestionsViet Nguyen QuocNo ratings yet

- Annual Report FY2020Document424 pagesAnnual Report FY2020SAGAR KASERANo ratings yet

- Opensys An20200518a2 1Document17 pagesOpensys An20200518a2 1Nor FarizalNo ratings yet

- Mock Test - 2023Document3 pagesMock Test - 2023Phuoc TruongNo ratings yet

- ICAN MAY 2018 DIET FINANCIAL REPORTING SKILLS LEVEL EXAMDocument155 pagesICAN MAY 2018 DIET FINANCIAL REPORTING SKILLS LEVEL EXAMOgunmola femiNo ratings yet

- AFA IIP.L IIIQuestion June 2016Document4 pagesAFA IIP.L IIIQuestion June 2016HossainNo ratings yet

- Financial Reporting and AnalysisDocument7 pagesFinancial Reporting and AnalysisSagarPirtheeNo ratings yet

- Domtar Quarterly ReportDocument15 pagesDomtar Quarterly ReportWJHL News Channel ElevenNo ratings yet

- UCP 2020 Annual Report Highlights Net Revenue DeclineDocument25 pagesUCP 2020 Annual Report Highlights Net Revenue Declineahmad princeNo ratings yet

- Suggested Answers CAP III - Dec 2018 PDFDocument144 pagesSuggested Answers CAP III - Dec 2018 PDFsarojdawadiNo ratings yet

- Board's ReportDocument32 pagesBoard's ReportJiya ChawlaNo ratings yet

- Financial Management End Term Paper - Batch 2020-22Document4 pagesFinancial Management End Term Paper - Batch 2020-22Swastik NayakNo ratings yet

- Malawi Taxation Paper F6Document10 pagesMalawi Taxation Paper F6angaNo ratings yet

- SBR INT-2018-dec-QPDocument7 pagesSBR INT-2018-dec-QPkeyn1230No ratings yet

- Corporate Reporting (Singapore) : Tuesday 13 December 2011Document6 pagesCorporate Reporting (Singapore) : Tuesday 13 December 2011Haaris DurraniNo ratings yet

- Directors ReportDocument51 pagesDirectors ReportEllis ElliseusNo ratings yet

- Lloyds TSB Group PLC: Results For Half-Year To 30 June 2000Document41 pagesLloyds TSB Group PLC: Results For Half-Year To 30 June 2000saxobobNo ratings yet

- 4.1 E Varun Beverages LTDDocument22 pages4.1 E Varun Beverages LTDChanchal MadankarNo ratings yet

- PAC All CAF Subjects Mock QP With Solutions Compiled by Saboor AhmadDocument132 pagesPAC All CAF Subjects Mock QP With Solutions Compiled by Saboor AhmadHadeed HafeezNo ratings yet

- FM&EconomicsQUESTIONPAPER MAY21Document6 pagesFM&EconomicsQUESTIONPAPER MAY21Harish Palani PalaniNo ratings yet

- Hindusthan Engineering Annual Report InsightsDocument104 pagesHindusthan Engineering Annual Report InsightsSanjay sharmaNo ratings yet

- P2int 2008 Dec QDocument8 pagesP2int 2008 Dec Qpkv12No ratings yet

- Tempest Accounting and AnalysisDocument10 pagesTempest Accounting and AnalysisSIXIAN JIANGNo ratings yet

- Corporate Reporting (International) : Tuesday 15 June 2010Document7 pagesCorporate Reporting (International) : Tuesday 15 June 2010magnetbox8No ratings yet

- Quiz 2aDocument2 pagesQuiz 2aadura71No ratings yet

- Dec 2002 - Qns Mod ADocument13 pagesDec 2002 - Qns Mod AHubbak Khan100% (2)

- TXP MDA December 31 2019 FINALDocument47 pagesTXP MDA December 31 2019 FINALasraghuNo ratings yet

- ACC 401-2023 GA 2-EvenDocument3 pagesACC 401-2023 GA 2-EvenOhene Asare PogastyNo ratings yet

- Exceptional and Extraordinary Items in Annual ReportDocument11 pagesExceptional and Extraordinary Items in Annual ReportMuskan TyagiNo ratings yet

- Aafr Ias 12 Icap Past Paper With SolutionDocument16 pagesAafr Ias 12 Icap Past Paper With SolutionTsegay ArayaNo ratings yet

- CA23 Financial Reporting and AnalysisDocument5 pagesCA23 Financial Reporting and AnalysisjoanNo ratings yet

- Amber Hill Financial Holdings Limited 安 山 金 控 股 份 有 限 公 司Document37 pagesAmber Hill Financial Holdings Limited 安 山 金 控 股 份 有 限 公 司in resNo ratings yet

- Ias 8Document9 pagesIas 8Syed Huzaifa SamiNo ratings yet

- Tanzania AziziDocument5 pagesTanzania Aziziazizin1994No ratings yet

- Aafr Ias 19 Icap Past Papers With SolutionDocument12 pagesAafr Ias 19 Icap Past Papers With SolutionTsegay ArayaNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Capital Asset Investment: Strategy, Tactics and ToolsFrom EverandCapital Asset Investment: Strategy, Tactics and ToolsRating: 1 out of 5 stars1/5 (1)

- P2 Corporate Reporting Essentials AnswersDocument10 pagesP2 Corporate Reporting Essentials AnswersVinny Lu VLNo ratings yet

- Moorland Group reports P2 exam answersDocument11 pagesMoorland Group reports P2 exam answersVinny Lu VLNo ratings yet

- Corporate Reporting (International) : March/June 2017 - Sample QuestionsDocument10 pagesCorporate Reporting (International) : March/June 2017 - Sample QuestionsVinny Lu VLNo ratings yet

- SD17 Hybrid F9 Answers Clean ProofDocument10 pagesSD17 Hybrid F9 Answers Clean ProofVinny Lu VLNo ratings yet

- MJ17 Hybrid F9 Ans Clean ExComm PDFDocument9 pagesMJ17 Hybrid F9 Ans Clean ExComm PDFVinny Lu VLNo ratings yet

- Financial Management: September/December 2017 - Sample QuestionsDocument6 pagesFinancial Management: September/December 2017 - Sample QuestionsVinny Lu VLNo ratings yet

- MJ17 Hybrids F9 Clean ProofDocument6 pagesMJ17 Hybrids F9 Clean ProofVinny Lu VLNo ratings yet

- Financial Management: March/June 2016 - Sample QuestionsDocument8 pagesFinancial Management: March/June 2016 - Sample QuestionsVinny Lu VLNo ratings yet

- Long DistanceDocument3 pagesLong DistanceVinny Lu VLNo ratings yet

- Mock Exam Solutions - FinQuizDocument81 pagesMock Exam Solutions - FinQuizFerran Mola ReverteNo ratings yet

- ThemeDocument6 pagesThemeVinny Lu VLNo ratings yet

- Cement Industry AnalysisDocument55 pagesCement Industry Analysisspark_12396% (54)

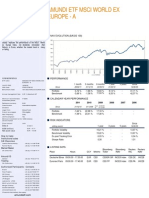

- Amundi ETF Tracks World ex Europe StocksDocument2 pagesAmundi ETF Tracks World ex Europe Stockshp24714303No ratings yet

- Long Term Assets IiDocument43 pagesLong Term Assets IiEsther TamaraNo ratings yet

- Malawi Dividend PolicyDocument31 pagesMalawi Dividend Policymages87No ratings yet

- Steelpath MLP InfographicDocument2 pagesSteelpath MLP Infographicapi-247644767No ratings yet

- Tutorial 3 - Risk Return (Part 1) PDFDocument2 pagesTutorial 3 - Risk Return (Part 1) PDFChamNo ratings yet

- PT Aqua Golden Mississippi Tbk Financial OverviewDocument4 pagesPT Aqua Golden Mississippi Tbk Financial OverviewIshidaUryuuNo ratings yet

- What is a Real Estate Investment Trust? (REITDocument45 pagesWhat is a Real Estate Investment Trust? (REITkoosNo ratings yet

- AGM & Earnings PresentationsDocument41 pagesAGM & Earnings PresentationsNaresh ReddyNo ratings yet

- Classification of Financial Services IndustryDocument4 pagesClassification of Financial Services IndustryRiteshHPatelNo ratings yet

- Vanna Volga FXDocument28 pagesVanna Volga FXTze Shao100% (1)

- MJ17 Hybrids P4 Clean ProofDocument13 pagesMJ17 Hybrids P4 Clean ProofDlamini SiceloNo ratings yet

- FINA 4001 CH 13Document23 pagesFINA 4001 CH 13Jesus Colin Campuzano100% (1)

- Auditing Problems: Adjusting Entries and Equity BalancesDocument2 pagesAuditing Problems: Adjusting Entries and Equity BalancesCattleyaNo ratings yet

- LabatDocument32 pagesLabatrascalkajeeNo ratings yet

- DSP Black RockDocument77 pagesDSP Black RockSharath S0% (1)

- Some Practice Questions-DerivativesDocument5 pagesSome Practice Questions-DerivativesAdeelTayyab50% (2)

- Taxation ManagementDocument11 pagesTaxation Managementshreya chhajerNo ratings yet

- MTLADocument10 pagesMTLAMuchamad AfifNo ratings yet

- Journalizing Transactions (Review) - 9.5.17Document13 pagesJournalizing Transactions (Review) - 9.5.17Jessa Beloy100% (1)

- Midterm Exam 2 FinanceDocument6 pagesMidterm Exam 2 FinancebobtanlaNo ratings yet

- Fundamental Analysis & TechnicalDocument4 pagesFundamental Analysis & Technicaltudoseeee4No ratings yet

- GMO Case FinalDocument23 pagesGMO Case FinalShivshankar YadavNo ratings yet

- Income Statement, Balance Sheet, Cash Flow AnalysisDocument6 pagesIncome Statement, Balance Sheet, Cash Flow AnalysisjaiNo ratings yet

- Citadel 2001Document9 pagesCitadel 2001mbt923No ratings yet

- Hitung ProyeksiDocument3 pagesHitung ProyeksiDwinanda HarsaNo ratings yet