You might also like

- Default Loan-Cancer For The Banking Sector of BangladeshDocument5 pagesDefault Loan-Cancer For The Banking Sector of BangladeshTanjila TombyNo ratings yet

- Fin 464Document4 pagesFin 464Zihad Al AminNo ratings yet

- Expert System For Banking Credit DecisionsDocument32 pagesExpert System For Banking Credit DecisionsBilal Ilyas100% (1)

- Internship Report On Non-Performing Loans of Commercial Banks in BangladeshDocument26 pagesInternship Report On Non-Performing Loans of Commercial Banks in BangladeshVivek Roy100% (1)

- Influence of Non Interest Income On Fina PDFDocument18 pagesInfluence of Non Interest Income On Fina PDFRama subediNo ratings yet

- 1.1 Background: " A Study On SME Banking Practices in Janata Bank Limited"Document56 pages1.1 Background: " A Study On SME Banking Practices in Janata Bank Limited"Tareq AlamNo ratings yet

- Recent Trend of NPL in Banking SectorDocument14 pagesRecent Trend of NPL in Banking SectorAbid HasanNo ratings yet

- Thesis Report of 5 BankDocument180 pagesThesis Report of 5 BankMd KamruzzamanNo ratings yet

- Ific BankDocument99 pagesIfic BankNoor Ibne SalehinNo ratings yet

- This Report Is To Analysis Credit Risk Management of Eastern Bank LimitedDocument30 pagesThis Report Is To Analysis Credit Risk Management of Eastern Bank Limitedশফিকুল ইসলাম লিপুNo ratings yet

- Inclusive Finance - DBBL RocketDocument56 pagesInclusive Finance - DBBL RocketTanjin UrmiNo ratings yet

- Banking As A Whole: Investment Bank Commercial BankingDocument50 pagesBanking As A Whole: Investment Bank Commercial Bankingsalva89830% (1)

- Overview of E Banking and Mobile Banking in BangladeshDocument74 pagesOverview of E Banking and Mobile Banking in BangladeshNasim AhmedNo ratings yet

- Bkash Marketing StrategiesDocument10 pagesBkash Marketing StrategiesAmirat Hossain100% (1)

- Niversity OF Haka: Non Performing Loan: Causes and Consequences Course Name: Business Research MethodsDocument26 pagesNiversity OF Haka: Non Performing Loan: Causes and Consequences Course Name: Business Research MethodsSanzida BegumNo ratings yet

- ConclusionDocument2 pagesConclusionMasud Khan Shakil0% (1)

- An - Analytical - Study - of - Determinants - of - Non-Performing LoanDocument14 pagesAn - Analytical - Study - of - Determinants - of - Non-Performing LoanSpade AceNo ratings yet

- General Banking Function of Agrani Bank LimitedDocument41 pagesGeneral Banking Function of Agrani Bank LimitedArefeen HridoyNo ratings yet

- Non-Performing Loans and Its Impact On Profitability: An Empirical Study On State Owned Commercial Banks in BangladeshDocument14 pagesNon-Performing Loans and Its Impact On Profitability: An Empirical Study On State Owned Commercial Banks in Bangladeshmostafaali123No ratings yet

- Project Report Financial ServicesDocument60 pagesProject Report Financial ServicesMahfooz Alam ShaikhNo ratings yet

- Intern Report On Bank AsiaDocument89 pagesIntern Report On Bank Asiaziko777No ratings yet

- An Internship Report OnDocument62 pagesAn Internship Report OnJahangir AlamNo ratings yet

- JBL Full - S. M. Abdul MukitDocument50 pagesJBL Full - S. M. Abdul MukithabibNo ratings yet

- Internship Report On Foreign Exchange Operation of Jamuna Bank LimitedDocument154 pagesInternship Report On Foreign Exchange Operation of Jamuna Bank LimitedAtikul Arif0% (1)

- Bank of Baroda BankingApplicationDocument45 pagesBank of Baroda BankingApplicationprateekNo ratings yet

- Credit Management System of IFIC Bank LTDDocument73 pagesCredit Management System of IFIC Bank LTDHasib SimantoNo ratings yet

- Submitted To:: "The Scenario of Non-Performing Loans in Bangladesh: Causes, Pitfalls and Remedies"Document26 pagesSubmitted To:: "The Scenario of Non-Performing Loans in Bangladesh: Causes, Pitfalls and Remedies"Siddharth ShrivastavNo ratings yet

- Assignment On NCC BankDocument44 pagesAssignment On NCC Bankhasan633100% (1)

- An Analytical Study of NPA-ProposalDocument10 pagesAn Analytical Study of NPA-ProposalBinod Kumar Karna0% (1)

- Foundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsFrom EverandFoundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsNo ratings yet

- A Study On Management of Non Performing Assets in District Central Cooperative Bank PDFDocument5 pagesA Study On Management of Non Performing Assets in District Central Cooperative Bank PDFDevikaNo ratings yet

- Report BCBLDocument98 pagesReport BCBLTanvir Ahamed100% (1)

- Credit Recovery ManagementDocument79 pagesCredit Recovery ManagementSudeep ChinnabathiniNo ratings yet

- Performance Analysis of Standard Bank Limited For Financial Years 2012-13Document16 pagesPerformance Analysis of Standard Bank Limited For Financial Years 2012-13ZerinTasnimeNo ratings yet

- SNL Fundamentals of Peer AnalysisDocument44 pagesSNL Fundamentals of Peer AnalysisBilal AhmadNo ratings yet

- Capital Market of BangladeshDocument25 pagesCapital Market of BangladeshrashelNo ratings yet

- Ific BankDocument95 pagesIfic BankAl AminNo ratings yet

- BASEL I, II, III-uDocument43 pagesBASEL I, II, III-uMomil FatimaNo ratings yet

- Overview of Lending Activity: by Dr. Ashok K. DubeyDocument19 pagesOverview of Lending Activity: by Dr. Ashok K. DubeySmitha R AcharyaNo ratings yet

- Analysis On Islamic Bank On Rate of Return RiskDocument25 pagesAnalysis On Islamic Bank On Rate of Return RiskNurhidayatul AqmaNo ratings yet

- Basel NormsDocument42 pagesBasel NormsBluehacksNo ratings yet

- Bandhan Case Study: Prepared By: Bakshi Satpreet Singh (10MBI1005)Document17 pagesBandhan Case Study: Prepared By: Bakshi Satpreet Singh (10MBI1005)Sachit MalikNo ratings yet

- Pricing of Financial Products and Services Offered by BankDocument42 pagesPricing of Financial Products and Services Offered by BankSmitaNo ratings yet

- Thesis Report On Pubali Bank LimitedDocument57 pagesThesis Report On Pubali Bank LimitedAtikul Arif100% (1)

- A Study On Bank of Maharashtra: Commercial Banking SystemDocument13 pagesA Study On Bank of Maharashtra: Commercial Banking SystemGovind N VNo ratings yet

- Soft Copy Internship Report of Sadia ChowdhuryDocument52 pagesSoft Copy Internship Report of Sadia ChowdhuryEligible Bachelor75% (4)

- Modes of Investment of IBBLDocument53 pagesModes of Investment of IBBLMussa Ratul100% (2)

- Credit Risk Management of NBL1Document119 pagesCredit Risk Management of NBL1Mir FaiazNo ratings yet

- Overview Telecom Industry in BangladeshDocument19 pagesOverview Telecom Industry in Bangladeshzubair07077371No ratings yet

- Basic Financial Management and Ratio Analysis For MFIs ToolkitDocument45 pagesBasic Financial Management and Ratio Analysis For MFIs ToolkitAndreea Cismaru100% (3)

- Origin of Report:: Chapter-1Document81 pagesOrigin of Report:: Chapter-1Pushpa BaruaNo ratings yet

- Evolution of Basel Norms and Their Contribution To The Subprime CrisisDocument7 pagesEvolution of Basel Norms and Their Contribution To The Subprime Crisisstuti dalmiaNo ratings yet

- 262086378-Internship-Report-on-Loans-and-Advances-of-Pubali-Bank-Limited 01 PDFDocument109 pages262086378-Internship-Report-on-Loans-and-Advances-of-Pubali-Bank-Limited 01 PDFaal linconNo ratings yet

- Public SME Financing and FILP System in JapanDocument36 pagesPublic SME Financing and FILP System in JapanADBI EventsNo ratings yet

- Case Study ON State Bank of India: VRS StoryDocument9 pagesCase Study ON State Bank of India: VRS StoryKapil SoniNo ratings yet

- BFW3841 Credit Analysis and Lening Management AssignmentDocument1 pageBFW3841 Credit Analysis and Lening Management Assignmenthi2joeyNo ratings yet

- Internship Report by Tanzina Ahmed ChoudhuryDocument56 pagesInternship Report by Tanzina Ahmed ChoudhuryTanzina Ahmed Choudhury100% (1)

- MID Exam (Bus620)Document2 pagesMID Exam (Bus620)red8blue8No ratings yet

- Why It Is Important To Have Glucose in Our Blood?Document2 pagesWhy It Is Important To Have Glucose in Our Blood?red8blue8No ratings yet

- Chapter 6 (Production Theory and Analysis)Document3 pagesChapter 6 (Production Theory and Analysis)red8blue8No ratings yet

- HistoryDocument2 pagesHistoryred8blue8No ratings yet

- PBH101 LabDocument4 pagesPBH101 Labred8blue8No ratings yet

- What Is BMI?Document2 pagesWhat Is BMI?red8blue8No ratings yet

- Study On Students Satisfaction Towards The Price of Snacks in Nsu CafeteriaDocument17 pagesStudy On Students Satisfaction Towards The Price of Snacks in Nsu Cafeteriared8blue8No ratings yet

- The Human Population and The EnvironmentDocument37 pagesThe Human Population and The Environmentred8blue8No ratings yet

- Inb 372 Course Outline MBT Fall 2016Document4 pagesInb 372 Course Outline MBT Fall 2016red8blue8No ratings yet

- Capital Budgeting Techniques: All Rights ReservedDocument43 pagesCapital Budgeting Techniques: All Rights Reservedred8blue8No ratings yet

- The Lean Startup NotesDocument10 pagesThe Lean Startup Notesred8blue8No ratings yet

- New ExcelDocument25 pagesNew Excelred8blue8No ratings yet

- Inb Final PresentationDocument19 pagesInb Final Presentationred8blue8No ratings yet

- Project Topic: Determining The Cost of ProductDocument10 pagesProject Topic: Determining The Cost of Productred8blue8No ratings yet

- School of Business & Economics: Financial Ratio AnalysisDocument31 pagesSchool of Business & Economics: Financial Ratio Analysisred8blue8No ratings yet

- Simón PolilloDocument28 pagesSimón PolilloDavid Enrique ValenciaNo ratings yet

- Sa 510Document14 pagesSa 510Narasimha Akash100% (1)

- ''My Trading Strategy With MACD and ADX 21 5 2017Document3 pages''My Trading Strategy With MACD and ADX 21 5 2017Vibhats VibhorNo ratings yet

- The New Concept of Alignment, Bleaching and Bonding. A Course With Inman Aligner in Dubai, United Arab Emirates.Document1 pageThe New Concept of Alignment, Bleaching and Bonding. A Course With Inman Aligner in Dubai, United Arab Emirates.InmanAlignerNo ratings yet

- Summary and Conclusions: Chapter Review and Self-Test ProblemsDocument4 pagesSummary and Conclusions: Chapter Review and Self-Test ProblemsSyed Asim AliNo ratings yet

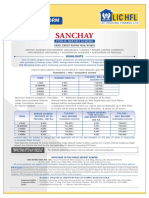

- LIC Housing Finance LTD FDDocument6 pagesLIC Housing Finance LTD FDBiswa Jyoti GuptaNo ratings yet

- Aurora Loan Services, LLC, V. Judith Mendes Da CostaDocument5 pagesAurora Loan Services, LLC, V. Judith Mendes Da CostaForeclosure Fraud100% (1)

- Sector 79Document3 pagesSector 79puebla201No ratings yet

- IIF ReportDocument152 pagesIIF ReportJuan Manuel Lopez LeonNo ratings yet

- App Aud - Prelim Exam (Key)Document16 pagesApp Aud - Prelim Exam (Key)Shaina Kaye De GuzmanNo ratings yet

- Depositry Service TinuDocument76 pagesDepositry Service TinunainakhushbooNo ratings yet

- Publice Notice Merger Notification Arise B.V and NMB 20170629Document2 pagesPublice Notice Merger Notification Arise B.V and NMB 20170629Anonymous iFZbkNw100% (2)

- Org Study Canara Bank 150904183048 Lva1 App6892Document81 pagesOrg Study Canara Bank 150904183048 Lva1 App6892shivaraj p yNo ratings yet

- Cash Management Application SetupDocument16 pagesCash Management Application SetupSriram KalidossNo ratings yet

- Legendary Chef Makes A Triumphant Return: Pierre KoffmannDocument36 pagesLegendary Chef Makes A Triumphant Return: Pierre KoffmannCity A.M.No ratings yet

- Employee HandbookDocument32 pagesEmployee HandbookKarl LabagalaNo ratings yet

- TRAIN Law BriefingDocument30 pagesTRAIN Law BriefingJoselito PabatangNo ratings yet

- 100 MCQ NegoDocument12 pages100 MCQ NegoDaphneNo ratings yet

- ch16 KeyDocument5 pagesch16 Keyrocksartha100% (1)

- CA Short Form Deed of TrustDocument3 pagesCA Short Form Deed of TrustAxisvipNo ratings yet

- Industry Profile: Banking Sector in IndiaDocument15 pagesIndustry Profile: Banking Sector in Indiasri1031No ratings yet

- Summer Internship On MSME Sector at Dena BankDocument62 pagesSummer Internship On MSME Sector at Dena BankSantashil MondalNo ratings yet

- FRTB - EyDocument8 pagesFRTB - EyJamesMc1144No ratings yet

- MCTC Refund FormDocument1 pageMCTC Refund FormdsdsNo ratings yet

- Practice Banking SyllabusDocument2 pagesPractice Banking SyllabusSrinivas GowdaNo ratings yet

- EcsmformDocument1 pageEcsmform0sandeepNo ratings yet

- Alice in Credit-Card Land - On ChargebacksDocument3 pagesAlice in Credit-Card Land - On ChargebacksFábio OliveiraNo ratings yet

- 7 P's of MarketingDocument42 pages7 P's of MarketingSagar Kumar0% (1)

- SBI Central Public Information Officer (CPIODocument219 pagesSBI Central Public Information Officer (CPIOanil kumarNo ratings yet

- Import Form 2018Document6 pagesImport Form 2018tejasg82100% (2)