You might also like

- NCC Bank ReportDocument54 pagesNCC Bank ReportSumon Shopnil100% (1)

- Overview of National BankDocument23 pagesOverview of National BankOnline CornerNo ratings yet

- Introduction To The ReportDocument34 pagesIntroduction To The ReportTalha Iftekhar Khan SwatiNo ratings yet

- Corporate Goverance - BodyDocument14 pagesCorporate Goverance - BodyjehanNo ratings yet

- Commercial Bank Loan ManagementDocument13 pagesCommercial Bank Loan ManagementBinod PoudelNo ratings yet

- Project of MCBDocument55 pagesProject of MCBSana JavaidNo ratings yet

- Intro of Prime BankDocument28 pagesIntro of Prime Banknusra_tNo ratings yet

- Study Material for Promotion Exams at Bank of BarodaDocument209 pagesStudy Material for Promotion Exams at Bank of BarodaPradipta BhattacharjeeNo ratings yet

- An Economy of A Country Depends On BankingDocument22 pagesAn Economy of A Country Depends On BankingOnline CornerNo ratings yet

- Internship Report RimshaDocument24 pagesInternship Report RimshaRimsha ButtNo ratings yet

- Executive Summary 1Document82 pagesExecutive Summary 1madihaijazkhanNo ratings yet

- SBI Non Performing AssetsDocument43 pagesSBI Non Performing AssetsVikram RokadeNo ratings yet

- Internship Report RimshaDocument23 pagesInternship Report RimshaRimsha ButtNo ratings yet

- Format of Internship ReportDocument32 pagesFormat of Internship ReportMuhammad BilalNo ratings yet

- Final Term Project: Report On MCB PakistanDocument6 pagesFinal Term Project: Report On MCB PakistanBHATTINo ratings yet

- Assignment On NCC BankDocument44 pagesAssignment On NCC Bankhasan633100% (1)

- Chapter # 1 IntroductionDocument107 pagesChapter # 1 Introductionmani1518No ratings yet

- Financing Small and Medium Business Enterprises by Janata Bank LTDDocument74 pagesFinancing Small and Medium Business Enterprises by Janata Bank LTDShowkatul IslamNo ratings yet

- Internship Report: MCB Bank LimitedDocument62 pagesInternship Report: MCB Bank Limitedfalon123No ratings yet

- To Evaluate The Financial Performance of The General Banking ActivitiesDocument53 pagesTo Evaluate The Financial Performance of The General Banking ActivitiesNiaz MorshedNo ratings yet

- Credit Management of NCC Bank Ltd.Document69 pagesCredit Management of NCC Bank Ltd.death_heaven100% (1)

- NCC Bank Credit Management and International Trade ReportDocument70 pagesNCC Bank Credit Management and International Trade ReportMarjana Khatun100% (1)

- RECENT DEVELOPMENTS IN INDIA'S BANKING SECTORDocument20 pagesRECENT DEVELOPMENTS IN INDIA'S BANKING SECTORSatyajit SahooNo ratings yet

- IT Final Project. GROUP#3Document18 pagesIT Final Project. GROUP#3Farishtey ZahraNo ratings yet

- Corporate CreditDocument69 pagesCorporate CreditAshish chanchlani100% (1)

- Master Tile Internship UOGDocument54 pagesMaster Tile Internship UOGAhsanNo ratings yet

- Internship Report On Nib Bank: Provided by Nishat Academy IslamabadDocument16 pagesInternship Report On Nib Bank: Provided by Nishat Academy Islamabadk_starsunNo ratings yet

- Internship Report On MCB Bank LimitedDocument40 pagesInternship Report On MCB Bank Limitedbbaahmad89No ratings yet

- Dsu Report PDFDocument14 pagesDsu Report PDFomNo ratings yet

- Project On MCB GCUFDocument19 pagesProject On MCB GCUFAmna Goher100% (1)

- 1.1 Background: Primary Sources of DataDocument42 pages1.1 Background: Primary Sources of Dataronok_85No ratings yet

- INTERNSHIP REPORT On UBLDocument22 pagesINTERNSHIP REPORT On UBLNour E HuddaNo ratings yet

- Bank Audit ProceduresDocument18 pagesBank Audit ProceduresPranav HariharanNo ratings yet

- Modernizing Banking ServicesDocument78 pagesModernizing Banking ServicesDharmikNo ratings yet

- MCB Report PDFDocument84 pagesMCB Report PDFMuhammad Irshad KhanNo ratings yet

- Bank and Banking System of BangladeshDocument49 pagesBank and Banking System of BangladeshCONTENT TUBENo ratings yet

- E-Banking Preferences Among PeopleDocument47 pagesE-Banking Preferences Among PeopleBishyer AmitNo ratings yet

- BRAC Bank Internship Report SummaryDocument124 pagesBRAC Bank Internship Report Summaryashik0526No ratings yet

- Bank of IndiaDocument94 pagesBank of IndiaOm Prakash Singh100% (2)

- DiruDocument84 pagesDirudhiru_hadiaNo ratings yet

- 6 FEOD AND DFSU ReportDocument45 pages6 FEOD AND DFSU ReportOsama HussainNo ratings yet

- MCB Bank Limited Internship ReportDocument52 pagesMCB Bank Limited Internship ReportSufian IqbalNo ratings yet

- Project Banking Repaired)Document26 pagesProject Banking Repaired)gautamshankarNo ratings yet

- Training Programs at Sonali BankDocument36 pagesTraining Programs at Sonali BankMission job30forlifeNo ratings yet

- Ahmer Report FinaldsfdfDocument55 pagesAhmer Report FinaldsfdfZaheer Ahmed SwatiNo ratings yet

- Internship Report ON Human Resource and Marketing Department in Tsehey BankDocument14 pagesInternship Report ON Human Resource and Marketing Department in Tsehey BankEthiopia AmergaNo ratings yet

- Research Project Rough ReportDocument73 pagesResearch Project Rough Reportpamidi shakeerNo ratings yet

- NCC Bank LTDDocument69 pagesNCC Bank LTDZaman's ZarineNo ratings yet

- Report MCBDocument29 pagesReport MCBalisha waheedNo ratings yet

- Chapter # 2: Organization Structure of National Bank of Pakistan 2.1 NBP Organizational StructureDocument15 pagesChapter # 2: Organization Structure of National Bank of Pakistan 2.1 NBP Organizational StructureTalha Iftekhar KhanNo ratings yet

- Mansoor Ihsan ReportDocument70 pagesMansoor Ihsan ReportSherzada KhanNo ratings yet

- Banking: Industries in IndiaDocument41 pagesBanking: Industries in IndiaManavNo ratings yet

- Executive SummaryDocument59 pagesExecutive SummarywaqarNo ratings yet

- Group-3 Bank: MCB: Project: Commercial BankingDocument18 pagesGroup-3 Bank: MCB: Project: Commercial Bankingshahroze ALINo ratings yet

- Union Bank Limited Internship ReportDocument60 pagesUnion Bank Limited Internship Reportsaleemkhp50% (2)

- Understand Banks & Financial Markets: An Introduction to the International World of Money & FinanceFrom EverandUnderstand Banks & Financial Markets: An Introduction to the International World of Money & FinanceRating: 4 out of 5 stars4/5 (9)

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Public Financing for Small and Medium-Sized Enterprises: The Cases of the Republic of Korea and the United StatesFrom EverandPublic Financing for Small and Medium-Sized Enterprises: The Cases of the Republic of Korea and the United StatesNo ratings yet

- Iqbal, Javed Document - 10 - FSABRDocument12 pagesIqbal, Javed Document - 10 - FSABRAhsanNo ratings yet

- Assignment No 1Document12 pagesAssignment No 1AhsanNo ratings yet

- Ahmed, Hammad Financial System and Banking Regualtion Ass 1Document10 pagesAhmed, Hammad Financial System and Banking Regualtion Ass 1AhsanNo ratings yet

- Assignment-01: Name: Sheraz Ahmed Roll No: 20021554-048 Submitted To: Sir AhsanDocument11 pagesAssignment-01: Name: Sheraz Ahmed Roll No: 20021554-048 Submitted To: Sir AhsanAhsanNo ratings yet

- Assignment # 1: Financial System & Banking RegulationDocument10 pagesAssignment # 1: Financial System & Banking RegulationAhsanNo ratings yet

- Global Financial Crises of 1929 and 2008: Causes and EffectsDocument10 pagesGlobal Financial Crises of 1929 and 2008: Causes and EffectsAhsanNo ratings yet

- Financial System&banking Reg.: Global Finance Crises 1928 To 2008Document11 pagesFinancial System&banking Reg.: Global Finance Crises 1928 To 2008AhsanNo ratings yet

- Financial CrisisDocument12 pagesFinancial CrisisAhsanNo ratings yet

- Basic Approaches To Leadership: Organizational BehaviorDocument16 pagesBasic Approaches To Leadership: Organizational BehaviorAhsanNo ratings yet

- Assignment: Course Code: Comm-206 Course Title: Financial System and Banking R. Submitted byDocument10 pagesAssignment: Course Code: Comm-206 Course Title: Financial System and Banking R. Submitted byAhsanNo ratings yet

- Assignment # 1: Financial Crisis 1929Document13 pagesAssignment # 1: Financial Crisis 1929AhsanNo ratings yet

- Financial CrisisDocument12 pagesFinancial CrisisAhsanNo ratings yet

- OB11 12stDocument18 pagesOB11 12stKKNo ratings yet

- Report On Global Financial CrisisDocument11 pagesReport On Global Financial CrisisAhsanNo ratings yet

- Financial CrisisDocument11 pagesFinancial CrisisAhsanNo ratings yet

- Communication: Organizational BehaviorDocument16 pagesCommunication: Organizational BehaviorAditi SoniNo ratings yet

- Perception and Individual Decision Making: Organizational BehaviorDocument23 pagesPerception and Individual Decision Making: Organizational Behaviororyz agnuNo ratings yet

- Letter of RecommendationDocument1 pageLetter of RecommendationAhsanNo ratings yet

- Foundation of Group BehaviorDocument23 pagesFoundation of Group Behavioraqsa palijoNo ratings yet

- Values, Attitudes, and Job Satisfaction: Organizational BehaviorDocument21 pagesValues, Attitudes, and Job Satisfaction: Organizational BehaviorAhsanNo ratings yet

- MCB Internship UOGDocument51 pagesMCB Internship UOGAhsanNo ratings yet

- Motivation: From Concept To Applications: Organizational BehaviorDocument20 pagesMotivation: From Concept To Applications: Organizational BehaviorAditi SoniNo ratings yet

- Personality and Emotions: Organizational BehaviorDocument20 pagesPersonality and Emotions: Organizational Behavioryakan_aNo ratings yet

- Understanding Work Teams: Organizational BehaviorDocument10 pagesUnderstanding Work Teams: Organizational Behaviormoeen.tariq9252No ratings yet

- Chapter 1 What Is Organizational BehaviorDocument21 pagesChapter 1 What Is Organizational Behavioriqbal febriyantoNo ratings yet

- Basic Motivation Concepts: Organizational BehaviorDocument23 pagesBasic Motivation Concepts: Organizational BehaviorAditi SoniNo ratings yet

- Dynamic CapabilityDocument8 pagesDynamic CapabilityAhsanNo ratings yet

- Literature ReviewDocument7 pagesLiterature ReviewAhsanNo ratings yet

- Foundations of Individual BehaviorDocument14 pagesFoundations of Individual BehaviorNiraj SharmaNo ratings yet

- Rich and Ppor Dad BookDocument1 pageRich and Ppor Dad BookŤŕī ŚhāñNo ratings yet

- Super Care Pharma Bank Statement-July-2021Document4 pagesSuper Care Pharma Bank Statement-July-2021AKM Anwar SadatNo ratings yet

- PLM TAX 2 2016-2017 List of Cases & Assigned StrudentsDocument19 pagesPLM TAX 2 2016-2017 List of Cases & Assigned StrudentsCharlie Pein100% (1)

- MR - Vipin SharmaDocument1 pageMR - Vipin SharmaVIPIN SHARMANo ratings yet

- Plastic MoneyDocument63 pagesPlastic MoneyMaurya RahulNo ratings yet

- Negotiation of Export-Import DocumentsDocument16 pagesNegotiation of Export-Import Documentsramneet15866443100% (1)

- Accommodation Bills of ExchangeDocument5 pagesAccommodation Bills of Exchangenaumanahmad867129No ratings yet

- Macam-Vs-CaDocument3 pagesMacam-Vs-CaMikee RañolaNo ratings yet

- Chap 004Document20 pagesChap 004AHMED MOHAMED YUSUFNo ratings yet

- Ifm Field ReportDocument25 pagesIfm Field ReportEmmanuel Patrick100% (8)

- Travel and Expense PolicyDocument6 pagesTravel and Expense PolicyLee Cogburn100% (1)

- Test Copy ElmDocument2 pagesTest Copy ElmRama Krishna Saraswati80% (5)

- Credit Transactions - Transcribed First LectureDocument5 pagesCredit Transactions - Transcribed First LectureClarisse Ann MirandaNo ratings yet

- Reforms in Banking SectorDocument18 pagesReforms in Banking SectorPrabhjotkaur650% (2)

- Vietcombank Drawing Money Service FlowchartDocument1 pageVietcombank Drawing Money Service FlowchartHoàng VõNo ratings yet

- Credit Midterm Reviewer - Loan and DepositDocument12 pagesCredit Midterm Reviewer - Loan and Depositviva_33No ratings yet

- HDFC Bank TyDocument72 pagesHDFC Bank TyKhalid SaiyadNo ratings yet

- Part 3: Proposal of Recommendation For Credit Card Service Development at Vietinbank 3.1 Vietinbank Achivements in 2019Document3 pagesPart 3: Proposal of Recommendation For Credit Card Service Development at Vietinbank 3.1 Vietinbank Achivements in 2019Sữa ChuaNo ratings yet

- Life Rankings 2020 Based On Q4 Investments 1Document1 pageLife Rankings 2020 Based On Q4 Investments 1Ron CatalanNo ratings yet

- Commercial Letters of Credit ExplainedDocument130 pagesCommercial Letters of Credit ExplainedavisibleNo ratings yet

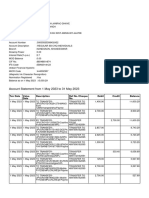

- Account Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument10 pagesAccount Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceavinashdeshmukh7027No ratings yet

- Lafarge Zambia 2015 Annual ReportDocument60 pagesLafarge Zambia 2015 Annual Reportimbo9100% (1)

- Describe The Concept of InsuranceDocument12 pagesDescribe The Concept of InsuranceIndu GuptaNo ratings yet

- List of Breach FirmsDocument819 pagesList of Breach FirmsSufyan AshrafNo ratings yet

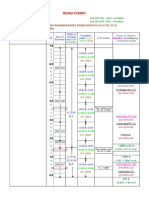

- ROAD CHART TITLEDocument4 pagesROAD CHART TITLEPhani PitchikaNo ratings yet

- UBL Internship ReportDocument124 pagesUBL Internship ReportTaha MadniNo ratings yet

- GIRO 2017 Delegate ListDocument22 pagesGIRO 2017 Delegate ListMike100% (1)

- MBA Finance ProjectDocument74 pagesMBA Finance ProjectAnshul BhardwajNo ratings yet

- Cashlite TNC Oct2018 EnbmDocument15 pagesCashlite TNC Oct2018 EnbmPokya SgNo ratings yet

- Challan 431798 02052018 112519 PDFDocument1 pageChallan 431798 02052018 112519 PDFchandrikaNo ratings yet