You might also like

- Final Annex F SGLGB Form No. 6Document3 pagesFinal Annex F SGLGB Form No. 6ruth searesNo ratings yet

- VAWC Form 1Document3 pagesVAWC Form 1Jervel GuanzonNo ratings yet

- 20% EDF PlanDocument1 page20% EDF PlanMarie AlejoNo ratings yet

- 1.1.1-1 FAS BFDP Monitoring Form ADocument1 page1.1.1-1 FAS BFDP Monitoring Form AVirgo CayabaNo ratings yet

- Republic of The Philippines Department of DBP Regional Office No. XVI, Marunong CityDocument38 pagesRepublic of The Philippines Department of DBP Regional Office No. XVI, Marunong CityTsenre Lien AragNo ratings yet

- BCPC Accomplishment Report Form 001-ADocument2 pagesBCPC Accomplishment Report Form 001-Abarangay threeNo ratings yet

- EO - Designation of Brgy Info OfficerDocument2 pagesEO - Designation of Brgy Info OfficerP2LT UTIT-CAABAY JAGS100% (1)

- Reorganizing the Barangay Banggot Peace and Order CommitteeDocument2 pagesReorganizing the Barangay Banggot Peace and Order CommitteeBARANGAY BANGGOT BANGGOTNo ratings yet

- Form BHERTsDocument1 pageForm BHERTsCasey Del Gallego EnrileNo ratings yet

- Past Year Current Year Budget Year (Actual) (Proposed)Document16 pagesPast Year Current Year Budget Year (Actual) (Proposed)Saphire DonsolNo ratings yet

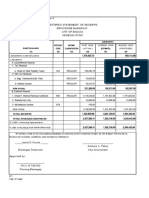

- 2022 Certified Statement of IncomeDocument2 pages2022 Certified Statement of IncomeAnne Socorro AbellanosaNo ratings yet

- Resolution 16 Republic Act No. 11285 Energy Efficiency and Conservation ActDocument5 pagesResolution 16 Republic Act No. 11285 Energy Efficiency and Conservation ActBARANGAY MOLINO IINo ratings yet

- Leyte Canal Construction Bidding AnnouncedDocument17 pagesLeyte Canal Construction Bidding AnnouncedArlene VillarosaNo ratings yet

- Annual Investment Program-2018Document3 pagesAnnual Investment Program-2018Shy Pantinople100% (1)

- Projects/Plans/Activity For BCPC Budget FY 2017Document5 pagesProjects/Plans/Activity For BCPC Budget FY 2017blublagaNo ratings yet

- CapDev AgendaDocument5 pagesCapDev AgendaLemuel Cayabyab100% (1)

- SGLGB - BDC Annex 3 and 4Document5 pagesSGLGB - BDC Annex 3 and 4Vinvin EsoenNo ratings yet

- BADPA TemplateDocument1 pageBADPA TemplateIinday AnrymNo ratings yet

- Post Activity ReportDocument3 pagesPost Activity ReportBarangay PalabotanNo ratings yet

- 3 Capacity Development Agenda For Barangays (Annex G-2)Document68 pages3 Capacity Development Agenda For Barangays (Annex G-2)Barangay Poblacion NaawanNo ratings yet

- Region: V City/Mun.: Bulusan Province: Sorsogon BARANGAY: DancalanDocument1 pageRegion: V City/Mun.: Bulusan Province: Sorsogon BARANGAY: DancalanChristine Frilles100% (1)

- Napafutu Nga Serbisyu, Pammacapianan Na Magaru": BARANGAYDocument4 pagesNapafutu Nga Serbisyu, Pammacapianan Na Magaru": BARANGAYAji NomotoNo ratings yet

- SGLGB Form 4. ChecklistDocument12 pagesSGLGB Form 4. ChecklistDENNIS PADOLINANo ratings yet

- Evacuation Management TeamDocument4 pagesEvacuation Management TeamMaeSarah Reambillo CamaNo ratings yet

- Barangay Development Council (BDC)Document2 pagesBarangay Development Council (BDC)sadzNo ratings yet

- FINAL-Annex E - SGLGB Form No. 5Document2 pagesFINAL-Annex E - SGLGB Form No. 5michael ricafortNo ratings yet

- Barangay Anti-Drug Abuse Council (Badac) Action Plan: FOR CYDocument1 pageBarangay Anti-Drug Abuse Council (Badac) Action Plan: FOR CYDann MarrNo ratings yet

- Annual Investment Plan identifies LGU projects and programsDocument5 pagesAnnual Investment Plan identifies LGU projects and programsFelicitas RelatoNo ratings yet

- Utilization of 2018 SK FundsDocument2 pagesUtilization of 2018 SK FundsDavid Mikael Nava TaclinoNo ratings yet

- Budget2022 Legaspi Final DraftDocument110 pagesBudget2022 Legaspi Final DraftFely rose SalangoNo ratings yet

- Aip 2023 EditedDocument6 pagesAip 2023 EditedLeon Garcia SrNo ratings yet

- Inventory of LGU Services for Barangay Sta. TeresaDocument15 pagesInventory of LGU Services for Barangay Sta. Teresamichael ricafortNo ratings yet

- MC No. 2019-35 PDFDocument4 pagesMC No. 2019-35 PDFRosalie T. Orbon-TamondongNo ratings yet

- Office of The Barangay Anti-Drug Abuse Council (Badac) Minutes of The Barangay Anti-Drug Abuse Council MeetingDocument2 pagesOffice of The Barangay Anti-Drug Abuse Council (Badac) Minutes of The Barangay Anti-Drug Abuse Council Meetingmark gempisawNo ratings yet

- Indicators Rating Remarks: City/MunicipalityDocument2 pagesIndicators Rating Remarks: City/MunicipalityJimNo ratings yet

- VAW Desk Form 5Document1 pageVAW Desk Form 5Shimofu KedokitokimoNo ratings yet

- Certification of unutilized MOOE funds for reprogrammingDocument1 pageCertification of unutilized MOOE funds for reprogrammingBarangay Taguitic100% (1)

- SB Resolution PPAN Adoption 2017-2022Document3 pagesSB Resolution PPAN Adoption 2017-2022Babuu BabuuNo ratings yet

- ELECTION - ForM - Annex C - Certificate of CandidacyDocument1 pageELECTION - ForM - Annex C - Certificate of CandidacyAaron GarlitosNo ratings yet

- Dahilig BDP Final Draft 2024-2029Document41 pagesDahilig BDP Final Draft 2024-2029melanie llagasNo ratings yet

- Table of Contents BnapDocument1 pageTable of Contents BnapJhonel De LimaNo ratings yet

- Barangay Budget PreparationDocument72 pagesBarangay Budget PreparationRjay's EscapadeNo ratings yet

- Republic of The Philippines Province of Camarines Sur Municipality of Ocampo Barangay Gatbo - O0oDocument26 pagesRepublic of The Philippines Province of Camarines Sur Municipality of Ocampo Barangay Gatbo - O0oCristina MelloriaNo ratings yet

- Transmittal Report From Barangay To CourtDocument1 pageTransmittal Report From Barangay To CourtEarlene Dale100% (1)

- Executive Order 3 BACDocument5 pagesExecutive Order 3 BACCy ValenzuelaNo ratings yet

- Barangay Monthly Road Clearing Annex ADocument1 pageBarangay Monthly Road Clearing Annex ARichard Bandong100% (1)

- 1.1.2 FAS BFR Statement of Receipt and ExpenditureDocument2 pages1.1.2 FAS BFR Statement of Receipt and Expenditureedvince mickael bagunas sinonNo ratings yet

- Brgy Template HAPAG Annex A 2sem 2023Document1 pageBrgy Template HAPAG Annex A 2sem 2023carmelagarcia496No ratings yet

- Final SGLGB Form 2. Data Capture Form A4Document9 pagesFinal SGLGB Form 2. Data Capture Form A4junayrah galmanNo ratings yet

- 1 Brgy Bussiness Clearance New 1Document1 page1 Brgy Bussiness Clearance New 1alfredo taguian100% (1)

- CBYDP Objectives Youth Development Tuao SouthDocument18 pagesCBYDP Objectives Youth Development Tuao SouthBarangay Tuao SouthNo ratings yet

- Annex ADocument1 pageAnnex Akerwin jayNo ratings yet

- Department of The Interior and Local GovernmentDocument6 pagesDepartment of The Interior and Local GovernmentMarvin ReyesNo ratings yet

- Compliance To DRRM Act, Cca Act, Utilization of LDRRM Fund and Calamity Response ProtocolDocument3 pagesCompliance To DRRM Act, Cca Act, Utilization of LDRRM Fund and Calamity Response Protocolyan deeNo ratings yet

- (Final) 2023 SGLGB Form 4-Component City - Municipal Consolidated Performance Assessment FormDocument5 pages(Final) 2023 SGLGB Form 4-Component City - Municipal Consolidated Performance Assessment FormRosalie T. Orbon-TamondongNo ratings yet

- Logbook of Checks Issued and CancelledDocument2 pagesLogbook of Checks Issued and Cancelledmichael john chavezNo ratings yet

- For Tanod EquipmentDocument2 pagesFor Tanod EquipmentBarangaymananaoevsiqNo ratings yet

- State of Barangay Governance ReportDocument100 pagesState of Barangay Governance ReportBrgylusongNo ratings yet

- Appendix 26 - RCD FormDocument1 pageAppendix 26 - RCD FormRogie ApoloNo ratings yet

- Quarterly Remittance Return: of Creditable Income Taxes Withheld (Expanded)Document2 pagesQuarterly Remittance Return: of Creditable Income Taxes Withheld (Expanded)Xylia TocaoNo ratings yet

- Leris Online Step by StepDocument22 pagesLeris Online Step by StepPRC Board85% (13)

- App Form UMID 2013Document2 pagesApp Form UMID 2013Адриан Убежище МоленьоNo ratings yet

- Value Ifrs June 2018Document53 pagesValue Ifrs June 2018Juan Daniel Garcia VeigaNo ratings yet

- App Form UMID 2013Document2 pagesApp Form UMID 2013Адриан Убежище МоленьоNo ratings yet

- Dissolution of Stock and Non-Stock (Corporate Term)Document1 pageDissolution of Stock and Non-Stock (Corporate Term)joseNo ratings yet

- Business Permit: Jps Nutri Herb IncDocument1 pageBusiness Permit: Jps Nutri Herb IncjoseNo ratings yet

- WAIVER ON REQUEST MeralcoDocument1 pageWAIVER ON REQUEST MeralcoAnonymous WXqKjTXMNo ratings yet

- G.R. No. 131359 - MERALCO vs. Province of LagunaDocument6 pagesG.R. No. 131359 - MERALCO vs. Province of LagunaseanNo ratings yet

- Your Electric BillDocument2 pagesYour Electric BillMarlene SubaNo ratings yet

- Bonnevie vs. Hernandez DigestDocument2 pagesBonnevie vs. Hernandez DigestPaolo AdalemNo ratings yet

- Classes of Corporation: Definition and ExampleDocument2 pagesClasses of Corporation: Definition and ExampleAisa SajolNo ratings yet

- PROPERTY (Case Digest Compilation)Document34 pagesPROPERTY (Case Digest Compilation)marizfuster17100% (1)

- Magna Carta For Residential Electricity PDFDocument92 pagesMagna Carta For Residential Electricity PDFEmmanuel S. CaliwanNo ratings yet

- Certificate of AttendanceDocument11 pagesCertificate of AttendanceCharisse Jordan CruzNo ratings yet

- 10 NPC DAMA V NPC (2017)Document41 pages10 NPC DAMA V NPC (2017)Samantha NicoleNo ratings yet

- Sps. Quisumbing vs. MERALCO rules on due process in disconnectionDocument1 pageSps. Quisumbing vs. MERALCO rules on due process in disconnectionRiss GammadNo ratings yet

- Meralco v. RamoyDocument1 pageMeralco v. Ramoycsalipio24No ratings yet

- Industry Analysis of MERALCO Using Porter's Five ForcesDocument5 pagesIndustry Analysis of MERALCO Using Porter's Five ForcesBi Nardo75% (4)

- Expanded Withholding TaxDocument3 pagesExpanded Withholding TaxCordero TJNo ratings yet

- Admin Cases CompilationDocument34 pagesAdmin Cases CompilationBenn DegusmanNo ratings yet

- Republic v. MeralcoDocument2 pagesRepublic v. MeralcoJoyce Sumagang Reyes100% (1)

- Property Meralco Steel Towers CaseDocument10 pagesProperty Meralco Steel Towers CaseJelena SebastianNo ratings yet

- National Educators Academy of The Philippines: QAME Analysis Form IDocument17 pagesNational Educators Academy of The Philippines: QAME Analysis Form IArlyne NonatoNo ratings yet

- Philippine Health-Care Providers vs. Estrada G.R. No. 171052 28 January 2008Document2 pagesPhilippine Health-Care Providers vs. Estrada G.R. No. 171052 28 January 2008krystel engcoyNo ratings yet

- Case Study 7Document4 pagesCase Study 7angelo macatangayNo ratings yet

- EpiraDocument163 pagesEpiraBenNo ratings yet

- Manila Electric Company Land Registration CaseDocument2 pagesManila Electric Company Land Registration CaseSonnyNo ratings yet

- New DEED OF ABSOLUTE SALE With SPADocument2 pagesNew DEED OF ABSOLUTE SALE With SPAOliver Raymundo50% (2)

- Supreme Court Rules in Favor of TEC and TPC in Dispute Over Alleged Electric Meter TamperingDocument8 pagesSupreme Court Rules in Favor of TEC and TPC in Dispute Over Alleged Electric Meter TamperingDiosa Mae SarillosaNo ratings yet

- Meralco v. Pasay TraspoDocument3 pagesMeralco v. Pasay TraspoJackie JubilanNo ratings yet

- Taxation 2 Case DigestDocument27 pagesTaxation 2 Case DigestThalia SalvadorNo ratings yet

- 08 Meralco Vs City Assessor of LucenaDocument1 page08 Meralco Vs City Assessor of LucenaKIMMYNo ratings yet

- Manila Electric Company V Pasay Transportation Company, Inc., Et Al.Document1 pageManila Electric Company V Pasay Transportation Company, Inc., Et Al.John YeungNo ratings yet

- Case 1 PropertyDocument194 pagesCase 1 PropertyMarj Reña LunaNo ratings yet

- Mini ResearchDocument14 pagesMini ResearchMarco BiliganNo ratings yet

- ERC vs NASECORE (GR No. 163935Document6 pagesERC vs NASECORE (GR No. 163935ANTHONY SALVADICONo ratings yet