You might also like

- NDC V CIRDocument5 pagesNDC V CIRjonbelzaNo ratings yet

- Summary of Significant SC Decisions (September-December 2013)Document3 pagesSummary of Significant SC Decisions (September-December 2013)anorith88No ratings yet

- 2010 MORB Volume 2 With Cir. No. 645Document801 pages2010 MORB Volume 2 With Cir. No. 645Thessaloe B. FernandezNo ratings yet

- Dr. Ram Manohar Lohiya National Law University, Lucknow.: JurisprudenceDocument9 pagesDr. Ram Manohar Lohiya National Law University, Lucknow.: JurisprudenceBharat JoshiNo ratings yet

- Labor Relations DigestsDocument10 pagesLabor Relations DigestsRaymer OclaritNo ratings yet

- Ethics Wee Cruzvlim UyDocument1 pageEthics Wee Cruzvlim UyMikMik UyNo ratings yet

- Tax CompiledDocument36 pagesTax CompiledHarold B. LacabaNo ratings yet

- Marjorie A. Apolinar-Petilo, Complainant, V. Atty. Aristedes A. Maramot, Respondent, A.C. No. 9067, January 31, 2018Document3 pagesMarjorie A. Apolinar-Petilo, Complainant, V. Atty. Aristedes A. Maramot, Respondent, A.C. No. 9067, January 31, 2018Karen Joy MasapolNo ratings yet

- CASUPANAN VS LAROYA RULING ON CIVIL ACTION FOR QUASI-DELICTDocument5 pagesCASUPANAN VS LAROYA RULING ON CIVIL ACTION FOR QUASI-DELICTSarah De GuzmanNo ratings yet

- 56-Splp-Castillo Vs Sps CruzDocument2 pages56-Splp-Castillo Vs Sps CruzJoesil Dianne SempronNo ratings yet

- Wee Cruz Vs LimDocument6 pagesWee Cruz Vs LimCyber QuestNo ratings yet

- Sameer Overseas Placement Agency vs. CabilesDocument55 pagesSameer Overseas Placement Agency vs. CabilescyhaaangelaaaNo ratings yet

- Mitsubishi Corporation-Manila Branch, Petitioner, vs. Commissioner of Internal REVENUE, RespondentDocument5 pagesMitsubishi Corporation-Manila Branch, Petitioner, vs. Commissioner of Internal REVENUE, RespondentevilsageNo ratings yet

- Second Division July 25, 2016 G.R. No. 202514 ANNA MARIE L. GUMABON, Petitioner Philippine National Bank, Respondent Decision Brion, J.Document11 pagesSecond Division July 25, 2016 G.R. No. 202514 ANNA MARIE L. GUMABON, Petitioner Philippine National Bank, Respondent Decision Brion, J.Graile Dela CruzNo ratings yet

- Case Law - Project EmployeeDocument4 pagesCase Law - Project EmployeeZeniNo ratings yet

- 283 Manila Hotel Employees Association V Manila HotelDocument3 pages283 Manila Hotel Employees Association V Manila HotelCJ Millena100% (1)

- Facts:: Case DigestDocument4 pagesFacts:: Case DigestjackNo ratings yet

- Padilla v. Globe Asiatique (Effect of Dismissal of Orig Complaint To Counterclaim)Document23 pagesPadilla v. Globe Asiatique (Effect of Dismissal of Orig Complaint To Counterclaim)Yralli MendozaNo ratings yet

- Index of Intention) - As The Statute Is ClearDocument6 pagesIndex of Intention) - As The Statute Is ClearKurt Geeno Du VencerNo ratings yet

- 2 Cayetano vs. MonsodDocument37 pages2 Cayetano vs. MonsodJnhNo ratings yet

- Concerned Citizens V MmdaDocument1 pageConcerned Citizens V Mmdamina villamorNo ratings yet

- Hrs of Divinagracia v. Ruiz DigestDocument1 pageHrs of Divinagracia v. Ruiz Digestcookbooks&lawbooksNo ratings yet

- SEC Determines Prosperity.Com Scheme Not an Investment ContractDocument4 pagesSEC Determines Prosperity.Com Scheme Not an Investment ContractLydia Marie MirabelNo ratings yet

- Supreme Court Rules on Taxation of Airlines Under FranchiseDocument18 pagesSupreme Court Rules on Taxation of Airlines Under Franchisemceline19No ratings yet

- Real Estate Broker's Commission UpheldDocument13 pagesReal Estate Broker's Commission UpheldCamille CruzNo ratings yet

- Silicon Philippines v. CIR: DOCTRINE/S: All Told, The NonDocument3 pagesSilicon Philippines v. CIR: DOCTRINE/S: All Told, The NonDaLe AparejadoNo ratings yet

- Court Update For Reading 2017Document132 pagesCourt Update For Reading 2017chris cardinoNo ratings yet

- Criminal Liability of Corporations Is Not A Universal Feature of Modern Legal SystemsDocument16 pagesCriminal Liability of Corporations Is Not A Universal Feature of Modern Legal SystemsAnonymous d6WYxHlNo ratings yet

- CIR v. Isabela Cultural CorporationDocument14 pagesCIR v. Isabela Cultural CorporationkimNo ratings yet

- Belgian Overseas Chartering and Shipping NDocument3 pagesBelgian Overseas Chartering and Shipping NLatjing SolimanNo ratings yet

- Chapman v. Underwood (MANALASTAS)Document1 pageChapman v. Underwood (MANALASTAS)Arnel ManalastasNo ratings yet

- G.R. No. 122226 March 25, 1998 Mendoza, J:) Will Still Be ExcludedDocument2 pagesG.R. No. 122226 March 25, 1998 Mendoza, J:) Will Still Be ExcludedgerlynNo ratings yet

- CIR v. Fisher ADocument30 pagesCIR v. Fisher ACE SherNo ratings yet

- Sample Investment Policy Statement ADocument4 pagesSample Investment Policy Statement AAna TapiaNo ratings yet

- Outline of Topics Taxation Law ReviewDocument9 pagesOutline of Topics Taxation Law ReviewAlain AlmarioNo ratings yet

- HOME INSURANCE CO v. AMERICAN STEAMSHIP AGENCIESM INC., TRANSPO CASE DIGEST, 4BLM - GROUP TWODocument2 pagesHOME INSURANCE CO v. AMERICAN STEAMSHIP AGENCIESM INC., TRANSPO CASE DIGEST, 4BLM - GROUP TWOMALALA MALALANo ratings yet

- 1 - Funk Brothers Seed Co. v. Kalo Inoculant Co. 333 U.S. 127Document7 pages1 - Funk Brothers Seed Co. v. Kalo Inoculant Co. 333 U.S. 127Michelle CatadmanNo ratings yet

- Santuyo vs. Remerco Garments Vol. Arbitrator Jurisdiction 2010Document8 pagesSantuyo vs. Remerco Garments Vol. Arbitrator Jurisdiction 2010Ulysses RallonNo ratings yet

- Doctrine of Last Clear ChanceDocument5 pagesDoctrine of Last Clear ChanceAnne TGNo ratings yet

- CASE DOCTRINE Labor ReviewDocument22 pagesCASE DOCTRINE Labor Reviewnahjassi mangateNo ratings yet

- Dunlao, SR - Vs.ca, G.r.no. 111342, August 22, 1996Document7 pagesDunlao, SR - Vs.ca, G.r.no. 111342, August 22, 1996gheljoshNo ratings yet

- Engracio Fabre, Jr. vs. Court of AppealsDocument3 pagesEngracio Fabre, Jr. vs. Court of AppealsAlvin ClaridadesNo ratings yet

- 82 Supreme Court Reports Annotated: Philippine Petroleum Corp. vs. Municipality of Pililla, RizalDocument10 pages82 Supreme Court Reports Annotated: Philippine Petroleum Corp. vs. Municipality of Pililla, RizalAaron ReyesNo ratings yet

- 12 Pilapil V Heirs of Maximo BrionesDocument14 pages12 Pilapil V Heirs of Maximo BrionesJed MendozaNo ratings yet

- 126.041 - Latip v. Chua - ARCEODocument2 pages126.041 - Latip v. Chua - ARCEOd9w8jntykjNo ratings yet

- Local TaxationDocument57 pagesLocal TaxationJesterNo ratings yet

- Lico vs. COMELEC, September 29, 2015 PDFDocument21 pagesLico vs. COMELEC, September 29, 2015 PDFNapoleon Sango IIINo ratings yet

- CIR v. SM Prime HoldingsDocument2 pagesCIR v. SM Prime HoldingsBrylle Deeiah TumarongNo ratings yet

- 8 RCBC Vs CIR 2007Document9 pages8 RCBC Vs CIR 2007BLNNo ratings yet

- Codilla v. de VeneciaDocument46 pagesCodilla v. de VeneciaDianneNo ratings yet

- Benjamin Gomez challenges constitutionality of anti-TB stamp requirementDocument1 pageBenjamin Gomez challenges constitutionality of anti-TB stamp requirementanonNo ratings yet

- Puig vs. PenafloridaDocument4 pagesPuig vs. PenafloridaMonikkaNo ratings yet

- BRB23 TaxDocument203 pagesBRB23 TaxIsabella Siggaoat100% (1)

- CIR Vs Euro-Philippines Airline ServicesDocument10 pagesCIR Vs Euro-Philippines Airline ServicesBeltran KathNo ratings yet

- New PPT (Torture)Document23 pagesNew PPT (Torture)Mark PesiganNo ratings yet

- Consti2Digest - Tolentino vs. Secretary of Finance, 235 SCRA 630, GR 115455 (25 August 1994)Document1 pageConsti2Digest - Tolentino vs. Secretary of Finance, 235 SCRA 630, GR 115455 (25 August 1994)Lu CasNo ratings yet

- Villavilla Vs CADocument6 pagesVillavilla Vs CABobby ParksNo ratings yet

- Arellano Vs PascualDocument2 pagesArellano Vs PascualnathNo ratings yet

- NDC v. CIR, 151 SCRA 472 (1987)Document10 pagesNDC v. CIR, 151 SCRA 472 (1987)citizenNo ratings yet

- National Development Company v. CIRDocument7 pagesNational Development Company v. CIRevelyn b t.No ratings yet

- New York Convention E PDFDocument26 pagesNew York Convention E PDFMaraNo ratings yet

- LGU Guide for Rehabilitation and Recovery from COVID-19Document86 pagesLGU Guide for Rehabilitation and Recovery from COVID-19Donald Roland Dela TorreNo ratings yet

- Law 134 Intellectual Property LawDocument11 pagesLaw 134 Intellectual Property LawAna EndayaNo ratings yet

- 10 Request For Interpretation (Cambodia V Thailand) 2013Document2 pages10 Request For Interpretation (Cambodia V Thailand) 2013rgtan3No ratings yet

- 031 - Aquino III vs. Robredo vs. COMELECDocument4 pages031 - Aquino III vs. Robredo vs. COMELECrgtan3No ratings yet

- 20th Century Fox V CADocument4 pages20th Century Fox V CArgtan3No ratings yet

- 033 - Cuenco V CADocument4 pages033 - Cuenco V CArgtan3No ratings yet

- 10 Manila Doctors vs. ChuaDocument2 pages10 Manila Doctors vs. Chuargtan3100% (3)

- 29 Bliss V Cali CoopDocument7 pages29 Bliss V Cali Cooprgtan3No ratings yet

- Villamor v. ComelecDocument2 pagesVillamor v. Comelecrgtan3No ratings yet

- Securities and Exchange Commission: Increase of Capital Stock and Consideration For StockDocument3 pagesSecurities and Exchange Commission: Increase of Capital Stock and Consideration For Stockrgtan3No ratings yet

- Consti 1 Gatmaytan Finals Reviewer PDFDocument130 pagesConsti 1 Gatmaytan Finals Reviewer PDFJulienne AristozaNo ratings yet

- CSC Clearance Rule Inapplicable to JudiciaryDocument1 pageCSC Clearance Rule Inapplicable to Judiciaryrgtan3No ratings yet

- Penera v. COMELEC, AndanarDocument5 pagesPenera v. COMELEC, Andanarrgtan3100% (1)

- Koppel V YatcoDocument2 pagesKoppel V Yatcorgtan3100% (1)

- Mclaran V CrescentDocument5 pagesMclaran V Crescentrgtan3No ratings yet

- Sws & Pulse V Comelec (2015)Document5 pagesSws & Pulse V Comelec (2015)rgtan3No ratings yet

- Criminal Law Review-2020 Part 2 SyllabusDocument11 pagesCriminal Law Review-2020 Part 2 Syllabusrgtan3No ratings yet

- Negotiable Instruments Law Bar QnADocument22 pagesNegotiable Instruments Law Bar QnArgtan3100% (4)

- Pub OffDocument98 pagesPub Offrgtan3No ratings yet

- Villa Rey v. CADocument1 pageVilla Rey v. CArgtan3No ratings yet

- Pub OffDocument98 pagesPub Offrgtan3No ratings yet

- PAL Vs CADocument1 pagePAL Vs CArgtan3No ratings yet

- Cathay Pacific v. VasquezDocument2 pagesCathay Pacific v. Vasquezrgtan3No ratings yet

- Savellano V NorthwestDocument2 pagesSavellano V Northwestrgtan3No ratings yet

- Santiago V COMELECDocument3 pagesSantiago V COMELECrgtan3No ratings yet

- Ortigas Vs Lufthansa (Digest)Document2 pagesOrtigas Vs Lufthansa (Digest)rgtan3No ratings yet

- Savellano V NorthwestDocument2 pagesSavellano V Northwestrgtan3No ratings yet

- CagasDocument19 pagesCagasrgtan3No ratings yet

- Corporate Acts With Voting Requirements FinalDocument4 pagesCorporate Acts With Voting Requirements FinalMela SuarezNo ratings yet

- Quiz 1 (Answer)Document3 pagesQuiz 1 (Answer)Ali SaeedNo ratings yet

- Ds Iron Condor StrategiaDocument43 pagesDs Iron Condor StrategiaFernando ColomerNo ratings yet

- Yu Lim Vs YuDocument6 pagesYu Lim Vs YusandrasulitNo ratings yet

- Confirmation Page PDFDocument1 pageConfirmation Page PDFsaralabitmNo ratings yet

- Security MarketDocument30 pagesSecurity Marketashish_k_srivastavaNo ratings yet

- Wise Transaction Invoice Transfer 814368287 1721868089 TRDocument2 pagesWise Transaction Invoice Transfer 814368287 1721868089 TRhmobgpxwhlugnvplokNo ratings yet

- Unit 1 FIDocument26 pagesUnit 1 FIRohit SinghNo ratings yet

- What Are The Important Functions of MoneyDocument3 pagesWhat Are The Important Functions of MoneyGanesh KaleNo ratings yet

- Sai Hadoop ResumeDocument5 pagesSai Hadoop ResumeSaikumar AvanigaddaNo ratings yet

- BRD transaction reportDocument5 pagesBRD transaction reportDavid GeorgeNo ratings yet

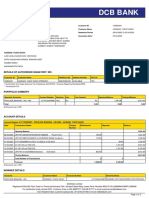

- DCB Bank: Statement of AccountDocument2 pagesDCB Bank: Statement of AccounthasnainNo ratings yet

- Ce Digital Banking Maturity Study EmeaDocument30 pagesCe Digital Banking Maturity Study EmeaRajeevNo ratings yet

- Solved in The Documentary Movie Expelled No Intelligence Allowed TherDocument1 pageSolved in The Documentary Movie Expelled No Intelligence Allowed TherAnbu jaromiaNo ratings yet

- P&S Bylaw 2072 II Amendment in NepaliDocument27 pagesP&S Bylaw 2072 II Amendment in NepaliNarayanPrajapatiNo ratings yet

- D - CCLAACTS - MANUALSRevenueThe Andhra Pradesh Rights in Land and Pattadar Pass Books Act, 1971.Document11 pagesD - CCLAACTS - MANUALSRevenueThe Andhra Pradesh Rights in Land and Pattadar Pass Books Act, 1971.Naveen Kumar RudhraNo ratings yet

- Regional Sales Manager Client Relationship Expert in Denver CO Resume Cynthia ChandlerDocument2 pagesRegional Sales Manager Client Relationship Expert in Denver CO Resume Cynthia ChandlerCynthia ChandlerNo ratings yet

- Telekom Bill: Page 1 of 6Document6 pagesTelekom Bill: Page 1 of 6Zulkhibri ZulNo ratings yet

- Medfield Pharmaceuticals' Valuation and Strategic OptionsDocument9 pagesMedfield Pharmaceuticals' Valuation and Strategic OptionsvATSALANo ratings yet

- Fee Based Activity in India BanksDocument12 pagesFee Based Activity in India BanksMu'ammar RizqiNo ratings yet

- BASIC ACCOUNTING PROCEDURESDocument35 pagesBASIC ACCOUNTING PROCEDURESjune100% (1)

- BPI Capital Audited Financial StatementsDocument66 pagesBPI Capital Audited Financial StatementsGes Glai-em BayabordaNo ratings yet

- Day 1 1.1 Session-1 1.2 Banking System in India: AnswersDocument51 pagesDay 1 1.1 Session-1 1.2 Banking System in India: AnswersAkella LokeshNo ratings yet

- INVITATION FOR FOREIGN LIQUOR SUPPLYDocument37 pagesINVITATION FOR FOREIGN LIQUOR SUPPLYRoddy RodriguesNo ratings yet

- Coastal Pacific Trading Inc. v. Southern Rolling Mills Co., Inc.Document36 pagesCoastal Pacific Trading Inc. v. Southern Rolling Mills Co., Inc.arsalle2014No ratings yet

- Abhishek ReportDocument67 pagesAbhishek ReportAbhishek KarNo ratings yet

- How To Write A Hardship Letter For Mortgage Loan ModificationDocument4 pagesHow To Write A Hardship Letter For Mortgage Loan ModificationMatt Carter100% (1)

- Basel II- RBI Guidelines SummaryDocument70 pagesBasel II- RBI Guidelines SummaryHarsh MehtaNo ratings yet

- UBS Global Real Estate Bubble IndexDocument24 pagesUBS Global Real Estate Bubble IndexKiva DangNo ratings yet

- Indian Economy QuestionsDocument25 pagesIndian Economy QuestionsPadyala SriramNo ratings yet

- Submitted To: Submitted byDocument33 pagesSubmitted To: Submitted byaanaughtyNo ratings yet