You might also like

- Internal Foundations of Corporate GovernanceDocument13 pagesInternal Foundations of Corporate GovernanceArvin0% (2)

- Philippine Debt FPVICLARDocument15 pagesPhilippine Debt FPVICLARenaportillo13No ratings yet

- Sustainable DevelopmentDocument3 pagesSustainable DevelopmentruxuliciphilosNo ratings yet

- Lesson 9.09.20 Financial System in The PhilippinesDocument5 pagesLesson 9.09.20 Financial System in The PhilippinesVatchdemonNo ratings yet

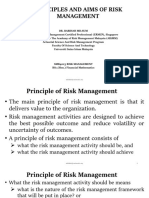

- Principles and Aims of Risk ManagementDocument10 pagesPrinciples and Aims of Risk ManagementAfiq Zaqwan Mohd ZakirNo ratings yet

- Banking Supervision and ExaminationDocument16 pagesBanking Supervision and ExaminationatoydequitNo ratings yet

- ThesisDocument115 pagesThesisL.a.Zumárraga50% (2)

- Code of Ethics For Advertising: Section 1Document20 pagesCode of Ethics For Advertising: Section 1Kym AlgarmeNo ratings yet

- RESEARCH2015-Life Insurance PolicyDocument21 pagesRESEARCH2015-Life Insurance PolicyMary Jane BaliuagNo ratings yet

- Report On Micro FinanceDocument54 pagesReport On Micro Financemohsinmalik07100% (1)

- CB-03 Central Monetary AuthorityDocument7 pagesCB-03 Central Monetary AuthorityJHERRY MIG SEVILLANo ratings yet

- Topic I Introduction To CreditDocument4 pagesTopic I Introduction To CreditLemon OwNo ratings yet

- Clinical Governance: The Challenges of Implementation in IranDocument10 pagesClinical Governance: The Challenges of Implementation in Iransunny100% (1)

- Illegal Termination and ContractualizationDocument25 pagesIllegal Termination and ContractualizationMA. LORRAINE ABELANo ratings yet

- BAPF 102:: Banking and Financial InstitutionsDocument11 pagesBAPF 102:: Banking and Financial Institutionsbad geniusNo ratings yet

- Essay On Flexible LearningDocument4 pagesEssay On Flexible LearningNathan Atkins0% (1)

- What Is Financial RiskDocument9 pagesWhat Is Financial RiskDeboit BhattacharjeeNo ratings yet

- Personal FinanceDocument21 pagesPersonal FinanceBench AndayaNo ratings yet

- CreditCollection ModulesDocument71 pagesCreditCollection ModulesShaina Angel FulgencioNo ratings yet

- Chap 13Document5 pagesChap 13Jade Marie FerrolinoNo ratings yet

- Proposal Covid 19Document3 pagesProposal Covid 19ninafatima allam0% (1)

- Aeco136 - Final Term Report (Manatal Multipurpose Cooperatives)Document20 pagesAeco136 - Final Term Report (Manatal Multipurpose Cooperatives)JoyDianneGumatayNo ratings yet

- PNBDocument3 pagesPNBLove KarenNo ratings yet

- Ama Bank Business CaseDocument4 pagesAma Bank Business Caserogimel trinidadNo ratings yet

- Role of Non-Depository Financial InstitutionDocument9 pagesRole of Non-Depository Financial InstitutionFaye AritchetaNo ratings yet

- Case AnalysisDocument13 pagesCase AnalysisBarry Rayven CutaranNo ratings yet

- Introduction To Mutual Fund and Its Various AspectsDocument46 pagesIntroduction To Mutual Fund and Its Various AspectsNaazlah SadafNo ratings yet

- BTR Functions Draft 6-1-15Document16 pagesBTR Functions Draft 6-1-15Hanna PentiñoNo ratings yet

- Microinsurance ProjectDocument59 pagesMicroinsurance Projectmayur9664501232No ratings yet

- MAHUSAYLAW211 REFLECTIVE ESSAY - Module 3Document3 pagesMAHUSAYLAW211 REFLECTIVE ESSAY - Module 3Jeth MahusayNo ratings yet

- What Are The Potential Applications of Nanotechnology in The Philippines?Document2 pagesWhat Are The Potential Applications of Nanotechnology in The Philippines?Sarah GNo ratings yet

- Insurance Services - Types of Insurers and Marketing SystemDocument44 pagesInsurance Services - Types of Insurers and Marketing SystemnineeshkkNo ratings yet

- Financial Literacy (Done)Document5 pagesFinancial Literacy (Done)Joseph Paul VERDANNo ratings yet

- Sources of Long Term FinanceDocument14 pagesSources of Long Term FinanceRakesh GuptaNo ratings yet

- Cooperative PDFDocument5 pagesCooperative PDFDenise Nicole CuarteroNo ratings yet

- Reflection ObliconDocument1 pageReflection ObliconLyncee Domingo100% (1)

- Delinquency ManagementDocument4 pagesDelinquency ManagementJeff SmithNo ratings yet

- Methods of Measuring RiskDocument7 pagesMethods of Measuring RiskOvais GodilNo ratings yet

- Reflection Paper "How COVID-19 Affected Business Industries?"Document3 pagesReflection Paper "How COVID-19 Affected Business Industries?"Briann Sophia Reyes100% (1)

- What Are Capital Markets?Document5 pagesWhat Are Capital Markets?Aijaz KhajaNo ratings yet

- First Community Cooperative (Ficco) Balingasag Mis. Or. BranchDocument5 pagesFirst Community Cooperative (Ficco) Balingasag Mis. Or. BranchJapet Jose EcuacionNo ratings yet

- What Are The Two Major Perceptions of Time, and How Does Each Affect International Business? AnswerDocument2 pagesWhat Are The Two Major Perceptions of Time, and How Does Each Affect International Business? AnswerVikram KumarNo ratings yet

- Open Letter To ChedDocument2 pagesOpen Letter To Chedwmesa7770% (1)

- Define What Are These Tools and Describe How These Two Tools Affect The Performance of An OrganizationDocument2 pagesDefine What Are These Tools and Describe How These Two Tools Affect The Performance of An OrganizationCorrine Kylah PasteleroNo ratings yet

- Credit C7Document14 pagesCredit C7Chantelle Ishi Macatangay AquinoNo ratings yet

- Malalim Multi-Purpose CooperativeDocument11 pagesMalalim Multi-Purpose CooperativeAngelica P. CoracheaNo ratings yet

- Stop TB Program - Envisioning A Tuberculosis Free World, The Goal of TheDocument4 pagesStop TB Program - Envisioning A Tuberculosis Free World, The Goal of TheCharles Mart Rabe-Rodriguez HortilanoNo ratings yet

- Formation of Stock PortfoliosDocument11 pagesFormation of Stock PortfoliosJoe Garcia50% (2)

- Monetary Policies of BSPDocument5 pagesMonetary Policies of BSPNardsdel RiveraNo ratings yet

- Notrel Networks Case StudyDocument15 pagesNotrel Networks Case StudyGiora KetterNo ratings yet

- Credit Instruments Power PointDocument11 pagesCredit Instruments Power PointEd Leen Ü80% (10)

- Effects of Globalization in The PhilippinesDocument2 pagesEffects of Globalization in The PhilippinesEdmar OducayenNo ratings yet

- BSA2A WrittenReports Thrift-BanksDocument5 pagesBSA2A WrittenReports Thrift-Banksrobert pilapilNo ratings yet

- Credit and Collection Module 3Document2 pagesCredit and Collection Module 3aivan john CañadillaNo ratings yet

- 2016 Sss Guidebook PDFDocument128 pages2016 Sss Guidebook PDFagent_ros9956100% (1)

- Ateneo Multi-Purpose CooperativeDocument32 pagesAteneo Multi-Purpose CooperativeBlessy DomerNo ratings yet

- Interest Rates and Their Role in FinanceDocument17 pagesInterest Rates and Their Role in FinanceClyden Jaile RamirezNo ratings yet

- 1 SM PDFDocument17 pages1 SM PDFMharisa Amisola HernandezNo ratings yet

- $ - Upreme !court: L/epubltt of TBTDocument15 pages$ - Upreme !court: L/epubltt of TBTWinnie Ann Daquil Lomosad-MisagalNo ratings yet

- Seminar Code of EthicsDocument1 pageSeminar Code of Ethicspa3ckblancoNo ratings yet

- Caseclassification NewDocument2 pagesCaseclassification Newpa3ckblancoNo ratings yet

- 217 TWG Voluntourism Best PracticesDocument26 pages217 TWG Voluntourism Best Practicespa3ckblancoNo ratings yet

- Asean Plus 3 Solicitation LetterDocument2 pagesAsean Plus 3 Solicitation Letterpa3ckblancoNo ratings yet

- Seminar Code of EthicsDocument1 pageSeminar Code of Ethicspa3ckblancoNo ratings yet

- Civil Law Reviewer Lopez-RosarioDocument47 pagesCivil Law Reviewer Lopez-RosarioCrnc Navidad100% (7)

- How To Win Every Argument PDFDocument196 pagesHow To Win Every Argument PDFRice RS100% (7)

- Evidence Part 1 PDFDocument26 pagesEvidence Part 1 PDFpa3ckblancoNo ratings yet

- TRAIN LawDocument5 pagesTRAIN Lawpa3ckblancoNo ratings yet

- Blank Gad Accomplishment Report Fy 2017 1Document9 pagesBlank Gad Accomplishment Report Fy 2017 1pa3ckblancoNo ratings yet

- 6Document25 pages6pa3ckblancoNo ratings yet

- PhilippinesDocument11 pagesPhilippinespa3ckblancoNo ratings yet

- Evidence Part 1 PDFDocument26 pagesEvidence Part 1 PDFpa3ckblancoNo ratings yet

- 2017 PCW Endorsed Gad Plan and BudgetDocument7 pages2017 PCW Endorsed Gad Plan and Budgetpa3ckblancoNo ratings yet

- Guidelines For Preparing and Submitting Building Permit Application FormsDocument2 pagesGuidelines For Preparing and Submitting Building Permit Application FormsRobert Paredes DimapilisNo ratings yet

- Crim Law - PeraltaDocument118 pagesCrim Law - PeraltaJin Siclon60% (5)

- Sample Volunteer Code of EthicsDocument1 pageSample Volunteer Code of Ethicspa3ckblancoNo ratings yet

- Volunteer Probation Assistants of Quezon City Parole and Probation Office No. 1Document1 pageVolunteer Probation Assistants of Quezon City Parole and Probation Office No. 1pa3ckblancoNo ratings yet

- Procedure For OccupancyDocument1 pageProcedure For Occupancypa3ckblancoNo ratings yet

- Procedure For Bldg. Permit RegularDocument1 pageProcedure For Bldg. Permit Regularpa3ckblanco100% (1)

- Demolition PermitDocument1 pageDemolition Permitpa3ckblancoNo ratings yet

- Motion To Release Motor VehicleDocument1 pageMotion To Release Motor Vehiclepa3ckblancoNo ratings yet

- Procedure For Demolition PermitDocument1 pageProcedure For Demolition Permitpa3ckblanco100% (1)

- No79 31PA Carrillo PDFDocument14 pagesNo79 31PA Carrillo PDFpa3ckblancoNo ratings yet

- Petition Philippine Bar Exam For New ApplicantsDocument3 pagesPetition Philippine Bar Exam For New ApplicantsGil ValdezNo ratings yet

- Affidavit of DenialDocument9 pagesAffidavit of Denialpa3ckblancoNo ratings yet

- Affidavit of DenialDocument5 pagesAffidavit of Denialpa3ckblanco100% (1)

- Mr. Geronimo V. Francisco: Attention: Cancellations DepartmentDocument1 pageMr. Geronimo V. Francisco: Attention: Cancellations Departmentpa3ckblancoNo ratings yet

- Insurance Official OutlineDocument60 pagesInsurance Official OutlineDylan WheelerNo ratings yet

- Philippine International Trade Corp v. COA, G.R. No. 183517, June 22, 2010Document1 pagePhilippine International Trade Corp v. COA, G.R. No. 183517, June 22, 2010MonicaCelineCaroNo ratings yet

- Bajaj Bike 2019 - RemovedDocument2 pagesBajaj Bike 2019 - Removedsarath potnuriNo ratings yet

- (Summary) Charley's Steak HouseDocument3 pages(Summary) Charley's Steak HouseArihant patilNo ratings yet

- Ic 88 MCQDocument78 pagesIc 88 MCQSamba SivaNo ratings yet

- BS 8418: 2015 Installation and Remote Monitoring of Detector-Activated CCTV Systems - Code of PracticeDocument10 pagesBS 8418: 2015 Installation and Remote Monitoring of Detector-Activated CCTV Systems - Code of PracticemuchlisonNo ratings yet

- 2016 MOC - MWS Training PresentationDocument8 pages2016 MOC - MWS Training PresentationDragosNeaguNo ratings yet

- Premium Double InsuranceDocument9 pagesPremium Double InsuranceLDNo ratings yet

- For a special whole life insurance on (x), payable at the moment of death: (i) , δ (iii) The death benefit at time t is, - (iv)Document70 pagesFor a special whole life insurance on (x), payable at the moment of death: (i) , δ (iii) The death benefit at time t is, - (iv)BrianHillz-maticNo ratings yet

- Straddles and Trend Following: Case #10166365Document18 pagesStraddles and Trend Following: Case #101663655ty5No ratings yet

- Accenture Compliance Excellence Insurance Industry PDFDocument37 pagesAccenture Compliance Excellence Insurance Industry PDFsharon omashNo ratings yet

- Airline Charges ReportDocument25 pagesAirline Charges ReportbobbytronicNo ratings yet

- Contract of Adhesion - FinalDocument15 pagesContract of Adhesion - FinalDebashish DashNo ratings yet

- General Provisions: Supreme CourtDocument165 pagesGeneral Provisions: Supreme CourtJohn Adrian MaulionNo ratings yet

- Generate COIDocument2 pagesGenerate COIsaumitra ghogaleNo ratings yet

- InsuranceDocument29 pagesInsuranceMdms PayoeNo ratings yet

- Seven Principles of Insurance With ExamplesDocument7 pagesSeven Principles of Insurance With Examplessagar111033No ratings yet

- EC2066 Exam Commentary - May 2023Document21 pagesEC2066 Exam Commentary - May 2023the.multituorNo ratings yet

- AllState Insurance CompanyDocument14 pagesAllState Insurance CompanyNazish Sohail50% (2)

- InsuranceDocument5 pagesInsuranceMayroseTAquinoNo ratings yet

- Lawrence MattielloDocument2 pagesLawrence MattielloCAP History LibraryNo ratings yet

- RFBT - Law On CooperativesDocument6 pagesRFBT - Law On CooperativeseunicemaraNo ratings yet

- Edillon v. Manila Bankers Life, 1982Document1 pageEdillon v. Manila Bankers Life, 1982Randy SiosonNo ratings yet

- BCIS Tutorial PDFDocument13 pagesBCIS Tutorial PDFAryan AroraNo ratings yet

- WeHnMa1 - CA0l Agenda AandB CWC Puri 2 PDFDocument320 pagesWeHnMa1 - CA0l Agenda AandB CWC Puri 2 PDFRavi SrivastavaNo ratings yet

- FY 2019-20 Proposed BudgetDocument506 pagesFY 2019-20 Proposed BudgetMaritza NunezNo ratings yet

- Risk Management Solution Manual Chapter 01Document7 pagesRisk Management Solution Manual Chapter 01DanielLam100% (5)

- 904 New Jeevan Arogya PresentationDocument2 pages904 New Jeevan Arogya PresentationDhiman NaskarNo ratings yet

- ACCFA v. Alpha IncDocument5 pagesACCFA v. Alpha IncAnonymous nYvtSgoQNo ratings yet

- Acknowledgment Receipt: Loan Account Number: 3901092273Document1 pageAcknowledgment Receipt: Loan Account Number: 3901092273HERMAN DAGIONo ratings yet