You might also like

- Haribhakt Com Spectral Analysis of Vedic Mantra E0 A5 90 OmDocument15 pagesHaribhakt Com Spectral Analysis of Vedic Mantra E0 A5 90 Omron9123No ratings yet

- Haribhakt Com Fake Big Bang Theories Problems Is FalseDocument23 pagesHaribhakt Com Fake Big Bang Theories Problems Is Falseron9123No ratings yet

- Haribhakt Com Secrets of The Tanjore Thanjavur Big Temple BuDocument64 pagesHaribhakt Com Secrets of The Tanjore Thanjavur Big Temple Buron9123No ratings yet

- Haribhakt Com Brain Waves Theory of Bhagavad Gitas ConsciousDocument20 pagesHaribhakt Com Brain Waves Theory of Bhagavad Gitas Consciousron9123100% (1)

- Example SmallDocument26 pagesExample Smallron9123No ratings yet

- Algotrading Prezo v1 5 130204183501 Phpapp01 PDFDocument52 pagesAlgotrading Prezo v1 5 130204183501 Phpapp01 PDFron9123No ratings yet

- My Winning StrategyDocument30 pagesMy Winning Strategyron9123No ratings yet

- gd2dfgdf59287596 Vimshottari DashaDocument10 pagesgd2dfgdf59287596 Vimshottari Dasharon9123No ratings yet

- How To Understand A Renko ChartDocument18 pagesHow To Understand A Renko Chartron9123No ratings yet

- Asdper TrendDocument30 pagesAsdper Trendron9123No ratings yet

- Sensex: The Barometer of The Indian Capital MarketDocument2 pagesSensex: The Barometer of The Indian Capital Marketron9123No ratings yet

- Weird World PDFDocument67 pagesWeird World PDFAllanki Sanyasi Rao67% (6)

- D3rajendra Chola I 6292Document28 pagesD3rajendra Chola I 6292ron9123No ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

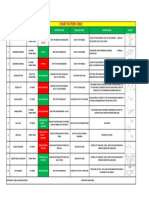

- Chart Pattern Table: S.No Types of Chart Pattern Found Trend Pattern Interpretation Measure Target Identification SymbolDocument1 pageChart Pattern Table: S.No Types of Chart Pattern Found Trend Pattern Interpretation Measure Target Identification SymbolGoogleuser googleNo ratings yet

- Beams AdvAcc11 Chapter12 PDFDocument9 pagesBeams AdvAcc11 Chapter12 PDFBellaNovindraNo ratings yet

- Exercise On Csofp - Mixed TartDocument3 pagesExercise On Csofp - Mixed TartNoor ShukirrahNo ratings yet

- Case 1 - DOMINOS - Group 6 - January 2021Document8 pagesCase 1 - DOMINOS - Group 6 - January 2021Jeffrey O'LearyNo ratings yet

- Mie L1 AbDocument38 pagesMie L1 AbSakshi MNo ratings yet

- ReportDocument1 pageReportarun_algoNo ratings yet

- Walt Disney Yen Financing I - Group 8Document6 pagesWalt Disney Yen Financing I - Group 8Sonal Choudhary100% (1)

- MARK4210 Class 2 Quantitative Analysis CompleteDocument18 pagesMARK4210 Class 2 Quantitative Analysis CompleteCandy ChoNo ratings yet

- URP Unrealised ProfitDocument2 pagesURP Unrealised ProfitruvaNo ratings yet

- A Guide To Investing in REITs - Intelligent Income by Simply Safe Dividends PDFDocument30 pagesA Guide To Investing in REITs - Intelligent Income by Simply Safe Dividends PDFRuTz92No ratings yet

- Treasury ManagementDocument10 pagesTreasury Managementrakeshrakesh1No ratings yet

- Barila Spa - Ans-1 & Ans-3Document2 pagesBarila Spa - Ans-1 & Ans-3SiddharthNo ratings yet

- Commercial Paper in IndiaDocument8 pagesCommercial Paper in IndiaMalyala JagadeeshNo ratings yet

- Walmart Swaps Case Study Interest Rate SwapsDocument12 pagesWalmart Swaps Case Study Interest Rate SwapsSimonaltkorn0% (2)

- Study of Stock Market Working FrameworkDocument13 pagesStudy of Stock Market Working Frameworkbenjoel1209No ratings yet

- Relative Valuations FINALDocument44 pagesRelative Valuations FINALChinmay ShirsatNo ratings yet

- Investment in Equity SecuritiesDocument4 pagesInvestment in Equity Securitieselsana philipNo ratings yet

- Investment Funds in Luxembourg - September 2017Document547 pagesInvestment Funds in Luxembourg - September 2017morticNo ratings yet

- Digital MarketingDocument21 pagesDigital Marketingsrivalli vabilisettyNo ratings yet

- p1139 WilsonDocument8 pagesp1139 WilsondnvnNo ratings yet

- EVULUS Staking Progressive EnglishDocument20 pagesEVULUS Staking Progressive EnglishSindhu ThomasNo ratings yet

- Explanation of Goodbelly Sales Spreadsheet: Variable Definitions 1 2 3 4 5 6 7 8 9Document38 pagesExplanation of Goodbelly Sales Spreadsheet: Variable Definitions 1 2 3 4 5 6 7 8 9nkjhlhNo ratings yet

- MBA (FB&E) 2019-21: Submitted To: Dr. Meeta MunshiDocument8 pagesMBA (FB&E) 2019-21: Submitted To: Dr. Meeta MunshinancyNo ratings yet

- Case Study 2 HW 4 BRICS CountriesDocument6 pagesCase Study 2 HW 4 BRICS CountriesmilagrosNo ratings yet

- Uv5631 Xls EngDocument37 pagesUv5631 Xls EngCarmelita EsclandaNo ratings yet

- Chapter 12-Capital Structure: Multiple ChoiceDocument22 pagesChapter 12-Capital Structure: Multiple ChoiceadssdasdsadNo ratings yet

- Porters Analysis For ITC Cigarette IndustryDocument8 pagesPorters Analysis For ITC Cigarette IndustryRajesh KumarNo ratings yet

- Strategic Financial MGT!Document35 pagesStrategic Financial MGT!Richie Fiel GacutnoNo ratings yet

- Sample MidTerm Multiple Choice Spring 2018Document3 pagesSample MidTerm Multiple Choice Spring 2018Barbie LCNo ratings yet

- Planet MicroCap Review Q3 2022Document120 pagesPlanet MicroCap Review Q3 2022Planet MicroCap Review MagazineNo ratings yet