You might also like

- Comparative Analysis of Financial Statements of Pacetel Systems PVT LTD.' Using Accounting RatiosDocument12 pagesComparative Analysis of Financial Statements of Pacetel Systems PVT LTD.' Using Accounting RatiosYashraj vashishtNo ratings yet

- Presentation - Performance Management System IhclDocument7 pagesPresentation - Performance Management System IhclArijit DasNo ratings yet

- OpenView 2021 Financial and Operating Benchmarks ReportDocument58 pagesOpenView 2021 Financial and Operating Benchmarks ReportrrNo ratings yet

- Siemens Business Fact SheetsDocument7 pagesSiemens Business Fact SheetsahadjayaNo ratings yet

- Financial DepartmentDocument27 pagesFinancial DepartmentPiyu VyasNo ratings yet

- Byco Petroleum Pakistan LimitedDocument22 pagesByco Petroleum Pakistan LimitedHamna RizwanNo ratings yet

- C3 - SRV - MIO UpdatingDocument6 pagesC3 - SRV - MIO UpdatingKhincho ayeNo ratings yet

- C3 - SRV - MIO UpdatingDocument6 pagesC3 - SRV - MIO UpdatingKhincho ayeNo ratings yet

- C3 - SRV - MIO UpdatingDocument6 pagesC3 - SRV - MIO UpdatingKhincho ayeNo ratings yet

- Earnings Presentation: Bse Code: 524558 - Nse Symbol: Neulandlab - Bloomberg: Nll:In - Reuters: Neul - NsDocument34 pagesEarnings Presentation: Bse Code: 524558 - Nse Symbol: Neulandlab - Bloomberg: Nll:In - Reuters: Neul - Nssunil.dasarath jadhavNo ratings yet

- 2020 SaaS Benchmarks Deck VFINALDocument53 pages2020 SaaS Benchmarks Deck VFINALAbcd123411No ratings yet

- F3 - SRV - Gross Profit MarginDocument5 pagesF3 - SRV - Gross Profit MarginKhincho ayeNo ratings yet

- 38 Business Development KPI Accountabilities SOP 2021 07 30Document10 pages38 Business Development KPI Accountabilities SOP 2021 07 30Michael DuggerNo ratings yet

- Corporate CFRA ASSIGNMENTDocument11 pagesCorporate CFRA ASSIGNMENTHimanshu NagvaniNo ratings yet

- Financial and Strategic Analysis of Arpak International Investment LimitedDocument17 pagesFinancial and Strategic Analysis of Arpak International Investment LimitedFaria AlamNo ratings yet

- Uber Q4 23 Earnings Supplemental DataDocument28 pagesUber Q4 23 Earnings Supplemental Datadivbrown0No ratings yet

- Sbi PPTDocument59 pagesSbi PPTmisfitmedicoNo ratings yet

- Ezz Steel Financial AnalysisDocument31 pagesEzz Steel Financial Analysismohamed ashorNo ratings yet

- AMZN Financials Spring 2023abDocument47 pagesAMZN Financials Spring 2023abuma sainiNo ratings yet

- Financial Performance Impacts Compensation Options: Technical FeatureDocument8 pagesFinancial Performance Impacts Compensation Options: Technical FeatureBasil OguakaNo ratings yet

- M004/CL02 Managerial Finance Coursework 1 Assignment Brief Guidelines and RubricDocument10 pagesM004/CL02 Managerial Finance Coursework 1 Assignment Brief Guidelines and RubricPooja thangarajaNo ratings yet

- FinancialAnalysis - EQUIPOS DEL NORTEDocument6 pagesFinancialAnalysis - EQUIPOS DEL NORTEOscar TrujilloNo ratings yet

- Bonus CalculationsDocument2 pagesBonus CalculationsGeetika BhargavaNo ratings yet

- Horizontal and Vertical Analysis of Maruti SuzukiDocument31 pagesHorizontal and Vertical Analysis of Maruti SuzukiAnushka GuptaNo ratings yet

- 2020 Performance Pay Sales Incentive Sample ReportDocument9 pages2020 Performance Pay Sales Incentive Sample ReportDendi AlfiandiNo ratings yet

- Key Performance IndicatorsDocument6 pagesKey Performance IndicatorsEmmanuel AkoloNo ratings yet

- Aleman HaDocument4 pagesAleman Harborgesdossantos37No ratings yet

- Audit A Financial Model With Macabacus (Complete)Document7 pagesAudit A Financial Model With Macabacus (Complete)Kayerinna PardosiNo ratings yet

- Edel India Strategy 5 Pathways To EfficiencyDocument40 pagesEdel India Strategy 5 Pathways To EfficiencyarhagarNo ratings yet

- GLOBUSSPR - Investor Presentation - 16-Jun-21 - TickertapeDocument29 pagesGLOBUSSPR - Investor Presentation - 16-Jun-21 - Tickertapepiyush rohiraNo ratings yet

- Ambev Presentation Dec.19Document22 pagesAmbev Presentation Dec.19arthurNo ratings yet

- Module 7 Financial Statement AnalysisDocument20 pagesModule 7 Financial Statement AnalysisHailsey WinterNo ratings yet

- CRM Q1 FY23 Earnings Press Release W FinancialsDocument16 pagesCRM Q1 FY23 Earnings Press Release W Financialsstan LeeNo ratings yet

- Vertical Analysis 1. Asset Management, or Turnover, Ratios: A. Inventory TurnoverDocument5 pagesVertical Analysis 1. Asset Management, or Turnover, Ratios: A. Inventory TurnoverNhi ChuNo ratings yet

- Vertical Analysis 1. Asset Management, or Turnover, Ratios: A. Inventory TurnoverDocument5 pagesVertical Analysis 1. Asset Management, or Turnover, Ratios: A. Inventory TurnoverNhi ChuNo ratings yet

- Efficiency Ratios: Analysis - OutcomeDocument2 pagesEfficiency Ratios: Analysis - OutcomeManisha JhunjhunwalaNo ratings yet

- Internal Forces G, HDocument6 pagesInternal Forces G, HRui JiaNo ratings yet

- ZOES WB Presentation June17 (1) 2017Document29 pagesZOES WB Presentation June17 (1) 2017Ala BasterNo ratings yet

- Vertical Analysis Tabung HajiDocument6 pagesVertical Analysis Tabung HajiRyuzanna JubaidiNo ratings yet

- Presentation H1 2022Document43 pagesPresentation H1 2022Tran Thi ThuongNo ratings yet

- Employee Performance Assessment Form Staff Id: Staff Name:: Key Performance Indicators (Kpis)Document8 pagesEmployee Performance Assessment Form Staff Id: Staff Name:: Key Performance Indicators (Kpis)Victor ImehNo ratings yet

- CM Proje Ect FinalDocument14 pagesCM Proje Ect FinalSarah AliNo ratings yet

- RatioanalyasisDocument20 pagesRatioanalyasiscknowledge10No ratings yet

- FINMAN 3 - FINANCIAL-ANALYSIS-DiscussionDocument16 pagesFINMAN 3 - FINANCIAL-ANALYSIS-Discussionstel mariNo ratings yet

- Business ConsultationDocument16 pagesBusiness ConsultationKim Nicole ReyesNo ratings yet

- Real Time S & OP With APCC: Chandra Pandey - Director Supply ChainDocument43 pagesReal Time S & OP With APCC: Chandra Pandey - Director Supply ChainSanjeev ThakurNo ratings yet

- BF Group Assignment Group 3 (Hero MotoCorp)Document21 pagesBF Group Assignment Group 3 (Hero MotoCorp)Shiva KrishnanNo ratings yet

- 47047bosfinal p5 cp8Document89 pages47047bosfinal p5 cp8Mitali SharmaNo ratings yet

- Anandam CompanyDocument8 pagesAnandam CompanyNarinderNo ratings yet

- Annual Employee Bonus Plan - Target - BonusDocument7 pagesAnnual Employee Bonus Plan - Target - BonuspgalegoNo ratings yet

- Monthly Performance Report Craig Design and LandscapingDocument14 pagesMonthly Performance Report Craig Design and LandscapingShahnawaz JavedNo ratings yet

- Finance KPI Dashboard Someka Excel Template V6 Free Version 2Document11 pagesFinance KPI Dashboard Someka Excel Template V6 Free Version 2Arun GargNo ratings yet

- Padini Business Risk and Financial Risk AnalysisDocument8 pagesPadini Business Risk and Financial Risk AnalysisCheng Chung leeNo ratings yet

- CAF608833F3F75B7Document47 pagesCAF608833F3F75B7BrahimNo ratings yet

- Sak Case 20.3Document14 pagesSak Case 20.3Kemala Putri AyundaNo ratings yet

- Aldine WestfieldDocument250 pagesAldine WestfieldJafarNo ratings yet

- Laundry Care in Peru DatagraphicsDocument4 pagesLaundry Care in Peru DatagraphicsDanitza Villazana GómezNo ratings yet

- Omkar WCDocument14 pagesOmkar WComNo ratings yet

- Template of Financial Plan - 22.03.2017Document27 pagesTemplate of Financial Plan - 22.03.2017jpsmu09No ratings yet

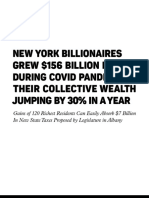

- Investinournewyork BillionairepandemicprofitDocument9 pagesInvestinournewyork BillionairepandemicprofitZacharyEJWilliamsNo ratings yet

- Investinournewyork BillionairepandemicprofitDocument9 pagesInvestinournewyork BillionairepandemicprofitZacharyEJWilliamsNo ratings yet

- Hochul 2022 Snapchat BuysDocument3 pagesHochul 2022 Snapchat BuysZacharyEJWilliamsNo ratings yet

- Clergy Letter To Governor Andrew Cuomo, Mayor Bill de Blasio, and New York State and City Elected Officials at Every Level.Document4 pagesClergy Letter To Governor Andrew Cuomo, Mayor Bill de Blasio, and New York State and City Elected Officials at Every Level.ZacharyEJWilliamsNo ratings yet

- Data For Progress PollDocument2 pagesData For Progress PollZacharyEJWilliamsNo ratings yet

- 0226.OPWDD Letter From MembersDocument2 pages0226.OPWDD Letter From MembersZacharyEJWilliamsNo ratings yet

- State Senate One House Budget Proposal Press ReleaseDocument10 pagesState Senate One House Budget Proposal Press ReleaseZacharyEJWilliams100% (1)

- Statement On Shutdown of NYC Schools From Citizens' Committee For Children of New YorkDocument1 pageStatement On Shutdown of NYC Schools From Citizens' Committee For Children of New YorkZacharyEJWilliamsNo ratings yet

- WFP LegislativeAgendaDocument2 pagesWFP LegislativeAgendaZacharyEJWilliamsNo ratings yet

- Assembly Senate Response.2.10.21. Final PDFDocument16 pagesAssembly Senate Response.2.10.21. Final PDFZacharyEJWilliamsNo ratings yet

- Group Letter To DOB On State Budget Withholding Transparency 12.21.20Document3 pagesGroup Letter To DOB On State Budget Withholding Transparency 12.21.20ZacharyEJWilliamsNo ratings yet

- Justice Roadmap 2021Document8 pagesJustice Roadmap 2021ZacharyEJWilliamsNo ratings yet

- Test and Trace RFP Dec 11Document17 pagesTest and Trace RFP Dec 11ZacharyEJWilliams100% (1)

- FINAL Food Insecurity Letter To Governor Oct 2020Document5 pagesFINAL Food Insecurity Letter To Governor Oct 2020ZacharyEJWilliamsNo ratings yet

- Sean Ryan Senate 60 Press Release 071520 2Document1 pageSean Ryan Senate 60 Press Release 071520 2ZacharyEJWilliamsNo ratings yet

- Dark Storm Industries V CuomoDocument34 pagesDark Storm Industries V CuomoZacharyEJWilliamsNo ratings yet

- Ibig 04 08Document45 pagesIbig 04 08Russell KimNo ratings yet

- Working Capital Management: University of CalicutDocument19 pagesWorking Capital Management: University of CalicutRam IyerNo ratings yet

- SBA Loan ChartDocument2 pagesSBA Loan ChartsbdcwtNo ratings yet

- Class 02Document3 pagesClass 02Aasim Bin BakrNo ratings yet

- Chapter 07 Positive Accounting TheoryDocument15 pagesChapter 07 Positive Accounting Theorymehrabshawn75% (4)

- CORPORATE GOVERNANCE AND ENRON CASE FinalDocument14 pagesCORPORATE GOVERNANCE AND ENRON CASE FinalAllyah Paula PostorNo ratings yet

- MatbisDocument8 pagesMatbisAditya DzikirNo ratings yet

- CDP Preparation Template Form 3c.1Document6 pagesCDP Preparation Template Form 3c.1Princess Hayria B. PiangNo ratings yet

- 1.Bd InitialaDocument4,241 pages1.Bd InitialaCorovei EmiliaNo ratings yet

- Home Improvement Loan-618: NF-546 NF - 964 NF-990 NF-967 NF-482 NF-803Document3 pagesHome Improvement Loan-618: NF-546 NF - 964 NF-990 NF-967 NF-482 NF-803Santosh KumarNo ratings yet

- Oblicon - NovationDocument3 pagesOblicon - NovationKaila Mae Tan DuNo ratings yet

- IkigaiDocument287 pagesIkigaiMuhammad Edwansyah RissalNo ratings yet

- Walmart Inc.: Consolidated Cash Flow StatementDocument2 pagesWalmart Inc.: Consolidated Cash Flow StatementThanh Phương TrịnhNo ratings yet

- Loan Mortgage Agreement On Sangla Tira - BobilesDocument2 pagesLoan Mortgage Agreement On Sangla Tira - BobilesJake EspinolNo ratings yet

- Reporte EstrategiaDocument15 pagesReporte EstrategiaCarolina GialdiNo ratings yet

- Essays Sample Questions - Parts 1 & 2Document54 pagesEssays Sample Questions - Parts 1 & 2Krizia Almiranez100% (1)

- List If Exempt - Zero Rated Supplies - UgandaDocument7 pagesList If Exempt - Zero Rated Supplies - UgandaArthur AsiimweNo ratings yet

- Courts and Banks - Effects of Judicial Enforcement On Credit MarketsDocument43 pagesCourts and Banks - Effects of Judicial Enforcement On Credit Marketsvidovdan9852No ratings yet

- Notice: Grant and Cooperative Agreement Awards: General Deputy Assistant Secretary For Housing-Deputy Federal Housing Commissioner Et Al.Document3 pagesNotice: Grant and Cooperative Agreement Awards: General Deputy Assistant Secretary For Housing-Deputy Federal Housing Commissioner Et Al.Justia.comNo ratings yet

- DuPont System of Analysis-HODocument1 pageDuPont System of Analysis-HOSyed Noman AhmedNo ratings yet

- Ratio AnalysisDocument15 pagesRatio Analysiskidhur faizal rifoyNo ratings yet

- Financial Analysis TATA STEElDocument18 pagesFinancial Analysis TATA STEElneha mundraNo ratings yet

- PFIN3 3rd Edition Gitman Solutions Manual 1Document36 pagesPFIN3 3rd Edition Gitman Solutions Manual 1rebeccabuckwecfyrisgj100% (24)

- Moody's Certificate in Commercail CreditDocument8 pagesMoody's Certificate in Commercail CreditExplore with TejuNo ratings yet

- Abiy MogesDocument67 pagesAbiy MogesMelesNo ratings yet

- 6 Impact of MgnregaDocument9 pages6 Impact of Mgnrega21BEC107 ASHOKNo ratings yet

- 10 - Borrowing Costs PS 12edDocument15 pages10 - Borrowing Costs PS 12edbusiness docNo ratings yet

- Sample of Loan Agreement - ContractDocument3 pagesSample of Loan Agreement - ContractYuriNo ratings yet

- PF - Chapter 2 - Personal Financial Statement - For STDocument14 pagesPF - Chapter 2 - Personal Financial Statement - For STTrung Lê BáNo ratings yet

- Amfi IapDocument30 pagesAmfi IapAshish AgarwalNo ratings yet