You might also like

- Taxation in Ghana: a Fiscal Policy Tool for Development: 75 Years ResearchFrom EverandTaxation in Ghana: a Fiscal Policy Tool for Development: 75 Years ResearchRating: 5 out of 5 stars5/5 (1)

- UP-Law 2016 Tax Bar ExamDocument23 pagesUP-Law 2016 Tax Bar Examrobertoii_suarez67% (3)

- Suggested Answers To The 2017 Bar Examinations in Taxation LawDocument15 pagesSuggested Answers To The 2017 Bar Examinations in Taxation LawRyan S. GodChild100% (2)

- Taxation Law Bar Examination 2019 Suggested AnswersDocument18 pagesTaxation Law Bar Examination 2019 Suggested AnswersSuzy93% (44)

- 2018 Taxation Bar Questions and AnswersDocument14 pages2018 Taxation Bar Questions and AnswersAlexLesle Roble100% (7)

- Suggested Answers To The 2017 Bar Examination Questions in Commercial Law Up Law Complex - Pinay JuristDocument43 pagesSuggested Answers To The 2017 Bar Examination Questions in Commercial Law Up Law Complex - Pinay JuristMark Pimentel100% (5)

- 2014-2019 TAXATION LAW BAR Questions and AnswersDocument81 pages2014-2019 TAXATION LAW BAR Questions and AnswersJuris Mendoza72% (18)

- 2018 Mercantile Law Suggested Answer (Incomplete)Document10 pages2018 Mercantile Law Suggested Answer (Incomplete)Victoria Denise Monte80% (5)

- Corpo Reviewer MiraviteDocument94 pagesCorpo Reviewer MiraviteGianne Vazquez75% (4)

- Mercantile Law Bar Questions (1990-2013)Document61 pagesMercantile Law Bar Questions (1990-2013)Frances Anne Gamboa100% (4)

- Transportation Laws Bar QsDocument3 pagesTransportation Laws Bar QsJao Santos56% (16)

- 2015 Taxation Law Bar Q and A by BSCDocument13 pages2015 Taxation Law Bar Q and A by BSCBumbo S. Cruz60% (5)

- Compiled BarQs Insurance LawDocument54 pagesCompiled BarQs Insurance LawCelinka Chun100% (1)

- 2008 Bar Examination Questions Ans Answers Legal Ethics and Practical Exercises XDocument4 pages2008 Bar Examination Questions Ans Answers Legal Ethics and Practical Exercises XronasoldeNo ratings yet

- Z Company stock disputeDocument13 pagesZ Company stock disputeFaithy Darna100% (11)

- FRANCISCO, CYRIL CLEOPE - FinalsDocument2 pagesFRANCISCO, CYRIL CLEOPE - FinalsBass TēhNo ratings yet

- 2017 Remedial Suggested AnswerDocument24 pages2017 Remedial Suggested Answernahjassi mangate100% (1)

- Lim - Tax Reviewer PDFDocument217 pagesLim - Tax Reviewer PDFHarris Camposano100% (4)

- Suggested Answers For 2019 Bar ExamsDocument5 pagesSuggested Answers For 2019 Bar ExamsJyrus Cimatu40% (5)

- 2015 Last Minute Reminders For Taxation Law by Atty. Noel Ortega-1Document28 pages2015 Last Minute Reminders For Taxation Law by Atty. Noel Ortega-1heirarchy67% (3)

- 2007-2013 Taxation Law Philippine Bar Examination Questions and Suggested Answers (JayArhSals&Ladot)Document125 pages2007-2013 Taxation Law Philippine Bar Examination Questions and Suggested Answers (JayArhSals&Ladot)Jay-Arh93% (98)

- Taxation Bar Questions (Multiple Choice Questions and Answers)Document81 pagesTaxation Bar Questions (Multiple Choice Questions and Answers)Anonymous Mickey Mouse100% (1)

- 2019 BOC Taxation Law Reviewer PDFDocument295 pages2019 BOC Taxation Law Reviewer PDFEdu Fajardo100% (2)

- Insurance Bar Questions CompilationDocument63 pagesInsurance Bar Questions CompilationMaria90% (10)

- Rakham's loan to Alfonso deemed non-deductible bad debtDocument17 pagesRakham's loan to Alfonso deemed non-deductible bad debtClarince Joyce Lao DoroyNo ratings yet

- Taxation Law PrinciplesDocument86 pagesTaxation Law PrinciplesEdmart Vicedo100% (1)

- Will Contest Succession RightsDocument5 pagesWill Contest Succession RightsAnonymous lokXJkc7l7100% (1)

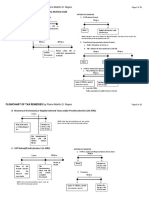

- Flowchart of Tax Remedies I. Remedies UnDocument12 pagesFlowchart of Tax Remedies I. Remedies UnKevin Ken Sison Ganchero100% (2)

- Tax 1 Mock BarDocument8 pagesTax 1 Mock BarMarco RvsNo ratings yet

- RemediesDocument45 pagesRemediesCzarina100% (1)

- Mercantile Law 2 SACP Rocille Tambasacan PDFDocument25 pagesMercantile Law 2 SACP Rocille Tambasacan PDFEduard Loberez ReyesNo ratings yet

- 2012 Bar Exam in Mercantile LawDocument102 pages2012 Bar Exam in Mercantile Lawtere_aquinoluna828No ratings yet

- Taxation Bar QuestionsDocument65 pagesTaxation Bar QuestionsJazz Adaza100% (1)

- 2016 TAXATION BAR QUESTION With Suggested AnswerDocument3 pages2016 TAXATION BAR QUESTION With Suggested AnswerGail Fabroa Navarra90% (10)

- Taxation Review Midterm ExamDocument19 pagesTaxation Review Midterm ExamGreggy Law100% (1)

- 1990-1991 Bar Examination QuestionsDocument13 pages1990-1991 Bar Examination Questionsdecemberssy100% (1)

- Differences between antichresis and usufructDocument2 pagesDifferences between antichresis and usufructRae DarNo ratings yet

- Remedial Law Bar 2018 With Suggested AnswersDocument100 pagesRemedial Law Bar 2018 With Suggested AnswersJed Takoy Paracha84% (19)

- Bar Exam Qs Taxation LawDocument123 pagesBar Exam Qs Taxation LawUlyssesNo ratings yet

- 193606-2016-Toenec Phils. Inc. v. Commissioner ofDocument10 pages193606-2016-Toenec Phils. Inc. v. Commissioner ofJunieNo ratings yet

- Bar QA Taxation 2010-2015Document238 pagesBar QA Taxation 2010-2015poontin rilakkuma100% (2)

- 2000 BAR EXAMINATION IN MERCANTILE LAW QUESTIONS AND ANSWERSDocument16 pages2000 BAR EXAMINATION IN MERCANTILE LAW QUESTIONS AND ANSWERSsirenangblue100% (4)

- 2019 Bar Questions and Suggested Answers PDFDocument28 pages2019 Bar Questions and Suggested Answers PDFKarl Shariff Ajihil100% (5)

- Single Borrowers LimitDocument10 pagesSingle Borrowers LimitCamille LamadoNo ratings yet

- 2010 BAR EXAMINATION PART IDocument295 pages2010 BAR EXAMINATION PART IRachel Ann B. Abion67% (3)

- 2017 Bar Q and ADocument7 pages2017 Bar Q and AAnonymous Mickey MouseNo ratings yet

- Up Law Complex: Uggested Answers To The 2017 Bar Examination Questions in TaxationDocument9 pagesUp Law Complex: Uggested Answers To The 2017 Bar Examination Questions in TaxationNissi JonnaNo ratings yet

- 2017 Taxation Law Bar QsDocument12 pages2017 Taxation Law Bar QsCj CarabbacanNo ratings yet

- TAXATION LAW BAR QUESTIONSDocument6 pagesTAXATION LAW BAR QUESTIONSBayan Ng RamonNo ratings yet

- Pinay Jurist: Suggested Answers To The 2017 Bar Examination Questions in Taxation Up Law ComplexDocument20 pagesPinay Jurist: Suggested Answers To The 2017 Bar Examination Questions in Taxation Up Law ComplexLogia LegisNo ratings yet

- 2017 Bar ExaminationsDocument12 pages2017 Bar ExaminationsLei BumanlagNo ratings yet

- Taxation Law Bar Questions 2017Document7 pagesTaxation Law Bar Questions 2017manol_salaNo ratings yet

- Tax 2017 Bar Q&aDocument12 pagesTax 2017 Bar Q&aRODNA JEMA GREMILLE RE ALENTONNo ratings yet

- 2017 Bar Exams Questions in Taxation LawDocument7 pages2017 Bar Exams Questions in Taxation LawJade Marlu DelaTorre100% (1)

- 2017 Bar Exams Taxation LawDocument15 pages2017 Bar Exams Taxation Lawrobertpeter_aNo ratings yet

- 2017 Bar - Taxation LawDocument5 pages2017 Bar - Taxation LawMiamor NatividadNo ratings yet

- 2015 Tax Law 1-6Document5 pages2015 Tax Law 1-6Tokie TokiNo ratings yet

- 2007 Bar ExaminationDocument14 pages2007 Bar ExaminationHaRry PeregrinoNo ratings yet

- TAX (2017) Bar QDocument6 pagesTAX (2017) Bar Qkhan lebronNo ratings yet

- Taxation Law Bar Q and A 2014 To 2017Document40 pagesTaxation Law Bar Q and A 2014 To 2017Garfit BumacasNo ratings yet

- Mercantile Bar Q and Answers 2017Document18 pagesMercantile Bar Q and Answers 2017Imma FoosaNo ratings yet

- Municipal Trial Court in Cities: Republic of The Philippines 4 Judicial Region Branch 1 Antipolo, RizalDocument2 pagesMunicipal Trial Court in Cities: Republic of The Philippines 4 Judicial Region Branch 1 Antipolo, RizalImma FoosaNo ratings yet

- Documentary Stamp TaxDocument6 pagesDocumentary Stamp TaxImma FoosaNo ratings yet

- Bar Exam Suggested Answers - 2017 Labor Law Bar Q&A AUGUST 31, 2018 2017 Labor Law Bar Questions and AnswersDocument17 pagesBar Exam Suggested Answers - 2017 Labor Law Bar Q&A AUGUST 31, 2018 2017 Labor Law Bar Questions and AnswersImma FoosaNo ratings yet

- Consti CasesDocument1 pageConsti Caseskrys_elleNo ratings yet

- Could There BeDocument1 pageCould There BeImma FoosaNo ratings yet

- 2017 Civil Law Bar Q&A Suggested AnswersDocument17 pages2017 Civil Law Bar Q&A Suggested AnswersImma FoosaNo ratings yet

- 2017 Civil Law Bar Q&A Suggested AnswersDocument17 pages2017 Civil Law Bar Q&A Suggested AnswersImma FoosaNo ratings yet

- 2018 Current EventsDocument1 page2018 Current EventsImma FoosaNo ratings yet

- Lawyers OathDocument4 pagesLawyers OathImma FoosaNo ratings yet

- PALS Bar Ops Pilipinas Must Read Cases CIVIL 2015Document167 pagesPALS Bar Ops Pilipinas Must Read Cases CIVIL 2015Hea ManNo ratings yet

- Lawyers OathDocument4 pagesLawyers OathImma FoosaNo ratings yet

- Social JusticeDocument1 pageSocial JusticeAngelinwhite FernandezNo ratings yet

- Constitution of The PhilippinesDocument2 pagesConstitution of The PhilippinesImma FoosaNo ratings yet

- Enrile v. SandiganbayanDocument15 pagesEnrile v. SandiganbayanImma FoosaNo ratings yet

- 2011 NLRC Procedure (As Amended) FlowchartDocument3 pages2011 NLRC Procedure (As Amended) FlowchartShine BillonesNo ratings yet

- Labor Relations Case DigestDocument10 pagesLabor Relations Case DigestImma FoosaNo ratings yet

- RP vs MERALCO dispute over electricity chargesDocument47 pagesRP vs MERALCO dispute over electricity chargesImma FoosaNo ratings yet

- Labor Relations Case DigestDocument23 pagesLabor Relations Case DigestImma FoosaNo ratings yet

- Eastern Shipping Lines, Inc. Vs AntonioDocument12 pagesEastern Shipping Lines, Inc. Vs AntonioImma FoosaNo ratings yet

- Civil ProcedureDocument3 pagesCivil ProcedureImma FoosaNo ratings yet

- Labor Relations Case DigestDocument10 pagesLabor Relations Case DigestImma FoosaNo ratings yet

- Labor Relations Case DigestDocument10 pagesLabor Relations Case DigestImma FoosaNo ratings yet

- Case Digest Torts and DamagesDocument16 pagesCase Digest Torts and DamagesImma FoosaNo ratings yet

- CIR vs. YMCADocument14 pagesCIR vs. YMCAJoshua CuentoNo ratings yet

- Commissioner of Internal Revenue v. GCL Retirement Plan G.R. 95022Document6 pagesCommissioner of Internal Revenue v. GCL Retirement Plan G.R. 95022Dino Bernard LapitanNo ratings yet

- Salaries and Benefits For The Public Sector: Assistant Secretary Myrna S. Chua Department of Budget and ManagementDocument30 pagesSalaries and Benefits For The Public Sector: Assistant Secretary Myrna S. Chua Department of Budget and ManagementNascelAguilarGabitoNo ratings yet

- Bir - Train Tot - Transfer TaxesDocument14 pagesBir - Train Tot - Transfer TaxesGlo GanzonNo ratings yet

- Tax Exemptin and ConcessionDocument38 pagesTax Exemptin and ConcessionAdil ShresthaNo ratings yet

- AWS - Terms and ConditionsDocument12 pagesAWS - Terms and Conditionshect ProfileNo ratings yet

- PAGCOR Vs BIRDocument14 pagesPAGCOR Vs BIRGladys BantilanNo ratings yet

- Donor's Tax Basics, Exemptions and AdviceDocument5 pagesDonor's Tax Basics, Exemptions and AdviceJunivenReyUmadhayNo ratings yet

- How To Save Capital Gain Tax On Sale of Residential House Under Section 54 - Taxguru - inDocument2 pagesHow To Save Capital Gain Tax On Sale of Residential House Under Section 54 - Taxguru - inRoster BabaNo ratings yet

- 2020 IRR of RA 11256Document4 pages2020 IRR of RA 11256Karla Elaine UmaliNo ratings yet

- Midterm (Assignment (1) Income TaxationDocument3 pagesMidterm (Assignment (1) Income TaxationMark Emil BaritNo ratings yet

- Expanded Senior Citizens Act (7432)Document28 pagesExpanded Senior Citizens Act (7432)Mae Joan AbanNo ratings yet

- Chevron V BIRDocument6 pagesChevron V BIRMark Anthony AlvarioNo ratings yet

- Record KeepingDocument11 pagesRecord Keepingr.jeyashankar9550No ratings yet

- Real Property Taxation: by Atty Agnes SantosDocument22 pagesReal Property Taxation: by Atty Agnes SantosJulienne A Argosino100% (1)

- SEIA Solar Tax Manual V9.0 2018 September ES TOCDocument11 pagesSEIA Solar Tax Manual V9.0 2018 September ES TOCLoren LyleNo ratings yet

- United States Statutes at LargeDocument33 pagesUnited States Statutes at Largewealth2520100% (5)

- Salary INCOME - ITDocument64 pagesSalary INCOME - ITHrishikesh AshtaputreNo ratings yet

- Smart v. City of DavaoDocument9 pagesSmart v. City of DavaoEvelyn TocgongnaNo ratings yet

- Abra College V Aquino DigestDocument1 pageAbra College V Aquino DigestNicoleNo ratings yet

- Income Tax Quick Recap CapsulDocument24 pagesIncome Tax Quick Recap CapsulAmanNo ratings yet

- Colorado Corporate Income Tax GuideDocument42 pagesColorado Corporate Income Tax Guideneo kNo ratings yet

- Form 231Document9 pagesForm 231sanjay jadhav100% (5)

- CIR Vs Gen FoodsDocument12 pagesCIR Vs Gen FoodsOlivia JaneNo ratings yet

- Ch4 - Gross IncomeDocument10 pagesCh4 - Gross IncomeJuan FrivaldoNo ratings yet

- GST Digest: Issue No.7 Period: Aug 2021 To Sep 2021Document46 pagesGST Digest: Issue No.7 Period: Aug 2021 To Sep 2021Vraj PatelNo ratings yet

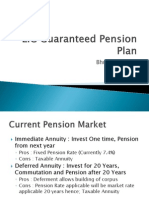

- LIC Guaranteed HNI Pension PlanDocument9 pagesLIC Guaranteed HNI Pension PlanBhushan ShethNo ratings yet

- Pansacola v. CIRDocument3 pagesPansacola v. CIRSean GalvezNo ratings yet

- Revised BGM On GST Vol2 PDFDocument503 pagesRevised BGM On GST Vol2 PDFJAINo ratings yet

- Holy Spirit Sciences Ministries of AmaracapanaDocument1 pageHoly Spirit Sciences Ministries of AmaracapanaDhakiy M Aqiel ElNo ratings yet

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesFrom EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesRating: 4 out of 5 stars4/5 (9)

- Tax Accounting: A Guide for Small Business Owners Wanting to Understand Tax Deductions, and Taxes Related to Payroll, LLCs, Self-Employment, S Corps, and C CorporationsFrom EverandTax Accounting: A Guide for Small Business Owners Wanting to Understand Tax Deductions, and Taxes Related to Payroll, LLCs, Self-Employment, S Corps, and C CorporationsRating: 4 out of 5 stars4/5 (1)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProFrom EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProRating: 4.5 out of 5 stars4.5/5 (43)

- The Payroll Book: A Guide for Small Businesses and StartupsFrom EverandThe Payroll Book: A Guide for Small Businesses and StartupsRating: 5 out of 5 stars5/5 (1)

- Owner Operator Trucking Business Startup: How to Start Your Own Commercial Freight Carrier Trucking Business With Little Money. Bonus: Licenses and Permits ChecklistFrom EverandOwner Operator Trucking Business Startup: How to Start Your Own Commercial Freight Carrier Trucking Business With Little Money. Bonus: Licenses and Permits ChecklistRating: 5 out of 5 stars5/5 (6)

- Deduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesFrom EverandDeduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesRating: 3 out of 5 stars3/5 (3)

- How to get US Bank Account for Non US ResidentFrom EverandHow to get US Bank Account for Non US ResidentRating: 5 out of 5 stars5/5 (1)

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingFrom EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingRating: 5 out of 5 stars5/5 (3)

- Bookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessFrom EverandBookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessRating: 5 out of 5 stars5/5 (5)

- Invested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)From EverandInvested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)Rating: 4.5 out of 5 stars4.5/5 (43)

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyFrom EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo ratings yet

- What Everyone Needs to Know about Tax: An Introduction to the UK Tax SystemFrom EverandWhat Everyone Needs to Know about Tax: An Introduction to the UK Tax SystemNo ratings yet

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Reduce Taxes for Business, Investing, & More.From EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Reduce Taxes for Business, Investing, & More.No ratings yet

- The Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyFrom EverandThe Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyRating: 4 out of 5 stars4/5 (52)

- How To Get IRS Tax Relief: The Complete Tax Resolution Guide for IRS: Back Tax Problems & Settlements, Offer in Compromise, Payment Plans, Federal Tax Liens & Levies, Penalty Abatement, and Much MoreFrom EverandHow To Get IRS Tax Relief: The Complete Tax Resolution Guide for IRS: Back Tax Problems & Settlements, Offer in Compromise, Payment Plans, Federal Tax Liens & Levies, Penalty Abatement, and Much MoreNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet