You might also like

- Research Proposal On Corporate GovernanceDocument12 pagesResearch Proposal On Corporate GovernanceOlabanjo Shefiu Olamiji60% (5)

- Kitchen Jad Jsa RevisedDocument2 pagesKitchen Jad Jsa Revisedsinghajitb100% (3)

- Understanding Salary Breakup, Salary Structure, and Salary ComponentsDocument11 pagesUnderstanding Salary Breakup, Salary Structure, and Salary ComponentsDoss MartinNo ratings yet

- Amazon ValuationDocument65 pagesAmazon ValuationJahangir Khan50% (2)

- Club Accounts Questions PDFDocument38 pagesClub Accounts Questions PDFSimra Riyaz100% (1)

- Commercial Bank Creditand Manufacturing Sector OutputDocument9 pagesCommercial Bank Creditand Manufacturing Sector OutputemmanuelNo ratings yet

- 15 JurnalDocument9 pages15 JurnalAditya SaputraNo ratings yet

- Literature Review On Central Bank of NigeriaDocument4 pagesLiterature Review On Central Bank of Nigeriaafmzdabdjteegf100% (1)

- Capital Structureand Profitabilityof Deposit Money BanksDocument13 pagesCapital Structureand Profitabilityof Deposit Money BanksRaja RehanNo ratings yet

- Investment Banking Activities in Nigeria A CriticaDocument12 pagesInvestment Banking Activities in Nigeria A Criticanuredin yimamNo ratings yet

- Oloye and OsumaDocument19 pagesOloye and OsumamwambusiNo ratings yet

- Recapitalization and Banks Performance ADocument17 pagesRecapitalization and Banks Performance AGREEN FIELD AGRO HI- TECH SERVICES SANGAMNER.No ratings yet

- Reform Research and Innovation in The Financial Sector of Nigeria: Diversity Issues and ChallengesDocument15 pagesReform Research and Innovation in The Financial Sector of Nigeria: Diversity Issues and ChallengesMalcolm ChristopherNo ratings yet

- The Use of Public Relations Strategies by Commercial Banks During The Recapitalisation of The Banking Sector in Nigeria (2004 - 2009)Document13 pagesThe Use of Public Relations Strategies by Commercial Banks During The Recapitalisation of The Banking Sector in Nigeria (2004 - 2009)Eslem ÇakırNo ratings yet

- Bank Credit and Capital Formation in Nigeria: January 2016Document13 pagesBank Credit and Capital Formation in Nigeria: January 2016Joel ChineduNo ratings yet

- The Impactof Interest Rate Liberalizationon SavingsandDocument8 pagesThe Impactof Interest Rate Liberalizationon SavingsandAhmad Muhammad SalamNo ratings yet

- The Effect of Banks Profitability On Economic Growth in NigeriaDocument9 pagesThe Effect of Banks Profitability On Economic Growth in NigeriaBurim GashiNo ratings yet

- Determinants of Dividend Payout of FinanDocument6 pagesDeterminants of Dividend Payout of Finanmobil daniNo ratings yet

- Literature Review of Commercial Banks in NigeriaDocument8 pagesLiterature Review of Commercial Banks in Nigeriagpnovecnd100% (1)

- Budgeting and Budgetary Control in The Manufacturing Sector of NigeriaDocument14 pagesBudgeting and Budgetary Control in The Manufacturing Sector of NigeriaNeha NMNo ratings yet

- Mergers and Acquisition: The Solution To The Problem of Ineffective Financial Intermediation in The Nigerian Banking SystemDocument14 pagesMergers and Acquisition: The Solution To The Problem of Ineffective Financial Intermediation in The Nigerian Banking Systemsajedul islamNo ratings yet

- Corporate Governance and Bank Performance: A Pooled Study of Selected Banks in NigeriaDocument10 pagesCorporate Governance and Bank Performance: A Pooled Study of Selected Banks in Nigeriamanishaamba7547No ratings yet

- Corporate Governance and Financial Performance ofDocument7 pagesCorporate Governance and Financial Performance ofadegokeoladayo0106No ratings yet

- The Performances of Commercial Banks in Post-ConsolidationDocument12 pagesThe Performances of Commercial Banks in Post-ConsolidationharmedluvNo ratings yet

- Online Banking Thesis PaperDocument6 pagesOnline Banking Thesis Paperlelaretzlaffsiouxfalls100% (3)

- A Panel Data Analysis of The Impact of Informality On The Liquidity of Deposit Money Banks in Nigeria1Document16 pagesA Panel Data Analysis of The Impact of Informality On The Liquidity of Deposit Money Banks in Nigeria1Binod SharmaNo ratings yet

- Determinants of Commercial Banks' Lending Behavior in NigeriaDocument12 pagesDeterminants of Commercial Banks' Lending Behavior in NigeriavqhNo ratings yet

- Ownership Structure and Financial Disclosure Quality: Evidence From Listed Firms in NigeriaDocument10 pagesOwnership Structure and Financial Disclosure Quality: Evidence From Listed Firms in NigeriaSumon Kumar DasNo ratings yet

- OopoDocument8 pagesOopoLasta MaharjanNo ratings yet

- 6db1 PDFDocument8 pages6db1 PDFDuy Khanh HaNo ratings yet

- PaperPublication 11ToyinOgunwaleDocument10 pagesPaperPublication 11ToyinOgunwaleDia Norce GanitaNo ratings yet

- Euroeconomica: Banking System Stability and Economic Growth in Nigeria: A Bounds Test To CointegrationDocument15 pagesEuroeconomica: Banking System Stability and Economic Growth in Nigeria: A Bounds Test To CointegrationOloche UdenyiNo ratings yet

- Chapter One 1.0 1.1 Background of The StudyDocument17 pagesChapter One 1.0 1.1 Background of The StudyEkoh EnduranceNo ratings yet

- Thesis Banking UnionDocument8 pagesThesis Banking UnionJanelle Martinez100% (2)

- Banking Stability in NigeriaDocument11 pagesBanking Stability in NigeriaSeye KareemNo ratings yet

- Comparative Analysis of The Impact of Mergers Andacquisitions On Financial Efficiency of Banks in NigeriaDocument7 pagesComparative Analysis of The Impact of Mergers Andacquisitions On Financial Efficiency of Banks in NigeriaArdi GunardiNo ratings yet

- Cashless Policy and Performance of Banks in NigeriaDocument16 pagesCashless Policy and Performance of Banks in NigeriaResearch ParkNo ratings yet

- Research Paper On Profitability Analysis of BanksDocument6 pagesResearch Paper On Profitability Analysis of Banksgvw6y2hv100% (1)

- Ahzizat SummaryDocument12 pagesAhzizat Summaryolasmart OluwaleNo ratings yet

- Literature Review Non Performing LoansDocument12 pagesLiterature Review Non Performing Loansaflsjcibl100% (1)

- Determinnt of Banking Profitability - 2Document5 pagesDeterminnt of Banking Profitability - 2thaonguyenpeoctieuNo ratings yet

- Agboola 2019 IOP Conf. Ser. Earth Environ. Sci. 331 012014Document9 pagesAgboola 2019 IOP Conf. Ser. Earth Environ. Sci. 331 012014Naol FramNo ratings yet

- 814-Article Text-2273-1-10-20240217 2Document11 pages814-Article Text-2273-1-10-20240217 2michaelmatuta36No ratings yet

- JETIR1906667Document9 pagesJETIR1906667Pooja MNo ratings yet

- BankingDocument12 pagesBankingedhaNo ratings yet

- Banking Research Papers in IndiaDocument9 pagesBanking Research Papers in Indiausbxsqznd100% (1)

- The Impact of Banking Consolidation On The Economic Development of NigeriaDocument8 pagesThe Impact of Banking Consolidation On The Economic Development of NigeriaShahbaz MerajNo ratings yet

- Research Journal of Social ScienceDocument7 pagesResearch Journal of Social Scienceshiva ranjaniNo ratings yet

- Effect of Deposit Money Bank Failure On Economic Development of Nigeria, 2009 2019Document13 pagesEffect of Deposit Money Bank Failure On Economic Development of Nigeria, 2009 2019Editor IJTSRDNo ratings yet

- Literature Review On Capital Market in NigeriaDocument6 pagesLiterature Review On Capital Market in Nigeriaafmzubkeaydllz100% (1)

- Oloye and OsumaDocument18 pagesOloye and OsumaagathaNo ratings yet

- Banking Stability in Nigeria-1Document33 pagesBanking Stability in Nigeria-1Seye KareemNo ratings yet

- Literature Review On Microfinance Institutions in UgandaDocument9 pagesLiterature Review On Microfinance Institutions in UgandakbcymacndNo ratings yet

- Journal 5Document8 pagesJournal 5tesoriosachiNo ratings yet

- New Publication2Document25 pagesNew Publication2Kanbiro OrkaidoNo ratings yet

- Chapter TwoDocument21 pagesChapter Twoafolabidairo5No ratings yet

- Research Paper On Npa of BanksDocument4 pagesResearch Paper On Npa of Banksiqfjzqulg100% (1)

- IS-15 MicrofinanceDocument349 pagesIS-15 MicrofinancePururaja AjsNo ratings yet

- The Implacations of Bank Consolidation in NigeriaDocument16 pagesThe Implacations of Bank Consolidation in Nigeriarotimioladun100% (2)

- Factors Affecting Sacco Membership in Kenya: A Case of Nairobi CountyDocument14 pagesFactors Affecting Sacco Membership in Kenya: A Case of Nairobi CountyKevin OdhiamboNo ratings yet

- Mypublication 2Document22 pagesMypublication 2Folashade ObajeNo ratings yet

- Merger & Acquisition PROJECTDocument49 pagesMerger & Acquisition PROJECTYUSUF DABONo ratings yet

- An Empirical Analysis of Effect of Capital Structure On Firm PerformanceDocument15 pagesAn Empirical Analysis of Effect of Capital Structure On Firm PerformanceDivine KingNo ratings yet

- Literaure ReviewDocument13 pagesLiteraure ReviewRavneet SinghNo ratings yet

- Monitor Your Temperature:: Fever Is 100.4°f/38°c or HigherDocument1 pageMonitor Your Temperature:: Fever Is 100.4°f/38°c or HighersinghajitbNo ratings yet

- DNU, DangDocument30 pagesDNU, DangsinghajitbNo ratings yet

- Safety Data SheetDocument3 pagesSafety Data SheetsinghajitbNo ratings yet

- 8.5.1 Air Emissions AIR EmissionDocument4 pages8.5.1 Air Emissions AIR EmissionsinghajitbNo ratings yet

- Guns, Firearms & WeaponsDocument1 pageGuns, Firearms & WeaponssinghajitbNo ratings yet

- Jad Construction Limited: Fal Form - Nil ListDocument1 pageJad Construction Limited: Fal Form - Nil ListsinghajitbNo ratings yet

- Do Not UseDocument15 pagesDo Not UsesinghajitbNo ratings yet

- ComitDocument2 pagesComitsinghajitbNo ratings yet

- JustDocument2 pagesJustsinghajitbNo ratings yet

- CMCLDocument1 pageCMCLsinghajitbNo ratings yet

- Medical Content BFTDocument1 pageMedical Content BFTsinghajitbNo ratings yet

- When Was The Neptune DiscoveredDocument1 pageWhen Was The Neptune DiscoveredsinghajitbNo ratings yet

- Jad - Heavy Lift ServicesDocument6 pagesJad - Heavy Lift ServicessinghajitbNo ratings yet

- When Was The Neptune DiscoveredDocument1 pageWhen Was The Neptune DiscoveredsinghajitbNo ratings yet

- 25M CelebrationDocument1 page25M CelebrationsinghajitbNo ratings yet

- JustDocument2 pagesJustsinghajitbNo ratings yet

- Section 2 Fire Safety Measures 2.1.1 Structural Fire ProtectionDocument15 pagesSection 2 Fire Safety Measures 2.1.1 Structural Fire ProtectionsinghajitbNo ratings yet

- Training EvaluationDocument1 pageTraining EvaluationsinghajitbNo ratings yet

- ComitDocument2 pagesComitsinghajitbNo ratings yet

- GibraltarDocument4 pagesGibraltarsinghajitbNo ratings yet

- When Was The Neptune DiscoveredDocument1 pageWhen Was The Neptune DiscoveredsinghajitbNo ratings yet

- Oil FishDocument1 pageOil FishsinghajitbNo ratings yet

- Champion Fuel Hose Cert - Page3 1 InchDocument1 pageChampion Fuel Hose Cert - Page3 1 InchsinghajitbNo ratings yet

- Capella University - PHD in Public Safety With em SpecializaDocument2 pagesCapella University - PHD in Public Safety With em SpecializasinghajitbNo ratings yet

- Champion Fuel Hose Cert - Page2 2 InchDocument1 pageChampion Fuel Hose Cert - Page2 2 InchsinghajitbNo ratings yet

- Neptune The Wild ChildDocument1 pageNeptune The Wild ChildsinghajitbNo ratings yet

- ISO 14001 Revision FAQ 2015Document4 pagesISO 14001 Revision FAQ 2015abidafifaNo ratings yet

- List of Prohibited Items On VesselDocument1 pageList of Prohibited Items On VesselsinghajitbNo ratings yet

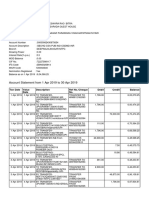

- Statement of Account: State Bank of IndiaDocument10 pagesStatement of Account: State Bank of IndiaKalpa RNo ratings yet

- HBL DebitCard Terms and Conditions - Conventional and Islamic PDFDocument43 pagesHBL DebitCard Terms and Conditions - Conventional and Islamic PDFJAWAD KHALIDNo ratings yet

- Iso8583 150204013523 Conversion Gate02 PDFDocument29 pagesIso8583 150204013523 Conversion Gate02 PDFhvalolaNo ratings yet

- What Is FinanceDocument3 pagesWhat Is FinanceBelle IbarraNo ratings yet

- 01601519370Document10 pages01601519370Alagar Shanmugam SNo ratings yet

- Loan Modification/Loss Mitigation Contacts and Phone Numbers ListDocument6 pagesLoan Modification/Loss Mitigation Contacts and Phone Numbers ListSteve Linnin100% (11)

- IBTDocument2 pagesIBTAmethyst NocelladoNo ratings yet

- World Bank Finance Details For TanescoDocument115 pagesWorld Bank Finance Details For TanescoAmani KeenjaNo ratings yet

- 15624702052231UoGssBO9TQOUnD5 PDFDocument5 pages15624702052231UoGssBO9TQOUnD5 PDFvenkateshbitraNo ratings yet

- CCDocument5 pagesCCchamadi18100% (1)

- Chapter 7 Vs Chapter 13 BankruptcyDocument2 pagesChapter 7 Vs Chapter 13 BankruptcyInternalJoy100% (1)

- 19 Jul 2023Document9 pages19 Jul 2023farahmusa100% (1)

- VSA-IRS Business LawDocument32 pagesVSA-IRS Business LawjpbluejnNo ratings yet

- PsDocument1 pagePsCarrie EvansNo ratings yet

- Dr. OgagaDocument108 pagesDr. Ogagamichaelaye64No ratings yet

- United States v. Behenna, 1st Cir. (1995)Document22 pagesUnited States v. Behenna, 1st Cir. (1995)Scribd Government DocsNo ratings yet

- Canara Bank PPT by Komal NathDocument11 pagesCanara Bank PPT by Komal Nathkomal_nath23No ratings yet

- FAQDocument58 pagesFAQvivekluvinNo ratings yet

- SMC ProjectDocument34 pagesSMC Projectpiyush solankiNo ratings yet

- Fida Et Al 2020 Impact of Service Quality On Customer Loyalty and Customer Satisfaction in Islamic Banks in TheDocument10 pagesFida Et Al 2020 Impact of Service Quality On Customer Loyalty and Customer Satisfaction in Islamic Banks in TheMelissa SantosoNo ratings yet

- Economics Assignment 2Document3 pagesEconomics Assignment 2Amar ChotaiNo ratings yet

- VP Equity Analyst CVDocument5 pagesVP Equity Analyst CVZolo ZoloNo ratings yet

- A Project Report On Depository System inDocument27 pagesA Project Report On Depository System ingupthaNo ratings yet

- Marketing of Bank Services: A Case Study Slovak Banks: Adriana Csikosova Maria Janošková (Antošová)Document16 pagesMarketing of Bank Services: A Case Study Slovak Banks: Adriana Csikosova Maria Janošková (Antošová)Rajan SreedharanNo ratings yet

- Complaint-Affidavit: Office of The City ProsecutorDocument7 pagesComplaint-Affidavit: Office of The City ProsecutorMark LojeroNo ratings yet

- Summer Internship Report On Chengalpattu Urban BankDocument29 pagesSummer Internship Report On Chengalpattu Urban BankAliasgar Patanwala40% (5)

- Chapter 7: Business Contracts in Islam: 4PM-7PM FST-BK 6.3 Group 5Document23 pagesChapter 7: Business Contracts in Islam: 4PM-7PM FST-BK 6.3 Group 5iman zainuddinNo ratings yet