You might also like

- Taxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCFrom EverandTaxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCRating: 4 out of 5 stars4/5 (5)

- Tax Sales for Rookies: A Beginner’s Guide to Understanding Property Tax SalesFrom EverandTax Sales for Rookies: A Beginner’s Guide to Understanding Property Tax SalesNo ratings yet

- Police Power Case DigestsDocument3 pagesPolice Power Case Digestsaphrodatee75% (4)

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Good Agriculture Practice (An Approach)Document28 pagesGood Agriculture Practice (An Approach)Robinson GultomNo ratings yet

- Customs Modernization and Tariff Act - Presentation by Atty Randy NagueDocument44 pagesCustoms Modernization and Tariff Act - Presentation by Atty Randy NaguePortCalls100% (9)

- Bookkeeping Course Syllabus - SDPDFDocument0 pagesBookkeeping Course Syllabus - SDPDFjasonmendez2010No ratings yet

- InvoiceDocument1 pageInvoiceJanhvii tiwariNo ratings yet

- Theories of Poverty and Community DevelopmentDocument13 pagesTheories of Poverty and Community DevelopmentOm Prakash100% (2)

- PSEG Sample Electric BillDocument4 pagesPSEG Sample Electric BilliFMi FOOTWEAR56% (16)

- (Tax 1) Midterms ReviewerDocument46 pages(Tax 1) Midterms ReviewerAiken Alagban LadinesNo ratings yet

- Commissioner of Internal Revenue vs. Algue IncDocument8 pagesCommissioner of Internal Revenue vs. Algue IncBesprenPaoloSpiritfmLucenaNo ratings yet

- Infrastructure Development Plan for Chhattisgarh - Road Project Viability OptionsDocument3 pagesInfrastructure Development Plan for Chhattisgarh - Road Project Viability Optionsjavedarzoo50% (2)

- Tax Case DigestDocument93 pagesTax Case DigestJuliet Julz Genita100% (1)

- 05 Victorias Milling Vs Municipality of VictorialDocument2 pages05 Victorias Milling Vs Municipality of VictorialJeanne CalalinNo ratings yet

- Municipal Board Upholds Tax on Vehicle SalesDocument133 pagesMunicipal Board Upholds Tax on Vehicle SalesAldrich AlmirezNo ratings yet

- Taxation 1 ReviewerDocument10 pagesTaxation 1 ReviewerRey ObnimagaNo ratings yet

- San Beda College of Law Case Digests in Taxation IDocument128 pagesSan Beda College of Law Case Digests in Taxation IAnne Lorraine DioknoNo ratings yet

- Commissioner of Internal Revenue vs. Hawaiian-Philippine Company G.R. No. L-16315Document7 pagesCommissioner of Internal Revenue vs. Hawaiian-Philippine Company G.R. No. L-16315Clark LimNo ratings yet

- Taxation 1 Case DigestDocument53 pagesTaxation 1 Case Digestamun dinNo ratings yet

- Local Government Taxation Powers and LimitationsDocument28 pagesLocal Government Taxation Powers and LimitationsFunnyPearl Adal GajuneraNo ratings yet

- Commissioner of Internal Revenue vs. Algue Inc. GR No. L-28896 - Feb. 17, 1988 FactsDocument9 pagesCommissioner of Internal Revenue vs. Algue Inc. GR No. L-28896 - Feb. 17, 1988 FactsPer PerNo ratings yet

- Tax Digest DukeDocument71 pagesTax Digest DukeDuke SucgangNo ratings yet

- Held:: of Makati vs. CA, G.R. Nos. 89898-99, October 1, 1990)Document5 pagesHeld:: of Makati vs. CA, G.R. Nos. 89898-99, October 1, 1990)charmagne cuevasNo ratings yet

- Tax DigestDocument25 pagesTax DigestAerwin AbesamisNo ratings yet

- Study Guide - Taxation CasesDocument3 pagesStudy Guide - Taxation CasesBabie Laarni Bagasina-MaribojocNo ratings yet

- TaxxxxDocument2 pagesTaxxxxRocel B. LigayaNo ratings yet

- Tax DigestsDocument16 pagesTax DigestsReina MarieNo ratings yet

- BUSTAXA ScheduleDocument6 pagesBUSTAXA ScheduleJohn MiguelNo ratings yet

- Philippine Taxation Cases SummarizedDocument30 pagesPhilippine Taxation Cases SummarizedLe Obm SizzlingNo ratings yet

- Philippine Airlines Tax Exemption Upheld in Landmark 1988 Supreme Court RulingDocument45 pagesPhilippine Airlines Tax Exemption Upheld in Landmark 1988 Supreme Court RulingPaulo SantosNo ratings yet

- Taxation LawDocument94 pagesTaxation LawspandanaNo ratings yet

- Villanueva V City of IloiloDocument48 pagesVillanueva V City of Iloiloamun dinNo ratings yet

- Own Reviewer 1 PDFDocument34 pagesOwn Reviewer 1 PDFChristineNo ratings yet

- General Principles On Taxation-2015Document40 pagesGeneral Principles On Taxation-2015Henry M. Macatuno Jr.No ratings yet

- Case Briefs on Taxation Powers of LGUsDocument3 pagesCase Briefs on Taxation Powers of LGUsEmmanuel ParagasNo ratings yet

- TAXATIONDocument18 pagesTAXATIONJiddery VilleNo ratings yet

- Tax 1 Midterms CasesDocument11 pagesTax 1 Midterms CasesJett LabillesNo ratings yet

- Issue: W/N The Collector of Internal RevenueDocument2 pagesIssue: W/N The Collector of Internal RevenueRalph Romeo BasconesNo ratings yet

- Taxation: Definition and Explanation Miss Rabia Asad Iqra University IslamabadDocument18 pagesTaxation: Definition and Explanation Miss Rabia Asad Iqra University IslamabadSaif Ur RehmanNo ratings yet

- Taxation: Basic Concepts and PrinciplesDocument47 pagesTaxation: Basic Concepts and PrinciplesMaybelleNo ratings yet

- CIR Vs Algue IncDocument2 pagesCIR Vs Algue IncQuoleteNo ratings yet

- Final Paper For TaxDocument43 pagesFinal Paper For TaxRaymond AlhambraNo ratings yet

- Taxation General PrinciplesDocument28 pagesTaxation General PrinciplesIzaNo ratings yet

- Chapter 2 Part 4 Income TaxDocument50 pagesChapter 2 Part 4 Income TaxGirlie Kaye Onongen PagtamaNo ratings yet

- Poli Rev Tax CasesDocument26 pagesPoli Rev Tax CasesBilton Cheng SyNo ratings yet

- CIR vs Cebu Portland Cement CompanyDocument14 pagesCIR vs Cebu Portland Cement CompanyJulian DubaNo ratings yet

- RA - PrE 418 - EXERCISE IIDocument3 pagesRA - PrE 418 - EXERCISE IIEnnajieee QtNo ratings yet

- CIR Disallowed 75K Deduction Claims by Private RespondentDocument2 pagesCIR Disallowed 75K Deduction Claims by Private RespondentMichael TampengcoNo ratings yet

- Taxation Cases 2Document16 pagesTaxation Cases 2Joji Marie PalecNo ratings yet

- Types of TaxesDocument58 pagesTypes of TaxesJuniorJayBNo ratings yet

- Tax Luna CasesDocument14 pagesTax Luna CasesIrish Bianca Usob LunaNo ratings yet

- General Principles of TaxationDocument2 pagesGeneral Principles of TaxationemgraceNo ratings yet

- Ge 2: Readings Philippine History: Colegio NG Lungsod NG BatangasDocument18 pagesGe 2: Readings Philippine History: Colegio NG Lungsod NG BatangasErica De CastroNo ratings yet

- Revenue Generation Program of Selected Local Government Units SAO Report No. 2009 04 Executive SummaryDocument6 pagesRevenue Generation Program of Selected Local Government Units SAO Report No. 2009 04 Executive SummaryRuelyn RosauroNo ratings yet

- Victorias Milling v. Municipality of VictoriaDocument12 pagesVictorias Milling v. Municipality of Victoriagemao.jb1986No ratings yet

- Taxation CasesDocument7 pagesTaxation Casesnicole coNo ratings yet

- Tax Review Cases SummaryDocument20 pagesTax Review Cases SummaryNeri DelfinNo ratings yet

- TAX 2 Feb 21 Incomplete CompilationDocument22 pagesTAX 2 Feb 21 Incomplete CompilationDaryl DumayasNo ratings yet

- Cbtax01 Chapter 9 (Activity)Document2 pagesCbtax01 Chapter 9 (Activity)Ariane CuayzonNo ratings yet

- Income Tax ActivityDocument7 pagesIncome Tax Activityenguitokarenjane708No ratings yet

- Institute-University School of Business Department of CommerceDocument21 pagesInstitute-University School of Business Department of Commercebhavu aryaNo ratings yet

- Tax Case DigestsDocument13 pagesTax Case DigestsArisa BajanaNo ratings yet

- Homeowner's Simple Guide to Property Tax Protest: Whats key: Exemptions & Deductions Blind. Disabled. Over 65. Property Rehabilitation. VeteransFrom EverandHomeowner's Simple Guide to Property Tax Protest: Whats key: Exemptions & Deductions Blind. Disabled. Over 65. Property Rehabilitation. VeteransNo ratings yet

- CASE DIGEST 1st Batch and 2nd BatchDocument21 pagesCASE DIGEST 1st Batch and 2nd BatchElla EspenesinNo ratings yet

- CD Asia Technologies, Inc.: Bookmarks My Queries History Back Search Help Log OutDocument34 pagesCD Asia Technologies, Inc.: Bookmarks My Queries History Back Search Help Log OutRegi PonferradaNo ratings yet

- TAX 42 - Exempt Sales GuideDocument10 pagesTAX 42 - Exempt Sales GuideEJ EduqueNo ratings yet

- Cancer PlanDocument10 pagesCancer PlanGURPREET SINGHNo ratings yet

- IT Card SaneepDocument4 pagesIT Card Saneephajabarala2008No ratings yet

- GSTR-2A Data Entry Instructions Worksheet Name GSTR-2A Table Reference Field NameDocument53 pagesGSTR-2A Data Entry Instructions Worksheet Name GSTR-2A Table Reference Field Namevishnu teja reddyNo ratings yet

- Indian Pharmaceutical Export IndustryDocument9 pagesIndian Pharmaceutical Export IndustrySumeet Shekhar NeerajNo ratings yet

- (Final) Financial Statement For Tax Return (03.03.2018)Document24 pages(Final) Financial Statement For Tax Return (03.03.2018)Engineering EntertainmentNo ratings yet

- Export Tax InvoiceDocument1 pageExport Tax InvoiceNavin RaviNo ratings yet

- HRCPC - LTC - LFC Reimbursement FormatDocument4 pagesHRCPC - LTC - LFC Reimbursement FormatAtul GuptaNo ratings yet

- Chandra Enterprises CRN-3Document1 pageChandra Enterprises CRN-3Aarvee FoodNo ratings yet

- GST May2023 V1Document213 pagesGST May2023 V1FhfhhNo ratings yet

- Using ReceivingDocument94 pagesUsing ReceivingPavlina StoqnovaNo ratings yet

- HD - RevisingDocument44 pagesHD - RevisingSon PhanNo ratings yet

- Analysing India'S Lability For A Framework in Trade: SUBMITTED TO MR - Animesh Das, Assistant ProfessorDocument19 pagesAnalysing India'S Lability For A Framework in Trade: SUBMITTED TO MR - Animesh Das, Assistant ProfessorVishwaja RaoNo ratings yet

- Philippines Sick ManDocument3 pagesPhilippines Sick ManMarielle Ansherine GuzmanNo ratings yet

- Andrew Bradley, Positive Rights, Negative Rights and Health CareDocument5 pagesAndrew Bradley, Positive Rights, Negative Rights and Health CareBonNo ratings yet

- Screenshot 2023-05-01 at 9.56.55 PMDocument2 pagesScreenshot 2023-05-01 at 9.56.55 PMketansanwalNo ratings yet

- Consensus Report 2-Page BriefDocument2 pagesConsensus Report 2-Page BriefchrsbakrNo ratings yet

- Lec 3 SalaryDocument28 pagesLec 3 SalaryManasi PatilNo ratings yet

- Manage Cash Flow & Optimize Business FinancesDocument125 pagesManage Cash Flow & Optimize Business FinancesJeam Endoma-ClzNo ratings yet

- Tax SparingDocument8 pagesTax SparingtaranNo ratings yet

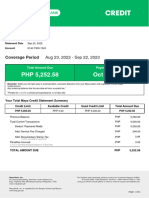

- MayaCredit SoA 2023SEPDocument3 pagesMayaCredit SoA 2023SEPjepoy palaruanNo ratings yet