You might also like

- Court of Tax Appeals: en BancDocument32 pagesCourt of Tax Appeals: en BancAemie JordanNo ratings yet

- Petitioner, 1169: Court of Tax AppealsDocument40 pagesPetitioner, 1169: Court of Tax Appealsgamingaccount10101No ratings yet

- Cta Eb CV 01386 D 2017mar21 Ass PDFDocument18 pagesCta Eb CV 01386 D 2017mar21 Ass PDFaudreydql5No ratings yet

- Republic of The Philippines: en BaneDocument30 pagesRepublic of The Philippines: en BaneKristine VillanuevaNo ratings yet

- Cta Eb CV 01498 D 2018may22 Ass PDFDocument30 pagesCta Eb CV 01498 D 2018may22 Ass PDFKhay-Ar PagdilaoNo ratings yet

- Cta Eb CV 01426 D 2018apr03 Ass PDFDocument26 pagesCta Eb CV 01426 D 2018apr03 Ass PDFYna YnaNo ratings yet

- Republic of The Philippines Court of Tax Appeals Quezon: PetitionerDocument45 pagesRepublic of The Philippines Court of Tax Appeals Quezon: PetitionerJay MirandaNo ratings yet

- Court of X Pea S: Ta Ap LDocument16 pagesCourt of X Pea S: Ta Ap LMa. Stephanie Kate LabroNo ratings yet

- Cta - Eb - CV - 01388 - D - 2017mar15 - Ass 2Document28 pagesCta - Eb - CV - 01388 - D - 2017mar15 - Ass 2Le SonneNo ratings yet

- Organizational Change v. CIRDocument16 pagesOrganizational Change v. CIRaudreydql5No ratings yet

- Cta Eb CV 01114 D 2015sep08 Ass PDFDocument17 pagesCta Eb CV 01114 D 2015sep08 Ass PDFHenson MontalvoNo ratings yet

- Republic of The Philippines Court of Tax Appeals Quezon CityDocument9 pagesRepublic of The Philippines Court of Tax Appeals Quezon CityLady Paul SyNo ratings yet

- Cta Eb CV 01322 D 2016oct17 AssDocument25 pagesCta Eb CV 01322 D 2016oct17 AssMarcy BaklushNo ratings yet

- Waterfront v. CIRDocument18 pagesWaterfront v. CIRaudreydql5No ratings yet

- First Division: Repubuc of The Philippines Court of Tax Appeals Quezon CityDocument14 pagesFirst Division: Repubuc of The Philippines Court of Tax Appeals Quezon CityYna YnaNo ratings yet

- Cta Eb CV 01424 D 2017aug17 AssDocument50 pagesCta Eb CV 01424 D 2017aug17 AssShwn Mchl SbynNo ratings yet

- Enbanc: Republic of The Philippines Court of Tax Appeals Quezon CityDocument14 pagesEnbanc: Republic of The Philippines Court of Tax Appeals Quezon CityHeartseed HazukiNo ratings yet

- Cta 2D CV 08551 M 2016mar02 AssDocument10 pagesCta 2D CV 08551 M 2016mar02 AssKathrine Chin LuNo ratings yet

- Cta Eb CV 01767 D 2019aug09 AssDocument18 pagesCta Eb CV 01767 D 2019aug09 AssChristel BravoNo ratings yet

- Cta 2D CV 08551 D 2015oct02 Ass PDFDocument37 pagesCta 2D CV 08551 D 2015oct02 Ass PDFMonica SorianoNo ratings yet

- Petitioner, Present: en BanDocument19 pagesPetitioner, Present: en BanMark EledaNo ratings yet

- Cta 1D CV 08820 D 2018jun21 AssDocument51 pagesCta 1D CV 08820 D 2018jun21 AssLarry Tobias Jr.No ratings yet

- CTA 8239 (AR Realty) - Excess Input Tax Carry-OverDocument53 pagesCTA 8239 (AR Realty) - Excess Input Tax Carry-OverJerwin DaveNo ratings yet

- Enban: Court of Ax AppealDocument16 pagesEnban: Court of Ax AppealRieland CuevasNo ratings yet

- Cta Eb CV 01338 D 2017jan11 AssDocument32 pagesCta Eb CV 01338 D 2017jan11 AssVince Llamazares LupangoNo ratings yet

- Cta Eb CV 01515 D 2018mar07 AssDocument20 pagesCta Eb CV 01515 D 2018mar07 AssMaryanne UnoNo ratings yet

- Commissioner of Internal Revenue v. GS GrainsDocument12 pagesCommissioner of Internal Revenue v. GS GrainsimianmoralesNo ratings yet

- Cta Eb CV 00988 M 2014dec16 Ref PDFDocument5 pagesCta Eb CV 00988 M 2014dec16 Ref PDFRobbie BañagaNo ratings yet

- Cta Eb CV 01686 D 2019mar25 AssDocument38 pagesCta Eb CV 01686 D 2019mar25 AssMosquite AquinoNo ratings yet

- Republic of The Philippines Court of Tax Appeals Quezon CityDocument38 pagesRepublic of The Philippines Court of Tax Appeals Quezon CityMosquite AquinoNo ratings yet

- Cta 2D CV 08179 D 2014may21 AssDocument37 pagesCta 2D CV 08179 D 2014may21 AssJanelle ZapataNo ratings yet

- Cta Eb CV 01280 D 2016oct03 Ass PDFDocument51 pagesCta Eb CV 01280 D 2016oct03 Ass PDFRic HardNo ratings yet

- Republic of The Philippines Quezon Ci1Y: Commissioner of Internal Revenue, Cta Eb Case No. 857Document13 pagesRepublic of The Philippines Quezon Ci1Y: Commissioner of Internal Revenue, Cta Eb Case No. 857Deloria DelsaNo ratings yet

- CIR v. SVI TechnologiesDocument23 pagesCIR v. SVI Technologiesaudreydql5No ratings yet

- Cta Eb CV 01569 D 2018jun07 AssDocument29 pagesCta Eb CV 01569 D 2018jun07 AssnorieNo ratings yet

- CTA Case No. 9074 - Subic Water vs. CIRDocument83 pagesCTA Case No. 9074 - Subic Water vs. CIRJeffrey JosolNo ratings yet

- Commissioner of Internal Revenue, INCORPORATED, RespondentDocument10 pagesCommissioner of Internal Revenue, INCORPORATED, RespondentRufino Gerard Moreno IIINo ratings yet

- Cta 2D CV 08872 M 2017jun07 AssDocument15 pagesCta 2D CV 08872 M 2017jun07 AssLarry Tobias Jr.No ratings yet

- CIR v. PAL, GR No180066Document12 pagesCIR v. PAL, GR No180066Rascille LaranasNo ratings yet

- Court of Tax Appeals: Travellers International Hotel Group, Inc., CTA Case No. 9168Document22 pagesCourt of Tax Appeals: Travellers International Hotel Group, Inc., CTA Case No. 9168Josef GutierrezNo ratings yet

- T Division: Republi The Philippines C AppealsDocument5 pagesT Division: Republi The Philippines C Appealsnia_artemis3414No ratings yet

- Northwind V Cir PDFDocument14 pagesNorthwind V Cir PDFJucca Noreen SalesNo ratings yet

- Cta Eb CV 01411 D 2017sep28 Ref PDFDocument21 pagesCta Eb CV 01411 D 2017sep28 Ref PDFpierremartinreyesNo ratings yet

- Bpi V Phil Am Life CtaDocument21 pagesBpi V Phil Am Life CtaEzer SccatsNo ratings yet

- Republic of The Philippines Court of Tax Appeals Quezon CityDocument21 pagesRepublic of The Philippines Court of Tax Appeals Quezon CityPaolaNo ratings yet

- Clark Water Corporation vs. BIR en BancDocument15 pagesClark Water Corporation vs. BIR en BancMarishiNo ratings yet

- First Division: Republic of The Philippines Court of Tax Appeals Quezon CityDocument36 pagesFirst Division: Republic of The Philippines Court of Tax Appeals Quezon CityYna YnaNo ratings yet

- En Banc: Republic of The Philippines Quezon CityDocument19 pagesEn Banc: Republic of The Philippines Quezon CityJonas CruzNo ratings yet

- CIR v. CarmonaDocument34 pagesCIR v. Carmonaaudreydql5No ratings yet

- Cta 3D CV 08091 D 2012oct23 AssDocument18 pagesCta 3D CV 08091 D 2012oct23 AssTin LicoNo ratings yet

- Etitioner,: Second DivisionDocument3 pagesEtitioner,: Second DivisionJudy RiveraNo ratings yet

- En Banc: Court of Tax AppealsDocument30 pagesEn Banc: Court of Tax Appealsmcguinto1No ratings yet

- First Division: Republic of The Philippines of Tax Appeals Quezon CityDocument16 pagesFirst Division: Republic of The Philippines of Tax Appeals Quezon CityfrancisNo ratings yet

- Cta Eb CV 02562 D 2023apr27 RefDocument20 pagesCta Eb CV 02562 D 2023apr27 RefFirenze PHNo ratings yet

- Republic of The Philippines Court of Tax Appeals Quezon CityDocument18 pagesRepublic of The Philippines Court of Tax Appeals Quezon CitykimNo ratings yet

- Cta Eb CV 02589 D 2023jul28 AssDocument28 pagesCta Eb CV 02589 D 2023jul28 AssVince Lupango (imistervince)No ratings yet

- Green Valley Marketing Corp. v. Commissioner of Internal Revenue, C.T.A. EB Case Nos. 1801 & 1808 (C.T.A. Case No. 8988), (October 14, 2019) PDFDocument22 pagesGreen Valley Marketing Corp. v. Commissioner of Internal Revenue, C.T.A. EB Case Nos. 1801 & 1808 (C.T.A. Case No. 8988), (October 14, 2019) PDFKriszan ManiponNo ratings yet

- Special Second Division: Republic of The Philippines Court of Tax Appeals Quezon CityDocument15 pagesSpecial Second Division: Republic of The Philippines Court of Tax Appeals Quezon CityhlcameroNo ratings yet

- CIR V PALDocument23 pagesCIR V PALCinNo ratings yet

- Abdullahi v. PfizerDocument41 pagesAbdullahi v. PfizerLarry Tobias Jr.No ratings yet

- LtvsvalenDocument3 pagesLtvsvalenManny DerainNo ratings yet

- Johnston v. Comp. Generale TransatlantiqueDocument3 pagesJohnston v. Comp. Generale TransatlantiqueLarry Tobias Jr.No ratings yet

- Enforcement of Foreign Judgments: Contributing EditorDocument9 pagesEnforcement of Foreign Judgments: Contributing EditorAprilleMaeKayeValentinNo ratings yet

- Abdullahi v. PfizerDocument41 pagesAbdullahi v. PfizerLarry Tobias Jr.No ratings yet

- Hilton v. GuyotDocument66 pagesHilton v. GuyotLarry Tobias Jr.No ratings yet

- 2016 ECP LectureDocument45 pages2016 ECP LectureMarlon LatNo ratings yet

- Public International Law ReviewerDocument39 pagesPublic International Law ReviewerAnthony Rupac Escasinas97% (75)

- Agcaoili LTD PDFDocument32 pagesAgcaoili LTD PDFruss8dikoNo ratings yet

- BIR Clarification On Senior Citizens DiscountDocument13 pagesBIR Clarification On Senior Citizens DiscountPaolo Antonio EscalonaNo ratings yet

- Supreme Court Case DigestDocument119 pagesSupreme Court Case DigestCon Pu50% (2)

- Revenue Memorandum Circular No.Document5 pagesRevenue Memorandum Circular No.Joel SyNo ratings yet

- Civ Pro Consi NotesDocument97 pagesCiv Pro Consi NotesChris Bonecile NadresNo ratings yet

- RR No. 22-2020 PDFDocument2 pagesRR No. 22-2020 PDFSandyNo ratings yet

- RR No. 13-2018 CorrectedDocument20 pagesRR No. 13-2018 CorrectedRap BaguioNo ratings yet

- Public Corporation: Atty. Mauricio UlepDocument90 pagesPublic Corporation: Atty. Mauricio UlepJamey SimpsonNo ratings yet

- Peza - RMC 74-99 PDFDocument4 pagesPeza - RMC 74-99 PDFRonnel TagalogonNo ratings yet

- Republic Act No. 11210 105-Day Expanded Maternity Leave Law: Frequently Asked Questions OnDocument6 pagesRepublic Act No. 11210 105-Day Expanded Maternity Leave Law: Frequently Asked Questions Onricardo revecheNo ratings yet

- 3a.epublit of Tbe Ftbtlippine $) Upreme Qtou RT: !ffilantlaDocument30 pages3a.epublit of Tbe Ftbtlippine $) Upreme Qtou RT: !ffilantlaValaris ColeNo ratings yet

- 230 Philippine Legal DoctrinesDocument24 pages230 Philippine Legal DoctrinesCindy BallesterosNo ratings yet

- Gti Ifrs Ias 12 Report UpdDocument52 pagesGti Ifrs Ias 12 Report UpdMallet S. GacadNo ratings yet

- Carbonell v. MetrobankDocument2 pagesCarbonell v. MetrobankLarry Tobias Jr.No ratings yet

- OHCHR BP Legal CapacityDocument20 pagesOHCHR BP Legal CapacityLarry Tobias Jr.No ratings yet

- Libro5 68Document30 pagesLibro5 68Larry Tobias Jr.No ratings yet

- 2016 ECP LectureDocument45 pages2016 ECP LectureMarlon LatNo ratings yet

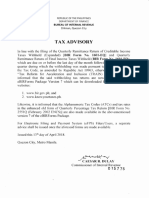

- Tax Advisory - BIR Form 1601EQ and FQDocument1 pageTax Advisory - BIR Form 1601EQ and FQLarry Tobias Jr.No ratings yet

- IRR-Data Privacy Act (Aug 25, 2016)Document49 pagesIRR-Data Privacy Act (Aug 25, 2016)BlogWatch100% (1)

- Manila Tax Code PDFDocument502 pagesManila Tax Code PDFJBBIllonesNo ratings yet

- CTA 8239 (AR Realty) - Excess Input Tax Carry-OverDocument53 pagesCTA 8239 (AR Realty) - Excess Input Tax Carry-OverJerwin DaveNo ratings yet

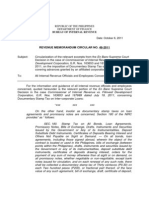

- Revenue Memorandum Circular No. 48-2011: Bureau of Internal RevenueDocument0 pagesRevenue Memorandum Circular No. 48-2011: Bureau of Internal RevenueEmil A. MolinaNo ratings yet

- Mission Statement: SBI Articulates Nine Core ValuesDocument6 pagesMission Statement: SBI Articulates Nine Core ValuesPaneer MomosNo ratings yet

- Coursera Branding and Customer ExperienceDocument1 pageCoursera Branding and Customer Experienceambuj joshiNo ratings yet

- !!!EVA 019 AtevaOverviewGradesSheet TS EN 0416 PDFDocument2 pages!!!EVA 019 AtevaOverviewGradesSheet TS EN 0416 PDFSlava75No ratings yet

- Treasurer'S Affidavit: Republic of The Philippines) City of Taguig) S.S. Metro Manila)Document2 pagesTreasurer'S Affidavit: Republic of The Philippines) City of Taguig) S.S. Metro Manila)Maria Andres50% (2)

- List of SAP Status CodesDocument19 pagesList of SAP Status Codesmajid D71% (7)

- VP Director Sales Pharmaceuticals in Philadelphia PA Resume James BruniDocument3 pagesVP Director Sales Pharmaceuticals in Philadelphia PA Resume James BruniJamesBruni10% (1)

- IDC IBM Honda Case Study May2017Document6 pagesIDC IBM Honda Case Study May2017Wanya Kumar (Ms.)No ratings yet

- From Good To Great: An Introduction To Servant Leadership Gemeco March 2018Document33 pagesFrom Good To Great: An Introduction To Servant Leadership Gemeco March 2018Papa KingNo ratings yet

- Tender Document Heliport ShimlaDocument128 pagesTender Document Heliport ShimlaAdarsh Kumar ManwalNo ratings yet

- Business Viability CalculatorDocument3 pagesBusiness Viability CalculatorKiyo AiNo ratings yet

- Training Levies: Rationale and Evidence From EvaluationsDocument17 pagesTraining Levies: Rationale and Evidence From EvaluationsGakuya KamboNo ratings yet

- Strategy Implementation - ClassDocument56 pagesStrategy Implementation - ClassM ManjunathNo ratings yet

- Evaluasi Kinerja Angkutan Umum Di Kota Magelang (Studi Kasus Jalur 1 Dan Jalur 8)Document10 pagesEvaluasi Kinerja Angkutan Umum Di Kota Magelang (Studi Kasus Jalur 1 Dan Jalur 8)Bahar FaizinNo ratings yet

- Exclusive Legislative ListDocument4 pagesExclusive Legislative ListLetsReclaim OurFutureNo ratings yet

- Mid Term Exam 1 - Fall 2018-799Document3 pagesMid Term Exam 1 - Fall 2018-799abdirahmanNo ratings yet

- Alliance Governance at Klarna: Managing and Controlling Risks of An Alliance PortfolioDocument9 pagesAlliance Governance at Klarna: Managing and Controlling Risks of An Alliance PortfolioAbhishek SinghNo ratings yet

- What Is The Importance of An Entrepreneurial MindDocument10 pagesWhat Is The Importance of An Entrepreneurial Mindlaarni joy conaderaNo ratings yet

- Test Bank For Financial Reporting and Analysis 13th Edition Charles H GibsonDocument36 pagesTest Bank For Financial Reporting and Analysis 13th Edition Charles H Gibsonbdelliumtiliairwoct100% (42)

- DhanVriddhi - 18-7-2023 8.8.55Document4 pagesDhanVriddhi - 18-7-2023 8.8.55Shreekant BhambareNo ratings yet

- TRDocument18 pagesTRharshal49No ratings yet

- CH 8Document64 pagesCH 8Anonymous 0cdKGOBBNo ratings yet

- CR 2015Document13 pagesCR 2015Agr AcabdiaNo ratings yet

- Configuring and Managing JDBC Data Sources For Oracle WebLogic Server 11.1Document148 pagesConfiguring and Managing JDBC Data Sources For Oracle WebLogic Server 11.1mdalaminNo ratings yet

- 4b18 PDFDocument5 pages4b18 PDFAnonymous lN5DHnehwNo ratings yet

- Construction Cost Handbook CNHK 2023Document63 pagesConstruction Cost Handbook CNHK 2023wlv hugoNo ratings yet

- Ker61035 Appd Case01Document3 pagesKer61035 Appd Case01GeeSungNo ratings yet

- Kotak Mahindra GroupDocument6 pagesKotak Mahindra GroupNitesh AswalNo ratings yet

- 5s Audit Check SheetDocument1 page5s Audit Check SheetDevendra Singh100% (1)

- Biz - Quatitative - Managment.Method Chapter.07Document27 pagesBiz - Quatitative - Managment.Method Chapter.07phannarithNo ratings yet

- Project ReportBanty Kumar VermaDocument126 pagesProject ReportBanty Kumar VermagunjanNo ratings yet

- Getting Through: Cold Calling Techniques To Get Your Foot In The DoorFrom EverandGetting Through: Cold Calling Techniques To Get Your Foot In The DoorRating: 4.5 out of 5 stars4.5/5 (63)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingFrom EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingRating: 4.5 out of 5 stars4.5/5 (97)

- Wall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementFrom EverandWall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementRating: 4.5 out of 5 stars4.5/5 (20)

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- The SHRM Essential Guide to Employment Law, Second Edition: A Handbook for HR Professionals, Managers, Businesses, and OrganizationsFrom EverandThe SHRM Essential Guide to Employment Law, Second Edition: A Handbook for HR Professionals, Managers, Businesses, and OrganizationsNo ratings yet

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorFrom EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorRating: 4.5 out of 5 stars4.5/5 (132)

- AI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersFrom EverandAI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersNo ratings yet

- Economics and the Law: From Posner to Postmodernism and Beyond - Second EditionFrom EverandEconomics and the Law: From Posner to Postmodernism and Beyond - Second EditionRating: 1 out of 5 stars1/5 (1)

- IFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SASFrom EverandIFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SASRating: 3 out of 5 stars3/5 (5)

- How to Win a Merchant Dispute or Fraudulent Chargeback CaseFrom EverandHow to Win a Merchant Dispute or Fraudulent Chargeback CaseNo ratings yet

- Disloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpFrom EverandDisloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpRating: 4 out of 5 stars4/5 (214)

- Learn the Essentials of Business Law in 15 DaysFrom EverandLearn the Essentials of Business Law in 15 DaysRating: 4 out of 5 stars4/5 (13)

- Indian Polity with Indian Constitution & Parliamentary AffairsFrom EverandIndian Polity with Indian Constitution & Parliamentary AffairsNo ratings yet

- How to Structure Your Business for Success: Choosing the Correct Legal Structure for Your BusinessFrom EverandHow to Structure Your Business for Success: Choosing the Correct Legal Structure for Your BusinessNo ratings yet

- Competition and Antitrust Law: A Very Short IntroductionFrom EverandCompetition and Antitrust Law: A Very Short IntroductionRating: 5 out of 5 stars5/5 (3)

- The Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesFrom EverandThe Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesRating: 5 out of 5 stars5/5 (1)

- LLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessFrom EverandLLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessRating: 5 out of 5 stars5/5 (1)

- Legal Guide for Starting & Running a Small BusinessFrom EverandLegal Guide for Starting & Running a Small BusinessRating: 4.5 out of 5 stars4.5/5 (9)

- Building Your Empire: Achieve Financial Freedom with Passive IncomeFrom EverandBuilding Your Empire: Achieve Financial Freedom with Passive IncomeNo ratings yet