You might also like

- Top 10 Lessons From 150 Trading BooksDocument16 pagesTop 10 Lessons From 150 Trading Bookskurwiszon100% (13)

- Grifols SA: Scranton and The Undisclosed DebtsDocument65 pagesGrifols SA: Scranton and The Undisclosed Debtsgothamcityresearch88% (25)

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Financial Statement Analysis - 10e by K. R. Am & John J. Wild Chapter01Document40 pagesFinancial Statement Analysis - 10e by K. R. Am & John J. Wild Chapter01Rifqi Ahmad Aula100% (2)

- Tucows Inc (TCX) - Cashing in On Neo-Nazis, Child Porn, & A Hidden Lawsuit As Insiders DumpDocument68 pagesTucows Inc (TCX) - Cashing in On Neo-Nazis, Child Porn, & A Hidden Lawsuit As Insiders DumpCopperfield_Research50% (12)

- Chapter 3 ProblemsDocument11 pagesChapter 3 Problemsahmed arfan100% (1)

- Business Valuation Methods and TechniquesDocument43 pagesBusiness Valuation Methods and TechniquesJunaid IqbalNo ratings yet

- Corporate Finance Ross 10th Edition Test BankDocument15 pagesCorporate Finance Ross 10th Edition Test Bankotoscopyforklesslx8v100% (29)

- Wayne Whaley - Planes, Trains and AutomobilesDocument16 pagesWayne Whaley - Planes, Trains and AutomobilesMacroCharts100% (2)

- Financial Performance Measures and Value Creation: the State of the ArtFrom EverandFinancial Performance Measures and Value Creation: the State of the ArtNo ratings yet

- Financial Statement Analysis: K R Subramanyam John J WildDocument40 pagesFinancial Statement Analysis: K R Subramanyam John J WildAgus TinaNo ratings yet

- Chapter 01Document36 pagesChapter 01vithyaNo ratings yet

- Financial Statement Analysis: K R Subramanyam John J WildDocument60 pagesFinancial Statement Analysis: K R Subramanyam John J WildEvan DanielNo ratings yet

- Chap 001Document50 pagesChap 001Loser NeetNo ratings yet

- Financial Statement Analysis: K R Subramanyam John J WildDocument40 pagesFinancial Statement Analysis: K R Subramanyam John J WildAftabKhanNo ratings yet

- Financial Statement Analysis: K R Subramanyam John J WildDocument40 pagesFinancial Statement Analysis: K R Subramanyam John J WildEmma SuryaniNo ratings yet

- Chapter 01 Overview of Financial Statement Analysis.Document40 pagesChapter 01 Overview of Financial Statement Analysis.audria_mh_110967519No ratings yet

- Financial Statement Analysis: K.R. SubramanyamDocument50 pagesFinancial Statement Analysis: K.R. SubramanyamDaveli NatanaelNo ratings yet

- Chapter 1 - BFMDocument60 pagesChapter 1 - BFMTricia Kate TungalaNo ratings yet

- IPPTChap001 ModifiedDocument48 pagesIPPTChap001 ModifiedLINH GIẢN PHƯƠNGNo ratings yet

- Financial Statement Analysis: K R SubramanyamDocument40 pagesFinancial Statement Analysis: K R SubramanyamElsye SinayNo ratings yet

- LU1 Overview of Financial Statement AnalysisDocument36 pagesLU1 Overview of Financial Statement AnalysisPriyah ThaiyalanNo ratings yet

- SW Chapter 1Document39 pagesSW Chapter 1fiqNo ratings yet

- Financial Statement Analysis: K.R. SubramanyamDocument49 pagesFinancial Statement Analysis: K.R. SubramanyamArinYuniastikaEkaPutriNo ratings yet

- 157 28235 EA419 2012 1 2 1 Chapter01Document40 pages157 28235 EA419 2012 1 2 1 Chapter01Ratri ParamitalaksmiNo ratings yet

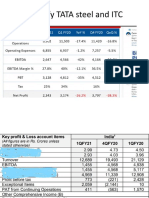

- Identify TATA steel and ITC through business analysisDocument37 pagesIdentify TATA steel and ITC through business analysisSakshi SharmaNo ratings yet

- 1 - Overview of Financial Statement AnalysisDocument40 pages1 - Overview of Financial Statement Analysisnovi afianingsihNo ratings yet

- Chapter 1 402 26Document44 pagesChapter 1 402 26boishakh38512No ratings yet

- Financial Statement Analysis: K R Subramanyam John J WildDocument40 pagesFinancial Statement Analysis: K R Subramanyam John J WildGustrilimandaNo ratings yet

- Financial Statement Analysis: K R Subramanyam John J WildDocument40 pagesFinancial Statement Analysis: K R Subramanyam John J WildSakshi SharmaNo ratings yet

- Financial Statement Analysis: K R Subramanyam John J WildDocument40 pagesFinancial Statement Analysis: K R Subramanyam John J WildSiap ManNo ratings yet

- Chapter 5Document39 pagesChapter 5trịnh thị quỳnhNo ratings yet

- CH 1Document40 pagesCH 1Theofanus Budya PrimasivaNo ratings yet

- Analisis Informasi KeuanganDocument40 pagesAnalisis Informasi KeuanganjosgarudaeagleNo ratings yet

- Overview of Financial Statement AnalysisDocument45 pagesOverview of Financial Statement Analysisshanky1124No ratings yet

- Financial Statement Analysis OverviewDocument45 pagesFinancial Statement Analysis OverviewAhmed ZaheerNo ratings yet

- Lec 1Document44 pagesLec 1Ahmad FauzanNo ratings yet

- FSA Fiches MidtermsDocument15 pagesFSA Fiches Midtermsimad imadNo ratings yet

- Financial Statements Analysis: Presented byDocument40 pagesFinancial Statements Analysis: Presented bykakolalamamaNo ratings yet

- Understanding Financial Statements for Equity and Credit AnalysisDocument43 pagesUnderstanding Financial Statements for Equity and Credit Analysisjason leeNo ratings yet

- Analysis of Financial Statements - Lecture 4Document15 pagesAnalysis of Financial Statements - Lecture 4Zahid Shahid SheikhaNo ratings yet

- Laporan Keuangan DAN Tujuan Analisis KeuanganDocument37 pagesLaporan Keuangan DAN Tujuan Analisis Keuanganrangga agungNo ratings yet

- Capitulo 1Document13 pagesCapitulo 1Sara CarvalhoNo ratings yet

- Analysis of Financial Statements: Analysts Are More Concerned About Future PerformanceDocument12 pagesAnalysis of Financial Statements: Analysts Are More Concerned About Future PerformanceintizarbukhariNo ratings yet

- Lecture Financial Statement Analysis 2Document36 pagesLecture Financial Statement Analysis 2Devyansh GuptaNo ratings yet

- AI - Materi 9 Analisis LK InternasDocument21 pagesAI - Materi 9 Analisis LK Internasbams_febNo ratings yet

- 1 Session - Overfiew of FSADocument45 pages1 Session - Overfiew of FSAAbhishek SwarnkarNo ratings yet

- Lecture 1 - Overview of FADocument17 pagesLecture 1 - Overview of FAJF FNo ratings yet

- FsaDocument53 pagesFsakweeNo ratings yet

- Chapter 9 - Prospective AnalysisDocument4 pagesChapter 9 - Prospective AnalysisjonaxxNo ratings yet

- Session 3&4 IA 2021Document93 pagesSession 3&4 IA 2021Ashley NguyenNo ratings yet

- Introduction To Financial AccountingDocument50 pagesIntroduction To Financial Accounting夏域No ratings yet

- FINC 3015 Financial ValuationsDocument14 pagesFINC 3015 Financial ValuationsParadoxicalNo ratings yet

- Financial Statement Anlaysis Ratio Analysis - Session 17 To 19Document49 pagesFinancial Statement Anlaysis Ratio Analysis - Session 17 To 19shvm.shkla96No ratings yet

- Ch01 Penman ModiDocument25 pagesCh01 Penman ModiFashion ThriftNo ratings yet

- The Use of Financial Ratios Analyzing Liquidity Analyzing Activity Analyzing Debt Analyzing Profitability A Complete Ratio AnalysisDocument19 pagesThe Use of Financial Ratios Analyzing Liquidity Analyzing Activity Analyzing Debt Analyzing Profitability A Complete Ratio Analysiskowsalya18No ratings yet

- BBA2K20: Principles of Business FinanceDocument18 pagesBBA2K20: Principles of Business FinanceMurtaza bhuttoNo ratings yet

- 2 - Engineering Economic Analysis: Construction Cost Analysis and Estimating (0401448)Document18 pages2 - Engineering Economic Analysis: Construction Cost Analysis and Estimating (0401448)danmsmith25No ratings yet

- Financial AnalysisDocument78 pagesFinancial AnalysisvithyaNo ratings yet

- Business Analysis and Valuation - Financial AnalysisDocument86 pagesBusiness Analysis and Valuation - Financial AnalysiscapassoaNo ratings yet

- Lesson 02 Financial AnalysisDocument8 pagesLesson 02 Financial AnalysisSVS ShanthaNo ratings yet

- Session 03Document30 pagesSession 03amanthi gunarathna95No ratings yet

- Week 2 FINA2207Document31 pagesWeek 2 FINA2207blythe shengNo ratings yet

- Portfolio TheoryDocument6 pagesPortfolio TheorykrgitNo ratings yet

- Revised Syllabus for Economics PapersDocument34 pagesRevised Syllabus for Economics PapersRUPESH SHIDNo ratings yet

- Derivatives Mishaps and What We Can Learn From Them: Big Losses by Financial InstitutionsDocument1 pageDerivatives Mishaps and What We Can Learn From Them: Big Losses by Financial InstitutionsUten nstNo ratings yet

- Case 06 Financial Detective 2016 F1763XDocument6 pagesCase 06 Financial Detective 2016 F1763XJosie KomiNo ratings yet

- Business Finance Module 5 StudentsDocument18 pagesBusiness Finance Module 5 StudentsOnly MeNo ratings yet

- Apznza 1Document27 pagesApznza 1jason manalotoNo ratings yet

- Accounting for Business Combinations Midterm Exam ReviewDocument4 pagesAccounting for Business Combinations Midterm Exam ReviewMica Ella San DiegoNo ratings yet

- Frequently Asked Questions On ASBADocument5 pagesFrequently Asked Questions On ASBAPratik BhadraNo ratings yet

- Changes in Equity, Cash Flows, NotesDocument3 pagesChanges in Equity, Cash Flows, NotesLucas BantilingNo ratings yet

- Ia 3 PrelimDocument12 pagesIa 3 PrelimshaylieeeNo ratings yet

- Dividends Company LawDocument18 pagesDividends Company LawKhizar Jamal SiddiquiNo ratings yet

- Compound Interest, Simple Interest, and Financial Concepts MCQDocument15 pagesCompound Interest, Simple Interest, and Financial Concepts MCQOlamilekan JuliusNo ratings yet

- AFR Final ExamDocument2 pagesAFR Final ExamSherif KhalifaNo ratings yet

- Split 162013 190909 - 20220331Document5 pagesSplit 162013 190909 - 20220331NUR FASIHAH BINTINo ratings yet

- FINANCIAL ACCOUNTING FUNDAMENTALSDocument3 pagesFINANCIAL ACCOUNTING FUNDAMENTALSQuy TranNo ratings yet

- A Broad Range of Opportunities Our Exchange Traded Funds (Etfs)Document12 pagesA Broad Range of Opportunities Our Exchange Traded Funds (Etfs)JNo ratings yet

- Introduction to Financial Management ConceptsDocument31 pagesIntroduction to Financial Management ConceptsDeepak Arthur Jacob100% (1)

- Cash ManagementDocument18 pagesCash ManagementbhargaviNo ratings yet

- ZEE Q4FY20 RESULT UPDATEDocument5 pagesZEE Q4FY20 RESULT UPDATEArpit JhanwarNo ratings yet

- Bca 302 Special Accounts Dec 1Document6 pagesBca 302 Special Accounts Dec 1omondifoe23No ratings yet

- Law & TaxDocument13 pagesLaw & TaxrylNo ratings yet

- Problem 3&5Document17 pagesProblem 3&5panda 1No ratings yet

- WC ExercisesDocument5 pagesWC ExercisesRaniel PamatmatNo ratings yet

- PGP IB Capital MarketsDocument20 pagesPGP IB Capital MarketsrahulnationaliteNo ratings yet