You might also like

- How to Create and Manage a Mutual Fund or Exchange-Traded Fund: A Professional's GuideFrom EverandHow to Create and Manage a Mutual Fund or Exchange-Traded Fund: A Professional's GuideNo ratings yet

- Understanding Investments: An Australian Investor's Guide to Stock Market, Property and Cash-Based InvestmentsFrom EverandUnderstanding Investments: An Australian Investor's Guide to Stock Market, Property and Cash-Based InvestmentsNo ratings yet

- Week 1FDocument23 pagesWeek 1FJessicaNo ratings yet

- Chap 004Document25 pagesChap 004K59 Le Nhat ThanhNo ratings yet

- Chap 004Document24 pagesChap 004Hiep LuuNo ratings yet

- CH - 04 Mutual Funds and Other Investment CompaniesDocument27 pagesCH - 04 Mutual Funds and Other Investment CompaniesshomudrokothaNo ratings yet

- FNCE4030 Fall 2014 ch01 02 Handout - 2 PDFDocument64 pagesFNCE4030 Fall 2014 ch01 02 Handout - 2 PDFabdul mateenNo ratings yet

- Chapter 001Document35 pagesChapter 001ruba.nour.33No ratings yet

- Mutual Funds and Other Investment Companies: Bodie, Kane and MarcusDocument20 pagesMutual Funds and Other Investment Companies: Bodie, Kane and MarcusMd TowkikNo ratings yet

- Investments Chapter4Document31 pagesInvestments Chapter4Siddharth KaushalNo ratings yet

- Capital Investments: Unicorn USD FTSE/JSE Listed PortfolioDocument1 pageCapital Investments: Unicorn USD FTSE/JSE Listed PortfoliodoogNo ratings yet

- Financial Management - I: Introduction ToDocument18 pagesFinancial Management - I: Introduction ToShivpratap SinghNo ratings yet

- Mutual Funds and Other Investment CompaniesDocument22 pagesMutual Funds and Other Investment CompaniesChao FengNo ratings yet

- What Is A Mutual Fund?Document45 pagesWhat Is A Mutual Fund?pinkukoolNo ratings yet

- Amfi PPT-1Document209 pagesAmfi PPT-1Nilesh TodarmalNo ratings yet

- Presented By: Swati JaiswalDocument18 pagesPresented By: Swati Jaiswaljaiswalswatin87No ratings yet

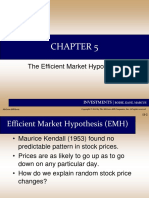

- Chap5 - The Efficient Market HypothesisDocument33 pagesChap5 - The Efficient Market HypothesisNgân HàNo ratings yet

- Investment Companies and Exchange-Traded FundsDocument11 pagesInvestment Companies and Exchange-Traded FundsJion DiazNo ratings yet

- AMFI Mutual Fund (Advisor) Module: Preparatory Training ProgramDocument231 pagesAMFI Mutual Fund (Advisor) Module: Preparatory Training Programallmutualfund100% (5)

- "It Is Not Wise To Put All Eggs Into One Basket": Was Probably in The Minds of Those WhoDocument34 pages"It Is Not Wise To Put All Eggs Into One Basket": Was Probably in The Minds of Those Whoprasannabb7452No ratings yet

- Mutual Fund: Prof. Shriram NerlekarDocument167 pagesMutual Fund: Prof. Shriram Nerlekarhimanshu sikarwarNo ratings yet

- Us The Bond Investor S Guide To EtfsDocument148 pagesUs The Bond Investor S Guide To EtfsmunnaiNo ratings yet

- Chap 004Document41 pagesChap 004Prem PrakashNo ratings yet

- Real Estate Mutual FundDocument13 pagesReal Estate Mutual Fundsonu238909No ratings yet

- Real Estate Mutual FundDocument13 pagesReal Estate Mutual Fundsonu238909No ratings yet

- Real Estate Mutual FundDocument13 pagesReal Estate Mutual Fundsonu238909No ratings yet

- Series-V-A: Mutual Fund Distributors Certification ExaminationDocument218 pagesSeries-V-A: Mutual Fund Distributors Certification ExaminationAjithreddy BasireddyNo ratings yet

- Understanding Portfolio Management of Investors Final Draft PDFDocument66 pagesUnderstanding Portfolio Management of Investors Final Draft PDFUrvashi VidhaniNo ratings yet

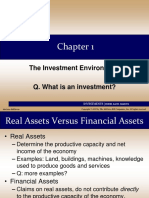

- The Investment Environment: InvestmentsDocument11 pagesThe Investment Environment: InvestmentsAtiqueSouravNo ratings yet

- Chap 001Document40 pagesChap 001AhmedNo ratings yet

- Financial Institutions, Markets, and Money, 9th Edition: Power Point Slides ForDocument39 pagesFinancial Institutions, Markets, and Money, 9th Edition: Power Point Slides Forahmed tahaNo ratings yet

- Chapter 1 The Investment EnvironmentDocument32 pagesChapter 1 The Investment EnvironmentNguyễn VânNo ratings yet

- Amfi PPTDocument203 pagesAmfi PPTmuskaan111No ratings yet

- Mutual FundsDocument37 pagesMutual FundsrmbowersNo ratings yet

- Mutual Funds: A Presentation by - Munish Sharma (Ca-Final)Document28 pagesMutual Funds: A Presentation by - Munish Sharma (Ca-Final)SANCHI610No ratings yet

- Guide To Privae Equity Fund of FundsDocument19 pagesGuide To Privae Equity Fund of FundslentinieNo ratings yet

- Investments CFADocument31 pagesInvestments CFAVasilIvanovNo ratings yet

- Fundamentals of Investments - Mutual FundsDocument36 pagesFundamentals of Investments - Mutual FundsE.r. RangarajaprasadNo ratings yet

- Chapter One: The Investment EnvironmentDocument30 pagesChapter One: The Investment Environmentkaylakshmi8314100% (1)

- 72712-29656-Mutual FundsDocument27 pages72712-29656-Mutual FundsAnkush JakkaNo ratings yet

- Is Used As A Generic Term For Various Types of Collective Investment Vehicles, Such AsDocument10 pagesIs Used As A Generic Term For Various Types of Collective Investment Vehicles, Such AsRaghavendra ChauhanNo ratings yet

- SapmDocument35 pagesSapmparag_85No ratings yet

- NJDocument186 pagesNJPurvi LimbasiaNo ratings yet

- A) What Is Mutual Fund?Document11 pagesA) What Is Mutual Fund?deyanimesh007No ratings yet

- Fidelity Real Estate Investment PortfolioDocument5 pagesFidelity Real Estate Investment PortfolioMaryna BolotskaNo ratings yet

- Mutual Fund WikipediaDocument12 pagesMutual Fund WikipediaDave ThreeTearsNo ratings yet

- Equity TradingDocument105 pagesEquity TradingMary Rose MoralesNo ratings yet

- Group 1 BDO MOTORTRADE TOYOTA 1Document63 pagesGroup 1 BDO MOTORTRADE TOYOTA 1Julla Agnes EscosioNo ratings yet

- Real Estate Investment Trusts (Reits)Document53 pagesReal Estate Investment Trusts (Reits)ElieNo ratings yet

- December 2020: Quarterly Commentary ReportDocument8 pagesDecember 2020: Quarterly Commentary ReportYog MehtaNo ratings yet

- A Presentation By: Joint Venture With Standard Life InvestmentsDocument156 pagesA Presentation By: Joint Venture With Standard Life InvestmentsaapkaskyNo ratings yet

- A Descriptive Study of Mutual Funds & Investors Perception About Investment in Mutual FundsDocument15 pagesA Descriptive Study of Mutual Funds & Investors Perception About Investment in Mutual FundssunilparmarNo ratings yet

- Fee Based Solutions: BMO Mutual Funds Series F and BMO Exchange Traded FundsDocument6 pagesFee Based Solutions: BMO Mutual Funds Series F and BMO Exchange Traded FundsSantiago Garcia PFP. MBA.No ratings yet

- 3 3MutualFundsDocument37 pages3 3MutualFundsSwathi SriNo ratings yet

- Aif Taxation Regulatory FlyerDocument6 pagesAif Taxation Regulatory FlyerAmit SharmaNo ratings yet

- The Mutual Fund Industry: Mingzhu WangDocument41 pagesThe Mutual Fund Industry: Mingzhu Wangcadeau01No ratings yet

- An easy approach to exchange traded funds: An introductory guide to ETFs and their investment and trading strategiesFrom EverandAn easy approach to exchange traded funds: An introductory guide to ETFs and their investment and trading strategiesRating: 3 out of 5 stars3/5 (2)

- Beyond the J Curve: Managing a Portfolio of Venture Capital and Private Equity FundsFrom EverandBeyond the J Curve: Managing a Portfolio of Venture Capital and Private Equity FundsNo ratings yet

- Common-Sense Investing: The Only Way to Guarantee Your Fair Share of Stock Market Return.From EverandCommon-Sense Investing: The Only Way to Guarantee Your Fair Share of Stock Market Return.No ratings yet

- Introduction+to+Game+Theory-assignment1+ 003Document2 pagesIntroduction+to+Game+Theory-assignment1+ 003abdul mateenNo ratings yet

- Urban Planning NotesDocument3 pagesUrban Planning Notesabdul mateenNo ratings yet

- Investments Return Short CutsDocument1 pageInvestments Return Short Cutsabdul mateenNo ratings yet

- Exercise 11 SolnDocument9 pagesExercise 11 Solnabdul mateenNo ratings yet

- Alternate InterventionDocument2 pagesAlternate Interventionabdul mateenNo ratings yet

- Math QuizDocument3 pagesMath Quizabdul mateenNo ratings yet

- Mathematics Problems With SolutionDocument3 pagesMathematics Problems With Solutionabdul mateenNo ratings yet

- Probablity Distribution SolutionDocument4 pagesProbablity Distribution Solutionabdul mateenNo ratings yet

- Exercise 1 Counting Soln 2Document7 pagesExercise 1 Counting Soln 2abdul mateenNo ratings yet

- Exercise 1 Counting Soln 2Document7 pagesExercise 1 Counting Soln 2abdul mateenNo ratings yet

- Lums WorksDocument2 pagesLums Worksabdul mateenNo ratings yet

- Probablity Distribution SolutionDocument4 pagesProbablity Distribution Solutionabdul mateenNo ratings yet

- Lums WorksDocument2 pagesLums Worksabdul mateenNo ratings yet

- Probablity Distribution SolutionDocument4 pagesProbablity Distribution Solutionabdul mateenNo ratings yet

- Sample Test Chap04Document9 pagesSample Test Chap04Niamul HasanNo ratings yet

- Cap 1Document74 pagesCap 1Mej Beit Chabab100% (1)

- Exercise 1 Counting Soln 2Document7 pagesExercise 1 Counting Soln 2abdul mateenNo ratings yet

- Maut Ki TayyariDocument81 pagesMaut Ki Tayyariabdul mateenNo ratings yet

- Maut Ka Manzar in Urdu PDFDocument119 pagesMaut Ka Manzar in Urdu PDFabdul mateenNo ratings yet

- FNCE4030 Fall 2014 ch05 Handout PDFDocument50 pagesFNCE4030 Fall 2014 ch05 Handout PDFabdul mateenNo ratings yet

- FNCE4030 Fall 2014 ch10 Handout PDFDocument22 pagesFNCE4030 Fall 2014 ch10 Handout PDFabdul mateenNo ratings yet

- FNCE4030 Fall 2014 ch15 Handout PDFDocument34 pagesFNCE4030 Fall 2014 ch15 Handout PDFabdul mateenNo ratings yet

- FNCE4030 Fall 2014 ch14 Handout PDFDocument37 pagesFNCE4030 Fall 2014 ch14 Handout PDFabdul mateenNo ratings yet

- FNCE4030 Fall 2014 ch12 Handout PDFDocument26 pagesFNCE4030 Fall 2014 ch12 Handout PDFabdul mateenNo ratings yet

- FNCE4030 Fall 2014 ch11 Handout PDFDocument45 pagesFNCE4030 Fall 2014 ch11 Handout PDFabdul mateenNo ratings yet

- FNCE4030 Fall 2014 ch07 Handout PDFDocument46 pagesFNCE4030 Fall 2014 ch07 Handout PDFabdul mateenNo ratings yet

- Aomq 3Document2 pagesAomq 3Dinesh SharmaNo ratings yet

- Betas 2017Document3 pagesBetas 2017Abraham Huachos GutierrezNo ratings yet

- Reliance Annual Repo PDFDocument463 pagesReliance Annual Repo PDFInfiniteNo ratings yet

- ABL DecDocument320 pagesABL DecGhulam HabibNo ratings yet

- Contoh Tesis Thesis BAB 1 - 5Document55 pagesContoh Tesis Thesis BAB 1 - 5Rolan Mart SasongkoNo ratings yet

- Centurion Bank of PunjabDocument7 pagesCenturion Bank of Punjabbaggamraasi1234No ratings yet

- Deepak Nitarte FY18Document216 pagesDeepak Nitarte FY18PRABHAT SHANKARNo ratings yet

- Data Science Banking and FintechDocument25 pagesData Science Banking and FintechBenoit Carrenand100% (2)

- Andreas, J.M., Rapp, M.S. Und M. Wolff (2010) "Determinants of Director Compensation in Two-Tier Systems Evidence From German Panel Data", Forthcoming in Review of Managerial ScienceDocument47 pagesAndreas, J.M., Rapp, M.S. Und M. Wolff (2010) "Determinants of Director Compensation in Two-Tier Systems Evidence From German Panel Data", Forthcoming in Review of Managerial Sciencemts_biniokNo ratings yet

- TESDA Online Program - Managing Your Personal FinancesDocument14 pagesTESDA Online Program - Managing Your Personal FinancesDinah Faye Redulla100% (3)

- QuestionsDocument10 pagesQuestionsLazy Panda100% (1)

- En 20120404Document24 pagesEn 20120404Hai Hoang ThanhNo ratings yet

- Enron ScandalDocument9 pagesEnron ScandalRohith MohanNo ratings yet

- NCFM ModulesDocument10 pagesNCFM ModulesMadhavi Reddy100% (1)

- Quantitative Methods in ProcurementDocument15 pagesQuantitative Methods in ProcurementPradeep KumarNo ratings yet

- FM Final ProjectDocument20 pagesFM Final ProjectNuman RoxNo ratings yet

- Blockbuster PDFDocument37 pagesBlockbuster PDFShinny HằngNo ratings yet

- Quiz 1 - Estate TaxDocument7 pagesQuiz 1 - Estate TaxKevin James Sedurifa Oledan100% (4)

- Thomas Bulkowski's Trading QuizDocument253 pagesThomas Bulkowski's Trading QuizBharath Raj Rathod100% (8)

- Accounting Theory - Chapter 10 Summary/NotesDocument7 pagesAccounting Theory - Chapter 10 Summary/NotesloveNo ratings yet

- Annex A. LTG FS 2013. NarraCapital FS 2012&2013 PDFDocument331 pagesAnnex A. LTG FS 2013. NarraCapital FS 2012&2013 PDFJohn Alfer Bag-oNo ratings yet

- Citigroup Credit Suisse J.P. Morgan Morgan Stanley Standard Chartered BankDocument5 pagesCitigroup Credit Suisse J.P. Morgan Morgan Stanley Standard Chartered BankhjsfdrNo ratings yet

- Bilal Ahmad 902344797Document87 pagesBilal Ahmad 902344797natasha_sethi_3No ratings yet

- Security Analysis and Portfolio Management: Question BankDocument12 pagesSecurity Analysis and Portfolio Management: Question BankgiteshNo ratings yet

- JLL ONPOINT Flanders Officemarket Report Q1 2017Document20 pagesJLL ONPOINT Flanders Officemarket Report Q1 2017Wim VandenbosscheNo ratings yet

- Foreign Direct Investment: Johanna C. Claro-Pichay, RCH Mpa 2Document21 pagesForeign Direct Investment: Johanna C. Claro-Pichay, RCH Mpa 2Tristan Lindsey Kaamiño AresNo ratings yet

- Project Intake FormDocument6 pagesProject Intake Formjamespeterson02No ratings yet

- Case Study - Linear Tech - Christopher Taylor - SampleDocument9 pagesCase Study - Linear Tech - Christopher Taylor - Sampleakshay87kumar8193No ratings yet

- Global Annual Review 2009 PWCDocument62 pagesGlobal Annual Review 2009 PWCDeepesh SinghNo ratings yet