You might also like

- Private Equity Portfolio OverviewDocument21 pagesPrivate Equity Portfolio OverviewRavi Chaurasia100% (4)

- RJR Case StudyDocument5 pagesRJR Case StudyFelipe Kasai MarcosNo ratings yet

- FINA 652 Private Equity: Class I Introduction To The Private Equity IndustryDocument51 pagesFINA 652 Private Equity: Class I Introduction To The Private Equity IndustryАнди А. СаэзNo ratings yet

- Valuation AnalysisDocument86 pagesValuation Analysisollllllllllo100% (1)

- WSO Private Equity Prep Package PDFDocument242 pagesWSO Private Equity Prep Package PDFBill Lee100% (2)

- KKR Overview and Organizational SummaryDocument73 pagesKKR Overview and Organizational SummaryRavi Chaurasia100% (3)

- Private Equity PDFDocument44 pagesPrivate Equity PDFOkba DjabbarNo ratings yet

- RJR NabiscoDocument22 pagesRJR Nabiscokriteesinha100% (2)

- Nike CaseDocument7 pagesNike CaseNindy Darista100% (1)

- Roll-Up: The Past, Present, and Future of Utilities ConsolidationFrom EverandRoll-Up: The Past, Present, and Future of Utilities ConsolidationNo ratings yet

- Case Assignment - RJR NabiscoDocument1 pageCase Assignment - RJR NabiscoMuhammad Rehan NasirNo ratings yet

- RJR Nabisco Case - Group 4 - PPTDocument8 pagesRJR Nabisco Case - Group 4 - PPTMeghna Saluja100% (1)

- Case Nike Cost of Capital - FinalDocument7 pagesCase Nike Cost of Capital - FinalNick ChongsanguanNo ratings yet

- RJR - NabiscoDocument37 pagesRJR - NabiscoAB100% (1)

- RJRDocument4 pagesRJRliyulongNo ratings yet

- Turnaround President COO CEO in USA Resume Gregory BuckleyDocument3 pagesTurnaround President COO CEO in USA Resume Gregory BuckleyGregoryBuckley100% (1)

- Asset Management OverviewDocument51 pagesAsset Management OverviewRavi Chaurasia100% (1)

- 24 RJR Nabisco - A Case Study of Complex Leveraged Buyout - Financial Analyst's JournalDocument14 pages24 RJR Nabisco - A Case Study of Complex Leveraged Buyout - Financial Analyst's JournalJoel DiasNo ratings yet

- RJR Nabisco 1Document6 pagesRJR Nabisco 1gopal mundhraNo ratings yet

- Berkshire - IntroDocument2 pagesBerkshire - IntroRohith ThatchanNo ratings yet

- Case Nike - Cost of Capital Fix 1Document9 pagesCase Nike - Cost of Capital Fix 1Yousania RatuNo ratings yet

- RJR NabiscoDocument17 pagesRJR Nabiscodanielcid100% (1)

- Technical Note On LBO Valuation and Modeling - 150309 - 4!10!2015 - SAMPLEDocument30 pagesTechnical Note On LBO Valuation and Modeling - 150309 - 4!10!2015 - SAMPLEJayant Sharma100% (1)

- Capstone Overview 2012Document24 pagesCapstone Overview 2012Ravi Chaurasia100% (1)

- International Investments in Private Equity: Asset Allocation, Markets, and Industry StructureFrom EverandInternational Investments in Private Equity: Asset Allocation, Markets, and Industry StructureNo ratings yet

- RJR Nabisco ValuationDocument7 pagesRJR Nabisco ValuationAnil Kotaga0% (1)

- RJR Nabisco - SpreadsheetDocument10 pagesRJR Nabisco - SpreadsheetSurajNo ratings yet

- H. J. Heinz M&A: Case SynopsisDocument8 pagesH. J. Heinz M&A: Case SynopsisTanya Raj100% (1)

- Southland Case StudyDocument7 pagesSouthland Case StudyRama Renspandy100% (2)

- RJR Nabisco ValuationDocument40 pagesRJR Nabisco ValuationEdisonCaguanaNo ratings yet

- RJR Nabisco ValuationDocument33 pagesRJR Nabisco ValuationShivani Bhatia100% (4)

- Plunder Private Equitys Plan To Pillage America 9781541702127 9781541702103Document371 pagesPlunder Private Equitys Plan To Pillage America 9781541702127 9781541702103sir loinNo ratings yet

- RJRJRJJRJRJRJJR111111Document4 pagesRJRJRJJRJRJRJJR111111John Paul Chua57% (7)

- RJRJRJJRJRJRJJR111111Document4 pagesRJRJRJJRJRJRJJR111111John Paul Chua57% (7)

- Beyond the Deal: A Revolutionary Framework for Successful Mergers & Acquisitions That Achieve Breakthrough Performance GainsFrom EverandBeyond the Deal: A Revolutionary Framework for Successful Mergers & Acquisitions That Achieve Breakthrough Performance GainsNo ratings yet

- Syndicate 6 - Gainesboro Machine Tools CorporationDocument12 pagesSyndicate 6 - Gainesboro Machine Tools CorporationSimon ErickNo ratings yet

- Midland Energy Resources Case Study: FINS3625-Applied Corporate FinanceDocument11 pagesMidland Energy Resources Case Study: FINS3625-Applied Corporate FinanceCourse Hero100% (1)

- Nike Cost of CapitalDocument23 pagesNike Cost of CapitalSaahil Ledwani100% (1)

- RJR Nabisco ValuationDocument38 pagesRJR Nabisco ValuationJCNo ratings yet

- Case Study: Hill Country Snack Foods " HCSF " (With Soluion )Document12 pagesCase Study: Hill Country Snack Foods " HCSF " (With Soluion )Kamran Shabbir50% (2)

- Corporate Finance - Hill Country Snack FoodDocument11 pagesCorporate Finance - Hill Country Snack FoodNell MizunoNo ratings yet

- Executive Decision Making at General MotorsDocument14 pagesExecutive Decision Making at General MotorsGourav Guha100% (2)

- The Art of M&A Integration 2nd Ed: A Guide to Merging Resources, Processes,and ResponsibiltiesFrom EverandThe Art of M&A Integration 2nd Ed: A Guide to Merging Resources, Processes,and ResponsibiltiesNo ratings yet

- Submitted To: Submitted By: Dr. Kulbir Singh Vinay Singh 201922106 Aurva Bhardwaj 201922066 Deepanshu Gupta 201922069 Sameer Kumbhalwar 201922097Document3 pagesSubmitted To: Submitted By: Dr. Kulbir Singh Vinay Singh 201922106 Aurva Bhardwaj 201922066 Deepanshu Gupta 201922069 Sameer Kumbhalwar 201922097Aurva BhardwajNo ratings yet

- LBO DELL Presentation Case StudyDocument20 pagesLBO DELL Presentation Case StudyJoseph TanNo ratings yet

- Cases RJR Nabisco 90 & 91 - Assignment QuestionsDocument1 pageCases RJR Nabisco 90 & 91 - Assignment QuestionsBrunoPereiraNo ratings yet

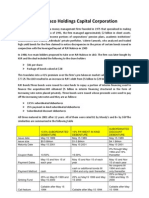

- The Relative Pricing of High-Yield Debt: The Case of RJR Nabisco Holdings Capital CorporationDocument24 pagesThe Relative Pricing of High-Yield Debt: The Case of RJR Nabisco Holdings Capital CorporationAhsen Ali Siddiqui100% (1)

- Nabisco - Sol v0.1 PDFDocument13 pagesNabisco - Sol v0.1 PDFMohit Khandelwal100% (1)

- COVID-19 R M&A TransactionsDocument3 pagesCOVID-19 R M&A TransactionsrdiazeplaNo ratings yet

- Summit Partners 2011Document20 pagesSummit Partners 2011Colin MisteleNo ratings yet

- RJR 1987 Annual ReportDocument94 pagesRJR 1987 Annual Reportmilken466100% (1)

- RJR Case StudyDocument14 pagesRJR Case StudyNazir Ahmad BahariNo ratings yet

- Calculating The NPV of The AcquisitionDocument23 pagesCalculating The NPV of The Acquisitionkooldude1989100% (1)

- Seagate Veritas Summary 021501Document4 pagesSeagate Veritas Summary 021501satheesh21090% (1)

- Leveraged BuyoutDocument9 pagesLeveraged Buyoutbharat100% (1)

- Revco LboDocument44 pagesRevco LboharshalNo ratings yet

- RJR Nabisco ValuationDocument33 pagesRJR Nabisco ValuationKrishna Chaitanya KothapalliNo ratings yet

- Case 2 Corporate FinanceDocument5 pagesCase 2 Corporate FinancePaula GarciaNo ratings yet

- Gainesboro Machine ToolsDocument2 pagesGainesboro Machine ToolsedselNo ratings yet

- Case 3: Rockboro Machine Tools Corporation Executive SummaryDocument1 pageCase 3: Rockboro Machine Tools Corporation Executive SummaryMaricel GuarinoNo ratings yet

- In-Class Project 2: Due 4/13/2019 Your Name: Valuation of The Leveraged Buyout (LBO) of RJR Nabisco 1. Cash Flow EstimatesDocument5 pagesIn-Class Project 2: Due 4/13/2019 Your Name: Valuation of The Leveraged Buyout (LBO) of RJR Nabisco 1. Cash Flow EstimatesDinhkhanh NguyenNo ratings yet

- RJR Nabisco Holdings Capital CorporationDocument3 pagesRJR Nabisco Holdings Capital CorporationManogana RasaNo ratings yet

- General Mills' PaperDocument9 pagesGeneral Mills' PaperSarah McDermottNo ratings yet

- 2 Yeats Valve and Controls Case 1Document16 pages2 Yeats Valve and Controls Case 1Yuki JameloNo ratings yet

- Effet de LevierDocument17 pagesEffet de Leviergeorges khairallahNo ratings yet

- Christopher Seifert's Portfolio ProjectDocument4 pagesChristopher Seifert's Portfolio ProjectChris SeifertNo ratings yet

- Private Equity JargonDocument14 pagesPrivate Equity JargonWilling ZvirevoNo ratings yet

- Kaye Scholer M&A Survey 2008 From Flash Drive ProvidedDocument72 pagesKaye Scholer M&A Survey 2008 From Flash Drive ProvidedJack DenverNo ratings yet

- Private Credit in Asia PacificDocument22 pagesPrivate Credit in Asia PacifictamlqNo ratings yet

- Year Market Winner Wwbid Wwqty Lfwbid Lfwqty Lfcbid LfcqtyDocument72 pagesYear Market Winner Wwbid Wwqty Lfwbid Lfwqty Lfcbid LfcqtyQuỳnh Anh NguyễnNo ratings yet

- Vietnam QXDDocument5 pagesVietnam QXDAn Hoang Le100% (1)

- Ipo A Global Guide, Expanded - (Part 1 Defining The Parameters)Document62 pagesIpo A Global Guide, Expanded - (Part 1 Defining The Parameters)taha zamzamNo ratings yet

- Private Equity Firm KKR, Appoints Shusaku Minoda To Chairman, Hirofumi Hirano Joins As CEODocument6 pagesPrivate Equity Firm KKR, Appoints Shusaku Minoda To Chairman, Hirofumi Hirano Joins As CEOAlex HoltNo ratings yet

- Nabisco CaseDocument3 pagesNabisco CaseVictorNo ratings yet

- Appendix - III Main Examination - HindiDocument54 pagesAppendix - III Main Examination - HindiDevrajNo ratings yet

- CPPIB Credit Investments Inc. Joins KKR and Stone Point Capital As A Partner in Capital Markets Platform: Press ReleaseDocument6 pagesCPPIB Credit Investments Inc. Joins KKR and Stone Point Capital As A Partner in Capital Markets Platform: Press ReleaseDevon JohnsonNo ratings yet

- Private Equity HistoryDocument3 pagesPrivate Equity HistorynbaffourNo ratings yet

- Kaizen MF VCF Updates 09 09Document62 pagesKaizen MF VCF Updates 09 09Sanjay KumarNo ratings yet

- CB Insights Global Unicorn Club 2019Document20 pagesCB Insights Global Unicorn Club 2019Yash Joglekar0% (1)

- Causes and Consequences of LBODocument25 pagesCauses and Consequences of LBODead EyeNo ratings yet

- Date Target Company Name Parent Deal Type Buyer (S) Seller (S) Deal Value ($ MN) % Sought Sector Sub IndustryDocument1 pageDate Target Company Name Parent Deal Type Buyer (S) Seller (S) Deal Value ($ MN) % Sought Sector Sub Industrysaahil kinkhabwalaNo ratings yet

- GHMH 101Document20 pagesGHMH 101dheeraj choudharyNo ratings yet

- BMO Bible 2013Document430 pagesBMO Bible 2013Matthew GoldsteinNo ratings yet

- Academy Sports + OutdoorsDocument19 pagesAcademy Sports + Outdoorsakr200714No ratings yet

- Matthias Knecht (Auth.) - Diversification, Industry Dynamism, and Economic Performance - The Impact of Dynamic-Related Diversification On The Multi-Business Firm-Gabler Verlag (2014)Document365 pagesMatthias Knecht (Auth.) - Diversification, Industry Dynamism, and Economic Performance - The Impact of Dynamic-Related Diversification On The Multi-Business Firm-Gabler Verlag (2014)Akbar LuckyNo ratings yet

- Primer On Private EquityDocument19 pagesPrimer On Private Equityhttp://besthedgefund.blogspot.comNo ratings yet

- Ken Mehlman - Private Equity - Kinder and GentlerDocument4 pagesKen Mehlman - Private Equity - Kinder and GentlerAlyson DavisNo ratings yet