You might also like

- Section A - ALL 15 Questions Are Compulsory and MUST Be AttemptedDocument17 pagesSection A - ALL 15 Questions Are Compulsory and MUST Be AttemptedAdnan SiddiquiNo ratings yet

- A) Project ADocument9 pagesA) Project AАнастасия ОсипкинаNo ratings yet

- Chapter 8Document71 pagesChapter 8MAN HIN NGAI100% (2)

- F2 Acca Mock ExamDocument4 pagesF2 Acca Mock Examsiksha0% (1)

- Capital Project AccountingDocument2 pagesCapital Project AccountingDhaval GandhiNo ratings yet

- Exam Questions and AnswersDocument18 pagesExam Questions and AnswersAna Aliyah Angin100% (1)

- Quiz 3.1 BudgetingDocument6 pagesQuiz 3.1 BudgetingMaxine ConstantinoNo ratings yet

- F2 Mock Questions 201603Document12 pagesF2 Mock Questions 201603Renato WilsonNo ratings yet

- Product Life CycleDocument19 pagesProduct Life CycleTamana Gupta100% (2)

- Chapter 14-Ch. 14-Cash Flow Estimation 11-13.El-Bigbee Bottling CompanyDocument1 pageChapter 14-Ch. 14-Cash Flow Estimation 11-13.El-Bigbee Bottling CompanyRajib DahalNo ratings yet

- The Cross-Price Elasticity of Demand For The Two Is CalculatedDocument3 pagesThe Cross-Price Elasticity of Demand For The Two Is CalculatedhaNo ratings yet

- Chap 2Document47 pagesChap 2ADITYA JAIN100% (1)

- caCAF 01 Suggested Solution Autumn 2014Document8 pagescaCAF 01 Suggested Solution Autumn 2014shahroozkhanNo ratings yet

- Practice Exam 1gdfgdfDocument49 pagesPractice Exam 1gdfgdfredearth2929100% (1)

- F2 6 Dec 2002 AnsDocument9 pagesF2 6 Dec 2002 Ansapi-26257228No ratings yet

- AccountingDocument7 pagesAccountingHà PhươngNo ratings yet

- Taxation of CompaniesDocument10 pagesTaxation of CompaniesnikhilramaneNo ratings yet

- Breakeven QuestionDocument14 pagesBreakeven QuestionALI HAMEED0% (1)

- 6int 2006 Dec QDocument9 pages6int 2006 Dec Qrizwan789No ratings yet

- Chapter 3 - Utility Theory: ST Petersburg ParadoxDocument77 pagesChapter 3 - Utility Theory: ST Petersburg Paradoxabc123No ratings yet

- F5-07 Risk and UncertaintyDocument26 pagesF5-07 Risk and UncertaintyIsavic AlsinaNo ratings yet

- CH 12 Irrecoverable Debts and Allowance v3Document8 pagesCH 12 Irrecoverable Debts and Allowance v3BuntheaNo ratings yet

- Tuition Mock D11 - F7 Questions FinalDocument11 pagesTuition Mock D11 - F7 Questions FinalRenato WilsonNo ratings yet

- CAT T10 - 2010 - Dec - ADocument9 pagesCAT T10 - 2010 - Dec - AHussain MeskinzadaNo ratings yet

- Orchid LimitedDocument3 pagesOrchid LimitedANo ratings yet

- Matrix: Md. Aktar Kamal Assistant Professor of Management FBS, BupDocument71 pagesMatrix: Md. Aktar Kamal Assistant Professor of Management FBS, BupSadia Afrin Arin50% (2)

- Chapter 4Document17 pagesChapter 4RBNo ratings yet

- Revision 2 - Investment AppraisalDocument27 pagesRevision 2 - Investment AppraisalVishal PrasadNo ratings yet

- Question-Ias 2 - Ias 16 and Ias 40 - Admin-2019-2020-1Document6 pagesQuestion-Ias 2 - Ias 16 and Ias 40 - Admin-2019-2020-1Letsah BrightNo ratings yet

- ACCA F2 Revision Notes OpenTuition PDFDocument25 pagesACCA F2 Revision Notes OpenTuition PDFSaurabh KaushikNo ratings yet

- F2 Past Paper - Ans12-2004Document10 pagesF2 Past Paper - Ans12-2004ArsalanACCANo ratings yet

- Master Budget Assignment CH 9Document4 pagesMaster Budget Assignment CH 9api-240741436No ratings yet

- Pacilio Securtiy Service Accounting EquationDocument11 pagesPacilio Securtiy Service Accounting EquationKailash KumarNo ratings yet

- Financial AccountingDocument9 pagesFinancial AccountingAnonymous VmhXGNlFyNo ratings yet

- Quiz 5Document8 pagesQuiz 5Putin Phy0% (1)

- Adams Inc Acquires Clay Corporation On January 1 2012 inDocument1 pageAdams Inc Acquires Clay Corporation On January 1 2012 inMiroslav GegoskiNo ratings yet

- KisikisiDocument7 pagesKisikisijalunasaNo ratings yet

- F2 Past Paper - Ans06-2004Document10 pagesF2 Past Paper - Ans06-2004ArsalanACCANo ratings yet

- F 2Document6 pagesF 2Nasir Iqbal100% (1)

- CH 4Document6 pagesCH 4Jean ValderramaNo ratings yet

- 05 DEC AnswersDocument15 pages05 DEC Answerskhengmai100% (5)

- Financial Accounting Question SetDocument24 pagesFinancial Accounting Question SetAlireza KafaeiNo ratings yet

- ACCA F3-FFA Revision Mock - Answers D15Document12 pagesACCA F3-FFA Revision Mock - Answers D15Kiri chrisNo ratings yet

- Dipifr Int 2010 Dec A PDFDocument11 pagesDipifr Int 2010 Dec A PDFPiyal HossainNo ratings yet

- Skans School of Accoutancy Subject Ma1 Test Teacher Shahab Name Batch Obtained Marks Total Marks 30Document4 pagesSkans School of Accoutancy Subject Ma1 Test Teacher Shahab Name Batch Obtained Marks Total Marks 30shahabNo ratings yet

- June 1, 2007 June 30, 2007Document2 pagesJune 1, 2007 June 30, 2007አረጋዊ ሐይለማርያምNo ratings yet

- IAS-37 Provisions, Contingent Liabilities and Contingent AssetsDocument3 pagesIAS-37 Provisions, Contingent Liabilities and Contingent AssetsAbdul SamiNo ratings yet

- 3 9 PDFDocument4 pages3 9 PDFHassan TariqNo ratings yet

- ManufacturingDocument6 pagesManufacturingapi-3034896990% (1)

- IPRO Mock Exam - 2021 - QDocument21 pagesIPRO Mock Exam - 2021 - QKevin Ch Li100% (1)

- Bca 423-Marginal Vs Absoption Costing.Document8 pagesBca 423-Marginal Vs Absoption Costing.James GathaiyaNo ratings yet

- 02 MA2 LRP QuestionsDocument36 pages02 MA2 LRP QuestionsKopanang Leokana50% (2)

- F2 Past Paper - Question06-2002Document8 pagesF2 Past Paper - Question06-2002ArsalanACCANo ratings yet

- 7Document101 pages7Navindra JaggernauthNo ratings yet

- Practice Questions - Ratio AnalysisDocument2 pagesPractice Questions - Ratio Analysissaltee100% (5)

- Exercises FS AnalysisDocument24 pagesExercises FS AnalysisEuniceNo ratings yet

- Paper T10 Managing Finances: Sample Multiple Choice Questions - June 2009Document174 pagesPaper T10 Managing Finances: Sample Multiple Choice Questions - June 2009Khánh LyNo ratings yet

- ACCA F2 AC N MCDocument10 pagesACCA F2 AC N MCSamuel DwumfourNo ratings yet

- IAS 02: Inventories: Requirement: SolutionDocument2 pagesIAS 02: Inventories: Requirement: SolutionMD Hafizul Islam Hafiz100% (1)

- Chapter Two: Master Budget and Responsibility AccountingDocument25 pagesChapter Two: Master Budget and Responsibility Accountingweyn deguNo ratings yet

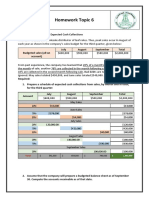

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- Ex and P-BudgetingDocument10 pagesEx and P-BudgetingJessa Swing Dela CruzNo ratings yet

- Barwani PDFDocument13 pagesBarwani PDFvishvarNo ratings yet

- CH 12Document27 pagesCH 12DewiRatihYunusNo ratings yet

- 2.strategic IntentDocument23 pages2.strategic IntentAnish ThomasNo ratings yet

- Project Budget WBSDocument4 pagesProject Budget WBSpooliglotaNo ratings yet

- Cash Budget Model Cash Budget Model - Case Study: InflowsDocument1 pageCash Budget Model Cash Budget Model - Case Study: Inflowsayu nailil kiromahNo ratings yet

- B1342 SavantICDocument3 pagesB1342 SavantICSveto SlNo ratings yet

- mgm3180 1328088793Document12 pagesmgm3180 1328088793epymaliNo ratings yet

- Fashion and StatusDocument11 pagesFashion and StatusDiana ScoriciNo ratings yet

- Ficci Ey M and e Report 2019 Era of Consumer Art PDFDocument309 pagesFicci Ey M and e Report 2019 Era of Consumer Art PDFAbhishek VyasNo ratings yet

- Annual Report of Bajaj Finance NBFC PDFDocument308 pagesAnnual Report of Bajaj Finance NBFC PDFAnand bhangariya100% (1)

- R WaseemDocument3 pagesR WaseemWaseem RajaNo ratings yet

- 8C PDFDocument16 pages8C PDFReinaNo ratings yet

- INterviewsDocument3 pagesINterviewsJanina SerranoNo ratings yet

- Ivy LeagueDocument2 pagesIvy LeagueDr Amit RangnekarNo ratings yet

- 3 Sem EcoDocument10 pages3 Sem EcoKushagra SrivastavaNo ratings yet

- Hazardous Consignment Note BlankDocument3 pagesHazardous Consignment Note BlankChristopher HenryNo ratings yet

- COMP2230 Introduction To Algorithmics: A/Prof Ljiljana BrankovicDocument18 pagesCOMP2230 Introduction To Algorithmics: A/Prof Ljiljana BrankovicMrZaggyNo ratings yet

- TFG Manuel Feito Dominguez 2015Document117 pagesTFG Manuel Feito Dominguez 2015Yenisel AguilarNo ratings yet

- Accounting For Income Tax-NotesDocument4 pagesAccounting For Income Tax-NotesMaureen Derial PantaNo ratings yet

- Dolly Madison Zingers (Devil's Food)Document2 pagesDolly Madison Zingers (Devil's Food)StuffNo ratings yet

- HZL 4100070676 Inv Pay Slip PDFDocument12 pagesHZL 4100070676 Inv Pay Slip PDFRakshit KeswaniNo ratings yet

- ELS4 Examples From Oys YdsDocument1 pageELS4 Examples From Oys YdsKranting TangNo ratings yet

- Cows and ChickensDocument9 pagesCows and Chickensapi-298565250No ratings yet

- Continue or Eliminate AnalysisDocument3 pagesContinue or Eliminate AnalysisMaryNo ratings yet

- Reverse Pricing ProcedureDocument4 pagesReverse Pricing ProcedureAnonymous 13sDEcwShTNo ratings yet

- (84650977) Variance Accounting Case Study - PD1Document24 pages(84650977) Variance Accounting Case Study - PD1Mukesh ManwaniNo ratings yet

- FRBM Act: The Fiscal Responsibility and Budget Management ActDocument12 pagesFRBM Act: The Fiscal Responsibility and Budget Management ActNaveen DsouzaNo ratings yet

- 18e Key Question Answers CH 4Document2 pages18e Key Question Answers CH 4AbdullahMughal100% (1)