You might also like

- ACLU Public Records Act Request To UC PoliceDocument4 pagesACLU Public Records Act Request To UC PoliceChris NewfieldNo ratings yet

- Letter of 36 Senior Executives On Removing Pension CapDocument13 pagesLetter of 36 Senior Executives On Removing Pension CapChris NewfieldNo ratings yet

- Senate To Yudof On Protests and Police 112011Document2 pagesSenate To Yudof On Protests and Police 112011Chris NewfieldNo ratings yet

- Academic Senate Budget Overview: Presented To The Regents May 17, 2007Document16 pagesAcademic Senate Budget Overview: Presented To The Regents May 17, 2007Chris NewfieldNo ratings yet

- CUCFA To Yudof Tuition HikeDocument4 pagesCUCFA To Yudof Tuition HikeChris NewfieldNo ratings yet

- The End of The Public and The Rise of The SubDocument6 pagesThe End of The Public and The Rise of The Subapi-39024083No ratings yet

- Chalfant and Henry PEB Op-EdDocument3 pagesChalfant and Henry PEB Op-EdChris NewfieldNo ratings yet

- Strategically Dynamic BlumDocument7 pagesStrategically Dynamic BlumChris NewfieldNo ratings yet

- Promoting UC Education 1Document1 pagePromoting UC Education 1Chris NewfieldNo ratings yet

- BudgetTransparency Proj UCSDDocument12 pagesBudgetTransparency Proj UCSDChris NewfieldNo ratings yet

- Senate Resolution On BudgetDocument1 pageSenate Resolution On BudgetChris NewfieldNo ratings yet

- Pages From 2009-12-07 Letter To University of California System-1Document5 pagesPages From 2009-12-07 Letter To University of California System-1api-26051999No ratings yet

- LakoffFacultyLetterEB CL FinalDocument3 pagesLakoffFacultyLetterEB CL FinalChris NewfieldNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Collective Bargaining Agreement PDFDocument4 pagesThe Collective Bargaining Agreement PDFChristine Joy DechavezNo ratings yet

- Nishat Mills Final HRM ProjectDocument32 pagesNishat Mills Final HRM ProjectMuhammad Tariq64% (11)

- Director: University Legal Counsel Office/ Legal Services DivisionDocument3 pagesDirector: University Legal Counsel Office/ Legal Services DivisionZeddy65No ratings yet

- Performance AppraisalDocument17 pagesPerformance AppraisalgddemosNo ratings yet

- Various HR Policies of Maruti Suzuki India LimitedDocument24 pagesVarious HR Policies of Maruti Suzuki India LimitedChirag AgarwalNo ratings yet

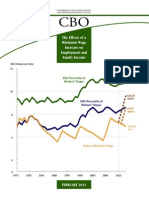

- The Effects of A Minimum-Wage Increase On Employment and Family IncomeDocument43 pagesThe Effects of A Minimum-Wage Increase On Employment and Family IncomeJeffrey DunetzNo ratings yet

- Competency Assessment-SupervisorDocument1 pageCompetency Assessment-SupervisorShailendra Sanap100% (1)

- Descriptive Review SampleDocument5 pagesDescriptive Review Sampleviveksonalgupta67% (3)

- Dual Career PathDocument11 pagesDual Career PathRashi Yadav100% (2)

- Walmart AnswersDocument5 pagesWalmart AnswersAhamed Najeeb Rahman0% (2)

- Emp Welfare EssayDocument7 pagesEmp Welfare Essaypeter_railviharNo ratings yet

- 8.work EnvironmentDocument69 pages8.work EnvironmentRodrigo Eberhart Musaio SommaNo ratings yet

- Self Performance EvaluationDocument2 pagesSelf Performance Evaluationhosny1234No ratings yet

- Janiqua Cobb: Work ExperienceDocument3 pagesJaniqua Cobb: Work ExperienceFranny CobbNo ratings yet

- Questionnaire of Measuring Employee Satisfaction at Bengal Group of IndustriesDocument2 pagesQuestionnaire of Measuring Employee Satisfaction at Bengal Group of IndustriesMuktadirhasanNo ratings yet

- Annexure - I QuestionnaireDocument16 pagesAnnexure - I QuestionnaireTanmay JagetiaNo ratings yet

- Industrialattachmentofnazbangladeshltd 140515042508 Phpapp02Document198 pagesIndustrialattachmentofnazbangladeshltd 140515042508 Phpapp02Ripon SayanNo ratings yet

- Chapter - 1 Introduction and Design of The StudyDocument9 pagesChapter - 1 Introduction and Design of The StudykalyanNo ratings yet

- The Expatriate IHRMDocument2 pagesThe Expatriate IHRMHK MahmudNo ratings yet

- Case Study 1Document3 pagesCase Study 1Tanveer Ameen LashariNo ratings yet

- My Hotel 19.10.22Document1 pageMy Hotel 19.10.22Corina PaiereleNo ratings yet

- Edu 3083Document16 pagesEdu 3083Shalini KanganNo ratings yet

- Chief HR Officer in South Florida Resume Corey HellerDocument2 pagesChief HR Officer in South Florida Resume Corey HellerCorey HellerNo ratings yet

- Chapter 10Document35 pagesChapter 10Canwal RazaNo ratings yet

- Service Sector Struggles Organizing Wal-Mart in QuebecDocument6 pagesService Sector Struggles Organizing Wal-Mart in QuebecAnonymous p9q6TshNo ratings yet

- Workplace Discrimination Consequences in Bangladesh - Zafreen Zaara - PHI401Document2 pagesWorkplace Discrimination Consequences in Bangladesh - Zafreen Zaara - PHI401AbuSalehMuhammadSaimonNo ratings yet

- Narrative ReportsDocument3 pagesNarrative Reportsapi-272329834No ratings yet

- LeadingDocument2 pagesLeading蒲俊雄No ratings yet

- Status Change FormDocument1 pageStatus Change FormComsale HRNo ratings yet

- HR Director Manager Benefits in Indianapolis IN Resume Diana Briggs-PopeDocument2 pagesHR Director Manager Benefits in Indianapolis IN Resume Diana Briggs-PopeDianaBriggsPopeNo ratings yet