You might also like

- Imbong V Ochoa DigestDocument9 pagesImbong V Ochoa DigestJaerelle HernandezNo ratings yet

- Topacio v. Ong DigestDocument2 pagesTopacio v. Ong DigestJaerelle HernandezNo ratings yet

- 07 Arigo V Swift Dela CruzDocument5 pages07 Arigo V Swift Dela CruzJaerelle HernandezNo ratings yet

- Abakada vs. Executive SecretaryDocument309 pagesAbakada vs. Executive SecretaryJaerelle HernandezNo ratings yet

- Gios-Samar, Inc. v. DOTC-DigestDocument4 pagesGios-Samar, Inc. v. DOTC-DigestJaerelle Hernandez100% (3)

- Imbong V Ochoa DigestDocument9 pagesImbong V Ochoa DigestJaerelle HernandezNo ratings yet

- Soriano vs. Sec of FinDocument84 pagesSoriano vs. Sec of FinJaerelle HernandezNo ratings yet

- Supreme Court Dismisses Petition Against Proposed Bills Abolishing Judiciary Development FundDocument2 pagesSupreme Court Dismisses Petition Against Proposed Bills Abolishing Judiciary Development FundJaerelle HernandezNo ratings yet

- Ople vs. TorresDocument60 pagesOple vs. TorresJaerelle HernandezNo ratings yet

- Magallona v. Ermita (Sample)Document3 pagesMagallona v. Ermita (Sample)Jaerelle HernandezNo ratings yet

- Court Locator PDFDocument327 pagesCourt Locator PDFJaerelle HernandezNo ratings yet

- Ang Nars Vs Executive SecretaryDocument43 pagesAng Nars Vs Executive SecretaryJaerelle Hernandez100% (1)

- 134 - Fores v. MirandaDocument3 pages134 - Fores v. MirandaJaerelle HernandezNo ratings yet

- Sen. Lopez v. Pan Am World Airways: SC rules on moral damages in airline breach of contract caseDocument4 pagesSen. Lopez v. Pan Am World Airways: SC rules on moral damages in airline breach of contract caseJaerelle HernandezNo ratings yet

- 4 Remedies of The AccusedDocument1 page4 Remedies of The AccusedJaerelle HernandezNo ratings yet

- 108 - Sps. Belen V Hon. ChavezDocument3 pages108 - Sps. Belen V Hon. ChavezJaerelle HernandezNo ratings yet

- 01 Manliclic vs. CalaunanDocument25 pages01 Manliclic vs. CalaunanJaerelle HernandezNo ratings yet

- 135 - Air France V CarrascosoDocument3 pages135 - Air France V CarrascosoJaerelle HernandezNo ratings yet

- First Day DigestsDocument58 pagesFirst Day DigestsJaerelle HernandezNo ratings yet

- EJERCITO V. Sandiganbayan PDFDocument3 pagesEJERCITO V. Sandiganbayan PDFJaerelle HernandezNo ratings yet

- Tsai v. CADocument11 pagesTsai v. CAJaerelle HernandezNo ratings yet

- Philip Morris vs CA ruling affirms foreign corporations' right to sue for trademark infringementDocument5 pagesPhilip Morris vs CA ruling affirms foreign corporations' right to sue for trademark infringementJaerelle Hernandez100% (1)

- MHP Garments, Inc. vs. Court of Appeals, 236 SCRA 227, September 02, 1994Document14 pagesMHP Garments, Inc. vs. Court of Appeals, 236 SCRA 227, September 02, 1994KPPNo ratings yet

- 026 - Francia v. IACDocument1 page026 - Francia v. IACJaerelle HernandezNo ratings yet

- Rosario Textile Mills v Home Bankers Savings and Trust CoDocument2 pagesRosario Textile Mills v Home Bankers Savings and Trust CoNylaNo ratings yet

- Pci Leasing V TrojanDocument3 pagesPci Leasing V TrojanJaerelle HernandezNo ratings yet

- Rosario Textile Mills V Home Bankers Savings and Trust Company GDocument3 pagesRosario Textile Mills V Home Bankers Savings and Trust Company GJaerelle HernandezNo ratings yet

- 034 Roman Catholic Bishop of Jaro v. Dela PeñaDocument1 page034 Roman Catholic Bishop of Jaro v. Dela PeñaJaerelle HernandezNo ratings yet

- 091 - People's Bank & Trust Co. V Dahican LumberDocument2 pages091 - People's Bank & Trust Co. V Dahican LumberJaerelle HernandezNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- VAT Return 2015 SAP LibraryDocument17 pagesVAT Return 2015 SAP LibraryTatyana KosarevaNo ratings yet

- CBexam Mockexam Draft01Document5 pagesCBexam Mockexam Draft01Mark Lord Morales BumagatNo ratings yet

- Settlement QuoteDocument1 pageSettlement QuotehowzellaNo ratings yet

- Ra 10963 RRD PDFDocument54 pagesRa 10963 RRD PDFMeAnn TumbagaNo ratings yet

- CIR v. Isabela Cultural Corp GR No. 17223, 12 Feb 2007Document5 pagesCIR v. Isabela Cultural Corp GR No. 17223, 12 Feb 2007Marge OstanNo ratings yet

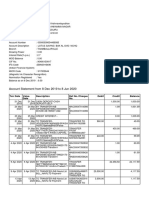

- Account Statement From 8 Dec 2019 To 8 Jun 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument6 pagesAccount Statement From 8 Dec 2019 To 8 Jun 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceMUTHYALA NEERAJANo ratings yet

- Account Statement From 1 Dec 2021 To 8 Jul 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument15 pagesAccount Statement From 1 Dec 2021 To 8 Jul 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceVIVEK CHAUHANNo ratings yet

- Configuration of SAP Special GLDocument20 pagesConfiguration of SAP Special GLAtulWalvekar100% (3)

- Tax - Sababan's NotesDocument120 pagesTax - Sababan's NotesfranceheartNo ratings yet

- Army Welfare Housing Organisation (Awho) Kashmir House, Rajaji Marg, New Delhi - 110011 WebsiteDocument4 pagesArmy Welfare Housing Organisation (Awho) Kashmir House, Rajaji Marg, New Delhi - 110011 Websitesaurabhkr1989No ratings yet

- 2022 Proof of PaymentDocument4 pages2022 Proof of PaymentCollen LihakaNo ratings yet

- Thq002-Inst. Sales PDFDocument2 pagesThq002-Inst. Sales PDFAndrea AtendidoNo ratings yet

- Tax1. Cases. 1. A. Definition, Concept and Purpose of Taxation - B. Nature and Characteristics of TaxationDocument37 pagesTax1. Cases. 1. A. Definition, Concept and Purpose of Taxation - B. Nature and Characteristics of TaxationLecdiee Nhojiezz Tacissea SalnackyiNo ratings yet

- RCO Commentary Finance Bill 2023-24Document26 pagesRCO Commentary Finance Bill 2023-24drtunioNo ratings yet

- M PassbookDocument4 pagesM Passbookirfan shaikhNo ratings yet

- T6 Employment Part 1 2016 StudentDocument2 pagesT6 Employment Part 1 2016 StudentVeenesha MuralidharanNo ratings yet

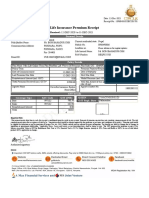

- Life Insurance Premium Receipt: Personal DetailsDocument1 pageLife Insurance Premium Receipt: Personal Detailschanam bedantaNo ratings yet

- F2 Individual Trainee Application Form Version 14 September 2023Document2 pagesF2 Individual Trainee Application Form Version 14 September 2023qa-qcNo ratings yet

- Constitutional Framework of GST in IndiaDocument20 pagesConstitutional Framework of GST in IndiaABNo ratings yet

- iCPA Practice Challenge Community Hi jbpedragosa23! 0 ePoints Log OutDocument15 pagesiCPA Practice Challenge Community Hi jbpedragosa23! 0 ePoints Log OutJericho PedragosaNo ratings yet

- Digital Banking PPT PresentationDocument16 pagesDigital Banking PPT PresentationSufyan ShaikhNo ratings yet

- This Study Resource Was: SolutionsDocument3 pagesThis Study Resource Was: SolutionsCzarwin William PobleteNo ratings yet

- TMT Quote 08.05.2023Document1 pageTMT Quote 08.05.2023sathya narayanaNo ratings yet

- DILG Memo Circular 2012531 Bd8bbf3770Document36 pagesDILG Memo Circular 2012531 Bd8bbf3770Jaja Ordinario Quiachon-AbarcaNo ratings yet

- Gyaan All in OneDocument41 pagesGyaan All in OneHEMANT SARVANKARNo ratings yet

- Income Tax Dissertation TopicsDocument5 pagesIncome Tax Dissertation TopicsDoMyPapersLowell100% (1)

- Bajaj Capital LimitedDocument1 pageBajaj Capital LimitedSunny JohnsonNo ratings yet

- Tax On IndividualsDocument9 pagesTax On IndividualsshakiraNo ratings yet

- 2306 Manila WaterDocument6 pages2306 Manila WaterRegina Raymundo AlbayNo ratings yet

- RTMF 990Document49 pagesRTMF 990Craig MaugerNo ratings yet