You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Computer Worm: Transactions On Dependable and Secure ComputingDocument2 pagesComputer Worm: Transactions On Dependable and Secure ComputingSherleen Anne Agtina DamianNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Board Resolution For Signing of MoU With NAPOCOR 9.25.02 AMDocument2 pagesBoard Resolution For Signing of MoU With NAPOCOR 9.25.02 AMSherleen Anne Agtina DamianNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Dissociative Identity DisorderDocument1 pageDissociative Identity DisorderSherleen Anne Agtina DamianNo ratings yet

- Block Screening GuidelinesDocument4 pagesBlock Screening GuidelinesSherleen Anne Agtina DamianNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Pale Digest: Cayetano VS. MonsodDocument26 pagesPale Digest: Cayetano VS. MonsodSherleen Anne Agtina DamianNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Law Schools U.S. Law Schools: General RequirementsDocument7 pagesLaw Schools U.S. Law Schools: General RequirementsSherleen Anne Agtina DamianNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Quasha Ancheta Peña v. LCN Construction CorporationDocument25 pagesQuasha Ancheta Peña v. LCN Construction CorporationSherleen Anne Agtina DamianNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- COMMISSIONER OF INTERNAL REVENUE VsDocument13 pagesCOMMISSIONER OF INTERNAL REVENUE VsSherleen Anne Agtina DamianNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Placido C. Ramos and Augusto L. RAMOS, Petitioners, vs. Pepsi-Cola Bottling Co. of The P.I. and ANDRES BONIFACIO, RespondentsDocument10 pagesPlacido C. Ramos and Augusto L. RAMOS, Petitioners, vs. Pepsi-Cola Bottling Co. of The P.I. and ANDRES BONIFACIO, RespondentsSherleen Anne Agtina DamianNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Corpo Digest 34-36Document6 pagesCorpo Digest 34-36Sherleen Anne Agtina DamianNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- CAsesDocument4 pagesCAsesSherleen Anne Agtina DamianNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- DRAFTTHHHDocument17 pagesDRAFTTHHHSherleen Anne Agtina DamianNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Digest EVIDDocument11 pagesDigest EVIDSherleen Anne Agtina DamianNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Agency 2Document19 pagesAgency 2Sherleen Anne Agtina DamianNo ratings yet

- Ñasque Filed A Complaint For Payment of Sum of Money and Damages Against RespondentsDocument9 pagesÑasque Filed A Complaint For Payment of Sum of Money and Damages Against RespondentsSherleen Anne Agtina DamianNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Tax Reviewer Constitutional Limitations (Dual-Pi Vet-F E RNS-J)Document11 pagesTax Reviewer Constitutional Limitations (Dual-Pi Vet-F E RNS-J)Sherleen Anne Agtina DamianNo ratings yet

- Demand and Support, Competitor AnalysisDocument116 pagesDemand and Support, Competitor AnalysisSherleen Anne Agtina DamianNo ratings yet

- GST Configuration in SAP FICODocument5 pagesGST Configuration in SAP FICOKingpinNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Sap SD Sales or To PaymentDocument21 pagesSap SD Sales or To PaymentKrishna MoorthyNo ratings yet

- Oracle Apps Order Management Interview QuestionsDocument9 pagesOracle Apps Order Management Interview Questionsnet6351100% (2)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- British Steel Sections Price ListDocument6 pagesBritish Steel Sections Price Listrezetane mohamed amineNo ratings yet

- Inventory Trading SampleDocument28 pagesInventory Trading SampleRonald Victor Galarza Hermitaño0% (1)

- CA Pragya Singh Rajpurohit: Documents List - BasicDocument30 pagesCA Pragya Singh Rajpurohit: Documents List - BasicsankNo ratings yet

- Attachment 1Document1 pageAttachment 1Akhmed TemaevNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Qbo 2018 TBDocument20 pagesQbo 2018 TBWilson CarlosNo ratings yet

- 2.order To Cash Sell From Stock en in P BPPDocument28 pages2.order To Cash Sell From Stock en in P BPPPrashant SinghNo ratings yet

- Candor Kolkata One Hi-Tech Structures Private LimitedDocument4 pagesCandor Kolkata One Hi-Tech Structures Private LimitedSurgicals GamingNo ratings yet

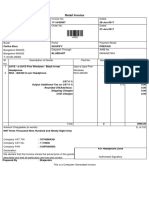

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Sourav SamaddarNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Acer Market Monitoring Report 2015Document329 pagesAcer Market Monitoring Report 2015MihaiAdiNo ratings yet

- Perform Customer and Product Profitability AnalysisDocument25 pagesPerform Customer and Product Profitability Analysisrahul_agrawal165No ratings yet

- ERP S4HANA1809 DeltaScope FINAL PartnerVersionDocument311 pagesERP S4HANA1809 DeltaScope FINAL PartnerVersionJohan GarciaNo ratings yet

- Kukil DasDocument1 pageKukil DasRajib DasNo ratings yet

- Customs ValuationDocument22 pagesCustoms ValuationRochelle Ann SamsonNo ratings yet

- 1Document2 pages1lrbbNo ratings yet

- IcpDocument15 pagesIcpOng Yang LimNo ratings yet

- RTO ProcessDocument5 pagesRTO Processashutosh mauryaNo ratings yet

- Vendor Selection ControlsDocument40 pagesVendor Selection ControlsLiew Chee KiongNo ratings yet

- Kwarsick Invoices Jan-Feb 2011Document2 pagesKwarsick Invoices Jan-Feb 2011southwhidbeyNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Invoice of 44500Document1 pageInvoice of 44500Partho BoraNo ratings yet

- Example Sales Contract 14Document10 pagesExample Sales Contract 14hinhkuteNo ratings yet

- Approval of Non-Pressure Paraffin Stoves & Heaters - CMMDocument43 pagesApproval of Non-Pressure Paraffin Stoves & Heaters - CMM胡大威No ratings yet

- Conference Organizers' Manual: How To Successfully Plan Your EventDocument36 pagesConference Organizers' Manual: How To Successfully Plan Your EventAIBPM CommitteeNo ratings yet

- Henry CVDocument6 pagesHenry CVSTRAHAN-HughesNo ratings yet

- SAP SD Certifications Questions and AnswersDocument22 pagesSAP SD Certifications Questions and Answerspradeep75% (4)

- Scenariu de Logistica in SAPDocument36 pagesScenariu de Logistica in SAPAdilé-Elena NemoianuNo ratings yet

- Purchase Requisition Policies & Procedures: Title: ScopeDocument4 pagesPurchase Requisition Policies & Procedures: Title: Scopeadil100% (1)

- Bộ Câu Hỏi Ts410Document22 pagesBộ Câu Hỏi Ts410Việt Nguyễn QuốcNo ratings yet