You might also like

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- W-8BEN-E: Certificate of Status of Beneficial Owner For United States Tax Withholding and Reporting (Entities)Document2 pagesW-8BEN-E: Certificate of Status of Beneficial Owner For United States Tax Withholding and Reporting (Entities)GYM VIỆT OfficialNo ratings yet

- Fw8eci PDFDocument1 pageFw8eci PDFAnonymous qaI31HNo ratings yet

- W 8benDocument1 pageW 8benantonio tovarNo ratings yet

- Form W-8 BEN-E DefaultDocument2 pagesForm W-8 BEN-E DefaultJack RaynoldNo ratings yet

- Tax W8 BENsDocument3 pagesTax W8 BENsroman tamayo Jr.No ratings yet

- 7 - TaxFormForeign PDFDocument1 page7 - TaxFormForeign PDFDiego MartínNo ratings yet

- Tax InterviewDocument1 pageTax InterviewgrigmihNo ratings yet

- w8 Ben FormDocument1 pagew8 Ben FormJv KunNo ratings yet

- W-8BEN: Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Document1 pageW-8BEN: Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)MatNo ratings yet

- FW 8 Ben 2Document1 pageFW 8 Ben 2DCOM SoftwaresNo ratings yet

- Tax InterviewDocument1 pageTax InterviewrodrigoNo ratings yet

- Foreign Tax Status W8BENDocument9 pagesForeign Tax Status W8BENOctavio Alfredo Solano VillalazNo ratings yet

- FW 8 BenDocument1 pageFW 8 BenELNo ratings yet

- Archivo W 8benDocument1 pageArchivo W 8benFabiola FuentesNo ratings yet

- Dokumen PDFDocument1 pageDokumen PDFkairirisolmayo2611No ratings yet

- HMARUFDocument1 pageHMARUFRadha DasyamNo ratings yet

- W-8BEN: Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Document1 pageW-8BEN: Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Ajmain Abdullah UtshowNo ratings yet

- Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Document1 pageCertificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Study HelpNo ratings yet

- Tax InterviewDocument1 pageTax InterviewAli RachidNo ratings yet

- W8 Ben PDFDocument1 pageW8 Ben PDFAdina JitaruNo ratings yet

- W 8ben With AffidavitDocument1 pageW 8ben With AffidavitFelipeNo ratings yet

- W-8BEN: Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Document1 pageW-8BEN: Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)H PNo ratings yet

- Tax InterviewDocument1 pageTax InterviewidealisteNo ratings yet

- Tax InterviewDocument1 pageTax InterviewChristine Mae CapatoyNo ratings yet

- Tax FormDocument1 pageTax FormitflyiljulwhzthzxfNo ratings yet

- Tax Interview PDFDocument1 pageTax Interview PDFYanka MaletteNo ratings yet

- TopCoder Member Tax Form W-8BENDocument1 pageTopCoder Member Tax Form W-8BENAnonymous FLvU583CNo ratings yet

- Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Document1 pageCertificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)ayoub madaniNo ratings yet

- Tax Interview PDFDocument1 pageTax Interview PDFSazidul IslamNo ratings yet

- Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Document1 pageCertificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Gixxi FlangerNo ratings yet

- FW 8 BenDocument1 pageFW 8 BenAbhinav Anand SinghNo ratings yet

- Tda2689 PDFDocument1 pageTda2689 PDFChristian BaltarNo ratings yet

- Tax InterviewDocument1 pageTax InterviewMohamed HossamNo ratings yet

- Tax InterviewDocument1 pageTax Interviewserkan aldemirNo ratings yet

- FW 8 BenDocument1 pageFW 8 BenEmanuel CastilloNo ratings yet

- W8Ben With US Mailing (FILLABLE)Document2 pagesW8Ben With US Mailing (FILLABLE)Veronica Mtz100% (1)

- Déclaration W-8BENDocument1 pageDéclaration W-8BENhabibdiangone2016No ratings yet

- Tax InterviewDocument1 pageTax Interviewsblackt74No ratings yet

- LivroDocument1 pageLivrolh3281528No ratings yet

- W8 FormDocument2 pagesW8 FormAwais HassanNo ratings yet

- W-8BEN: Donald ChristophDocument1 pageW-8BEN: Donald ChristophpaulNo ratings yet

- Tax InterviewDocument1 pageTax Interviewimma coverNo ratings yet

- Tax InterviewDocument1 pageTax InterviewWilliams PereiraNo ratings yet

- US Internal Revenue Service: Fw8imy AccessibleDocument2 pagesUS Internal Revenue Service: Fw8imy AccessibleIRSNo ratings yet

- Tax InterviewDocument1 pageTax InterviewOwusu Agyapong StephenNo ratings yet

- Tax InterviewDocument1 pageTax InterviewMd Mehedi HasanNo ratings yet

- 6o19pyvf4g5i8z3k Yhz2dqtm4kjv395eDocument1 page6o19pyvf4g5i8z3k Yhz2dqtm4kjv395eEd LucasNo ratings yet

- W-8benDocument1 pageW-8benalanagallvaoNo ratings yet

- Form W-8 BEN (Rev. July 2017)Document1 pageForm W-8 BEN (Rev. July 2017)shivaksh kumarNo ratings yet

- Formulario W-8 BENDocument1 pageFormulario W-8 BENSenpai AlchemistNo ratings yet

- W-8benDocument1 pageW-8bengabriel09.bNo ratings yet

- W-8BEN: Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Document1 pageW-8BEN: Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Moon Debbarma100% (1)

- Tax InterviewDocument1 pageTax InterviewAbde RahimNo ratings yet

- W8 FormDocument1 pageW8 FormMattia PerosinoNo ratings yet

- W-8benDocument1 pageW-8benejfuentes80No ratings yet

- AAI Annual Report 2016-17 EnglishDocument152 pagesAAI Annual Report 2016-17 EnglishmsadithianNo ratings yet

- Form16 SignedDocument7 pagesForm16 SignedrajNo ratings yet

- Funding Amount (INR)Document8 pagesFunding Amount (INR)Rahul PatelNo ratings yet

- Act-6j03 Comp1 1stsem05-06Document14 pagesAct-6j03 Comp1 1stsem05-06RegenLudeveseNo ratings yet

- Key Strategic Issues IdentifiedDocument5 pagesKey Strategic Issues IdentifiedTerix CheongNo ratings yet

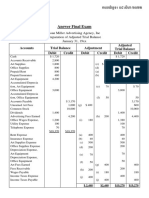

- Answer Final Exam (POA)Document2 pagesAnswer Final Exam (POA)Phâk Tèr ÑgNo ratings yet

- Tutorial 9 QsDocument7 pagesTutorial 9 QsDylan Rabin PereiraNo ratings yet

- Investment Analysis Polar Sports ADocument9 pagesInvestment Analysis Polar Sports AtalabreNo ratings yet

- ISAK 35 Non Profit Oriented EntitiesDocument48 pagesISAK 35 Non Profit Oriented Entitiesnabila dhiyaNo ratings yet

- Maskeliya Plantations PLC: ANNUAL REPORT 2016/ 2017Document130 pagesMaskeliya Plantations PLC: ANNUAL REPORT 2016/ 2017Anjalika PemarathnaNo ratings yet

- IMT Covid19 PDFDocument10 pagesIMT Covid19 PDFPrabhat Mishra100% (2)

- Financial UnderwritingDocument19 pagesFinancial UnderwritingPritish PatnaikNo ratings yet

- There Are Some Major Key Performance Indicators For Chemical Industry: 1. FinancialDocument3 pagesThere Are Some Major Key Performance Indicators For Chemical Industry: 1. FinancialsonuNo ratings yet

- FABM1 - Lesson-13 - Concepts & PrinciplesDocument31 pagesFABM1 - Lesson-13 - Concepts & PrinciplesBP CabreraNo ratings yet

- Incomes Which Do Not Form Part of Total Income: After Studying This Chapter, You Would Be Able ToDocument40 pagesIncomes Which Do Not Form Part of Total Income: After Studying This Chapter, You Would Be Able ToYash SharmaNo ratings yet

- MCQ Chapter 1-9Document36 pagesMCQ Chapter 1-9rupok96% (27)

- BudgetingDocument11 pagesBudgetingWinnie Ann Daquil LomosadNo ratings yet

- A Comparative PESTEL Analysis of Canada PDFDocument47 pagesA Comparative PESTEL Analysis of Canada PDFsparshNo ratings yet

- Glencore International FinalDocument50 pagesGlencore International Finalabiesaga90No ratings yet

- BPI V CIRDocument6 pagesBPI V CIRIan AuroNo ratings yet

- Poa Jan. 2002 Paper 2Document9 pagesPoa Jan. 2002 Paper 2Jerilee SoCute WattsNo ratings yet

- Damo CH 12Document65 pagesDamo CH 12HP KawaleNo ratings yet

- CORPORATE TAX PLANNING AND MANAGEMENT CiaDocument4 pagesCORPORATE TAX PLANNING AND MANAGEMENT CiaAaronNo ratings yet

- 1 Latest Latest Manual LatestDocument9 pages1 Latest Latest Manual LatestRohanMohapatraNo ratings yet

- Efficient Market TheoryDocument31 pagesEfficient Market TheorycasapnaNo ratings yet

- Jamba Juice Company AnalysisDocument24 pagesJamba Juice Company AnalysisMary Kim100% (6)

- TM Account XIDocument197 pagesTM Account XIPadma Ratna Vidya Mandir100% (1)

- Hemanshu Joshi 23Document4 pagesHemanshu Joshi 23HEMANSHU JOSHINo ratings yet

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument10 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionErwin Labayog MedinaNo ratings yet

- Cost Accounting RefresherDocument16 pagesCost Accounting RefresherDemi PardilloNo ratings yet