You might also like

- Small Business Taxation in Ethiopia A Focus On Legal and Practical Issues in Income Tax CategoryDocument21 pagesSmall Business Taxation in Ethiopia A Focus On Legal and Practical Issues in Income Tax CategoryMarta GobenaNo ratings yet

- TAD CH 1 PrintDocument100 pagesTAD CH 1 PrintYitera SisayNo ratings yet

- Selam Proposal 2Document14 pagesSelam Proposal 2sebehadinahmed1992No ratings yet

- Ajol File Journals - 419 - Articles - 240405 - Submission - Proof - 240405 4993 579046 1 10 20230129Document32 pagesAjol File Journals - 419 - Articles - 240405 - Submission - Proof - 240405 4993 579046 1 10 20230129Maalan JiraaNo ratings yet

- The Problem With Our Tax System and How It Affects UsDocument65 pagesThe Problem With Our Tax System and How It Affects Ussan pedro jailNo ratings yet

- Explaining the trajectory of international tax governanceDocument48 pagesExplaining the trajectory of international tax governanceمحمد البناءNo ratings yet

- Chapter 2 Three-Card MonteDocument2 pagesChapter 2 Three-Card MonteSze Ling100% (1)

- 3 MPRA Paper 100617Document27 pages3 MPRA Paper 100617Nur Rohmah Zainul FitriNo ratings yet

- Public Financ and TaxationDocument98 pagesPublic Financ and TaxationEyuel SintayehuNo ratings yet

- Tax Administration Reform in Transition: The Case of CroatiaDocument40 pagesTax Administration Reform in Transition: The Case of CroatiaSwastik GroverNo ratings yet

- Salam 8Document16 pagesSalam 8Galex BaakNo ratings yet

- The Level of Literacy Rate and Tax Education Both Are Different in The Case of Small Cities and TownsDocument4 pagesThe Level of Literacy Rate and Tax Education Both Are Different in The Case of Small Cities and TownsshabywarriachNo ratings yet

- Research Paper On VATDocument60 pagesResearch Paper On VATjtesh2020100% (1)

- Bank Transaction Tax Proposal Discussed as Potential Replacement for India's Complex Tax SystemDocument9 pagesBank Transaction Tax Proposal Discussed as Potential Replacement for India's Complex Tax Systemmandy021190No ratings yet

- Melkamu Reaserch ProfileDocument39 pagesMelkamu Reaserch ProfileNigatu ShiferawNo ratings yet

- Paper9 TaxPayers Attitudes LumumbaDocument11 pagesPaper9 TaxPayers Attitudes LumumbaGerald BarongoNo ratings yet

- 1 Current Tax Reforms (In Process)Document5 pages1 Current Tax Reforms (In Process)Katherin DiazNo ratings yet

- Best Practices To Control Underground Economy in The World: JapanDocument8 pagesBest Practices To Control Underground Economy in The World: JapanAsif RahoojoNo ratings yet

- Waris Taxation 2 PDFDocument33 pagesWaris Taxation 2 PDFMark OmugaNo ratings yet

- Lakshmi EcoDocument5 pagesLakshmi EcoNikhil KalyanNo ratings yet

- Assessment of Tax Collection Problems (The Case of Wolkite Town)Document25 pagesAssessment of Tax Collection Problems (The Case of Wolkite Town)kassahun mesele100% (6)

- Comprehensive Reaction Paper on TRAIN Law and Income TaxationDocument3 pagesComprehensive Reaction Paper on TRAIN Law and Income TaxationVillanueva, Jane G.No ratings yet

- Jimma, EthiopiaDocument51 pagesJimma, EthiopiaRiyaad MandisaNo ratings yet

- Vietnam Law On Corporate Income TaxDocument22 pagesVietnam Law On Corporate Income TaxFTU.CS2 Triệu Thạnh KhangNo ratings yet

- Brooking Paper Owens&HamiltonDocument37 pagesBrooking Paper Owens&HamiltonStuart HamiltonNo ratings yet

- Assignment 1 (Taxation)Document7 pagesAssignment 1 (Taxation)Aikal HakimNo ratings yet

- Mohammad Ali Jinnah University: AssignmentDocument4 pagesMohammad Ali Jinnah University: AssignmentMuhammad TuhaNo ratings yet

- Arbaminch University College of Business and Economics Department of Accounting and FinancDocument8 pagesArbaminch University College of Business and Economics Department of Accounting and FinancbabuNo ratings yet

- Taxation SynopsisDocument5 pagesTaxation SynopsisVanshita GuptaNo ratings yet

- Ethics and Tax ProfessionDocument24 pagesEthics and Tax ProfessionNur AsniNo ratings yet

- Apostol2018 Paying Taxes Is Losing Money'Document23 pagesApostol2018 Paying Taxes Is Losing Money'Muhammad IchsanNo ratings yet

- Assessment of Vat Administration (A Case Study On Bishoftu Town)Document41 pagesAssessment of Vat Administration (A Case Study On Bishoftu Town)chalachew mekonnenNo ratings yet

- BACC3 - Antiniolos, FaieDocument21 pagesBACC3 - Antiniolos, Faiemochi antiniolosNo ratings yet

- Subject: Taxation Laws I (Direct Tax) : Kumail FatimaDocument24 pagesSubject: Taxation Laws I (Direct Tax) : Kumail FatimaVida travel SolutionsNo ratings yet

- Article 3Document41 pagesArticle 3Mihret TadeleNo ratings yet

- How The Excess of Fiscal Evasion Can Influence Public ServicesDocument4 pagesHow The Excess of Fiscal Evasion Can Influence Public ServicesComar JacksonNo ratings yet

- Turbotax Contact Number (1-828-668-2992)Document64 pagesTurbotax Contact Number (1-828-668-2992)PC FixNo ratings yet

- Tax Evasion NigeriaDocument11 pagesTax Evasion NigeriadaydayNo ratings yet

- Critical Review Paper On TaxDocument4 pagesCritical Review Paper On TaxShannia LouieNo ratings yet

- Utilising Tax Literacy and Societal ConfDocument19 pagesUtilising Tax Literacy and Societal ConfNainaNo ratings yet

- Global Tax Governance Needed to Reduce InequalityDocument39 pagesGlobal Tax Governance Needed to Reduce InequalityALBERT IUSTIN BONȚOINo ratings yet

- Debat Pajak SasingDocument3 pagesDebat Pajak SasingFatikhul IrfanNo ratings yet

- Weber 2020 Saez Zucman Book ReviewDocument4 pagesWeber 2020 Saez Zucman Book ReviewBoy McFappoNo ratings yet

- Review and Improve Methods To Prevent and Combat Tax EvasionDocument21 pagesReview and Improve Methods To Prevent and Combat Tax Evasionprincessjel_0711No ratings yet

- Assessment of Vat AdministrationDocument30 pagesAssessment of Vat Administrationshimelis100% (1)

- 2005 JKAU 18-1 05 PEERZADA Towards Self-Enforcing Islamic Tax System - An Alternative To Current ApproachDocument10 pages2005 JKAU 18-1 05 PEERZADA Towards Self-Enforcing Islamic Tax System - An Alternative To Current ApproachFathimah Azzahra JafrilNo ratings yet

- Tax AvoidanceDocument38 pagesTax AvoidancerampayareNo ratings yet

- The Polytechnic, Ibadan: Kayode Oladipupo OlayemiDocument38 pagesThe Polytechnic, Ibadan: Kayode Oladipupo OlayemiSuleiman Abubakar AuduNo ratings yet

- TaxEvasion Lopez March2016Document31 pagesTaxEvasion Lopez March2016The Secret Account of Oda :3No ratings yet

- Proposal Tax Payer EducationDocument22 pagesProposal Tax Payer EducationDenis Robert Mfugale100% (1)

- Principles of TaxationDocument36 pagesPrinciples of TaxationyeyNo ratings yet

- Causes of Tax Evasion and Avoidance-Facts From NCR of India: June 2020Document13 pagesCauses of Tax Evasion and Avoidance-Facts From NCR of India: June 2020Che DivineNo ratings yet

- Tax Policy Research Paper TopicsDocument4 pagesTax Policy Research Paper Topicsfzmgp96k100% (1)

- TaxationDocument34 pagesTaxationShyamKumarKCNo ratings yet

- TAX+AUTHORITY+EFFORT+IN+THE+PREVENTION+AND+DETECTION+OF+TAX+FRAUD+IN+NIGERIADocument9 pagesTAX+AUTHORITY+EFFORT+IN+THE+PREVENTION+AND+DETECTION+OF+TAX+FRAUD+IN+NIGERIAOgunmodede OlamideNo ratings yet

- Taxation Law 2021Document60 pagesTaxation Law 2021eayemeyemieNo ratings yet

- Effectiveness of Income Tax Collection in Sri Lanka EditedDocument38 pagesEffectiveness of Income Tax Collection in Sri Lanka EditedIshu GunasekaraNo ratings yet

- Eco208 Assignment p2Document7 pagesEco208 Assignment p2Yash AgarwalNo ratings yet

- Tax Thesis TitleDocument4 pagesTax Thesis Titlekatieharrisannarbor100% (2)

- Obe Syllabus Acct 411Document12 pagesObe Syllabus Acct 411Maria AmulNo ratings yet

- Statement of Comprehensive Income - Ia3Document16 pagesStatement of Comprehensive Income - Ia3SharjaaahNo ratings yet

- Format. Hum - Self Help Group and Rural Development A Study From Bankura District of West BengalDocument14 pagesFormat. Hum - Self Help Group and Rural Development A Study From Bankura District of West BengalImpact JournalsNo ratings yet

- Macro Macro Objectives - KEYDocument24 pagesMacro Macro Objectives - KEYRobin Kuo100% (1)

- Guidance Note On Market Risk ManagementDocument63 pagesGuidance Note On Market Risk ManagementSonu AgrawalNo ratings yet

- Solution of Homework 4Document4 pagesSolution of Homework 4Kamalakar Reddy100% (2)

- Industry Analysis and Political Economic Social and Technological For Beverage Industry PakistanDocument6 pagesIndustry Analysis and Political Economic Social and Technological For Beverage Industry Pakistani8kuki0% (1)

- 2013 Revenue Code of Marikina CityDocument121 pages2013 Revenue Code of Marikina CityJeremiah John Soriano Nicolas100% (1)

- Week 6 Module 5 Analysis and Interpretation of Financial StatementsDocument31 pagesWeek 6 Module 5 Analysis and Interpretation of Financial StatementsZed Mercy86% (14)

- Principles of Accounting and Financial StatementsDocument9 pagesPrinciples of Accounting and Financial Statementsahmed100% (1)

- Business Research On Consumer Buying Behavior After The Implementation of Sin Tax Law in The PhilippinesDocument41 pagesBusiness Research On Consumer Buying Behavior After The Implementation of Sin Tax Law in The PhilippinesMajoy Mendoza100% (2)

- AccentureDocument16 pagesAccenturesimphiwe8043No ratings yet

- 2.Md. Shamim Hossain & Abdul Alim Basher - Final PaperDocument9 pages2.Md. Shamim Hossain & Abdul Alim Basher - Final PaperiisteNo ratings yet

- The Economic Security of Business Transactions: Management in BusinessDocument462 pagesThe Economic Security of Business Transactions: Management in BusinessChartridge Books OxfordNo ratings yet

- MAC 1E Study Guide CompleteDocument225 pagesMAC 1E Study Guide Completealicia1990No ratings yet

- Microsoft Dynamics GP 10.0 Table ReferenceDocument569 pagesMicrosoft Dynamics GP 10.0 Table ReferencekempecNo ratings yet

- Edoc - Pub - Igcse Economics NotesDocument26 pagesEdoc - Pub - Igcse Economics NotesKostas 2No ratings yet

- Recent Developments in RE Laws Taxation by CA. Jayesh Kariya 1 PDFDocument55 pagesRecent Developments in RE Laws Taxation by CA. Jayesh Kariya 1 PDFManu IttinaNo ratings yet

- Gov't Accounting Theories (GATDocument82 pagesGov't Accounting Theories (GATorly100% (1)

- OPPORTUNITY SEEKING, SCREENING, AND SEIZING CHPTR 2Document39 pagesOPPORTUNITY SEEKING, SCREENING, AND SEIZING CHPTR 2Remelyn Azor91% (11)

- FS TypesDocument23 pagesFS TypesAnamika VermaNo ratings yet

- Tolentino Vs SecretaryDocument7 pagesTolentino Vs SecretaryHansel Jake B. PampiloNo ratings yet

- ABC Company Business PlanDocument29 pagesABC Company Business Planmukesh.33No ratings yet

- TESCO Share Fundamentals (TSCO) - London Stock ExchangeDocument5 pagesTESCO Share Fundamentals (TSCO) - London Stock ExchangeinuNo ratings yet

- Record of Society of Actuaries 1988 VOL. 14 NO. 1Document20 pagesRecord of Society of Actuaries 1988 VOL. 14 NO. 1Nimrod WeinbergNo ratings yet

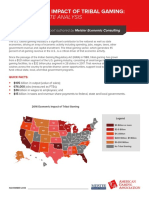

- Economic Impact of Tribal GamingDocument2 pagesEconomic Impact of Tribal GamingKJZZ PhoenixNo ratings yet

- Affidavit of RemittanceDocument1 pageAffidavit of RemittancenbmantillaNo ratings yet

- Samsung C&T 2014 Financial StatementsDocument126 pagesSamsung C&T 2014 Financial StatementsJinay ShahNo ratings yet

- Week13 SolutionsDocument14 pagesWeek13 SolutionsRian RorresNo ratings yet

- TVM Formulas Guide: Calculate Present, Future Values & AnnuitiesDocument56 pagesTVM Formulas Guide: Calculate Present, Future Values & AnnuitiesSaptorshi BagchiNo ratings yet