You might also like

- Using Economic Indicators to Improve Investment AnalysisFrom EverandUsing Economic Indicators to Improve Investment AnalysisRating: 3.5 out of 5 stars3.5/5 (1)

- Chap 60Document3 pagesChap 60Vijay ManeNo ratings yet

- Private Equity InvestmentDocument12 pagesPrivate Equity InvestmentRishipal ChauhanNo ratings yet

- Mutual Fund Portfolio Insight Report: Mohit GuptaDocument7 pagesMutual Fund Portfolio Insight Report: Mohit GuptaMohit GuptaNo ratings yet

- Real Estate: Presented By: Mukesh Singh SauravDocument13 pagesReal Estate: Presented By: Mukesh Singh SauravSaurabh SagarNo ratings yet

- SRPM Economy Analysis - Group-7Document58 pagesSRPM Economy Analysis - Group-7hiitsds12bNo ratings yet

- NNNNN NNNNNNNNN NNNNNNNNNDocument70 pagesNNNNN NNNNNNNNN NNNNNNNNNSheheryar KhanNo ratings yet

- Real Estate: Nishant Kumar PGDM 09 JimlDocument13 pagesReal Estate: Nishant Kumar PGDM 09 Jimlpankaj09128No ratings yet

- Japonia & TurciaDocument8 pagesJaponia & Turciabiancaftw90No ratings yet

- MD & Ceo CFO CRO CIO: Note For Investment Operation CommitteeDocument4 pagesMD & Ceo CFO CRO CIO: Note For Investment Operation CommitteeAyushi somaniNo ratings yet

- IREF V 6 Pager Brochure - X UnitsDocument6 pagesIREF V 6 Pager Brochure - X UnitsPushpa DeviNo ratings yet

- 'KQHK NhikoyhDocument12 pages'KQHK NhikoyhGiri BabaNo ratings yet

- IREF V 6 Pager Brochure - Regular UnitsDocument6 pagesIREF V 6 Pager Brochure - Regular UnitsPushpa DeviNo ratings yet

- Chap 62Document2 pagesChap 62api-19641717No ratings yet

- BD FinanceDocument5 pagesBD Financesibgat ullahNo ratings yet

- India: Asia-Pacific'S Next Mutual Funds Giant: Markets and Securities Services - 1Document10 pagesIndia: Asia-Pacific'S Next Mutual Funds Giant: Markets and Securities Services - 1EdifyNo ratings yet

- Aug-2010-Citi Indonesia ConferenceDocument67 pagesAug-2010-Citi Indonesia ConferenceFatchul WachidNo ratings yet

- Nitori Analyst ReportDocument7 pagesNitori Analyst ReportAhmad HaikalNo ratings yet

- The Philippine Stock Exchange, Inc.: February 26, 2021Document212 pagesThe Philippine Stock Exchange, Inc.: February 26, 2021Algen Lyn MendozaNo ratings yet

- DDW 20201105 PDFDocument1 pageDDW 20201105 PDFVimal SharmaNo ratings yet

- Monthly Bulletin July 2023 EnglishDocument13 pagesMonthly Bulletin July 2023 EnglishNirmal MenonNo ratings yet

- Government Domestic Borrowing: Monthly Report OnDocument8 pagesGovernment Domestic Borrowing: Monthly Report Onrashedul islamNo ratings yet

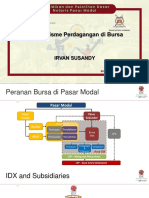

- Materi Mekanisme Perdagangan LMKA Nov 2020 - BPK IrvanDocument29 pagesMateri Mekanisme Perdagangan LMKA Nov 2020 - BPK IrvannurlisaNo ratings yet

- Debt 3Document16 pagesDebt 3mohsin.usafzai932No ratings yet

- January 21, 2022: Press ReleaseDocument2 pagesJanuary 21, 2022: Press ReleaseAayush GuptaNo ratings yet

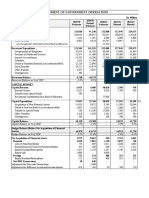

- Statement of Government Operations: O/w Exceptional Contribution From Bank of Mauritius 33,000Document2 pagesStatement of Government Operations: O/w Exceptional Contribution From Bank of Mauritius 33,000Yashas SridatNo ratings yet

- India Grid Q3FY18 - Result Update - Axis Direct - 22012018 - 22!01!2018 - 14Document5 pagesIndia Grid Q3FY18 - Result Update - Axis Direct - 22012018 - 22!01!2018 - 14saransh saranshNo ratings yet

- Portfolio Management: Assortment of Investments Options To Enhance Portfolio ValueDocument24 pagesPortfolio Management: Assortment of Investments Options To Enhance Portfolio Valuechintan shahNo ratings yet

- PT Nusantara Infrastructure TBK: Draft 1 (For Discussion)Document6 pagesPT Nusantara Infrastructure TBK: Draft 1 (For Discussion)Cindy CinintyaNo ratings yet

- Iiww 031210Document4 pagesIiww 0312109913004606No ratings yet

- 0315富邦年報 - 英文.indd 1 2021/5/17 下午 02:54:09Document32 pages0315富邦年報 - 英文.indd 1 2021/5/17 下午 02:54:09YudyChenNo ratings yet

- DEL L&T Infrastructure BondDocument3 pagesDEL L&T Infrastructure Bondpoly899No ratings yet

- Indian Mutual Fund IndustryDocument25 pagesIndian Mutual Fund Industryravijha_1984No ratings yet

- 5e7d86f900475 2019 BPI Audited FS CompressedDocument125 pages5e7d86f900475 2019 BPI Audited FS CompressedHannah Brynne UrreraNo ratings yet

- Current State of Japanese Business in IndiaDocument13 pagesCurrent State of Japanese Business in IndiaPayal KathiawadiNo ratings yet

- Wipro Limited: Investor PresentationDocument22 pagesWipro Limited: Investor PresentationKaveri PandeyNo ratings yet

- IapmDocument6 pagesIapmvishalsingh9669No ratings yet

- Wipro Limited: Investor PresentationDocument22 pagesWipro Limited: Investor Presentationashokdb2kNo ratings yet

- Indian Stock MarketsDocument13 pagesIndian Stock Marketsmr.avdheshsharmaNo ratings yet

- List of Content: FINANCIAL STATEMENT - Asat30September2010 (Unaudited)Document17 pagesList of Content: FINANCIAL STATEMENT - Asat30September2010 (Unaudited)Aziz MuhammadNo ratings yet

- Infra Bonds FAQs PDFDocument3 pagesInfra Bonds FAQs PDFAnshuman SharmaNo ratings yet

- Debt Bulletin-Govt. of The PunjabDocument4 pagesDebt Bulletin-Govt. of The PunjabSaqib JoyiaNo ratings yet

- Investor Presentation FY13 v1Document16 pagesInvestor Presentation FY13 v1Shakti ShuklaNo ratings yet

- Indonesia: The Delta Variant and Lagging Vaccination Have Set Back The RecoveryDocument4 pagesIndonesia: The Delta Variant and Lagging Vaccination Have Set Back The RecoveryTopan ArdiansyahNo ratings yet

- Data SheetDocument3 pagesData SheetAmey SawantNo ratings yet

- BS Delhi English 22-10-2022Document26 pagesBS Delhi English 22-10-2022Relaxing MusicNo ratings yet

- Saad - IFDocument5 pagesSaad - IFRidwan KabirNo ratings yet

- Ptmail m1219 Ss Two Stock Special Report PDFDocument18 pagesPtmail m1219 Ss Two Stock Special Report PDFAaron MartinNo ratings yet

- Zee Entertainment SELL (Recommendation Downgrade) 20240122Document13 pagesZee Entertainment SELL (Recommendation Downgrade) 20240122Rohan KhannaNo ratings yet

- Role of FII in INDIAN Capital Market: Presented By: Sanketh Shetty HarishDocument35 pagesRole of FII in INDIAN Capital Market: Presented By: Sanketh Shetty HarishHarish ShettyNo ratings yet

- Strategic Financial Analysis of Diversified and Undiversified CompanyDocument15 pagesStrategic Financial Analysis of Diversified and Undiversified CompanyarunprakaashNo ratings yet

- Analyst PPT De9 PDFDocument65 pagesAnalyst PPT De9 PDFAmit GagraniNo ratings yet

- INDIA@2030 Presentation - M.D. PaiDocument33 pagesINDIA@2030 Presentation - M.D. Paimannugupta123No ratings yet

- Credit Risk - JPM Case Study IIM KDocument8 pagesCredit Risk - JPM Case Study IIM KSourabh Agrawal 23No ratings yet

- Globalising Cost of Capital Cap Budgeting Case - Akash LodhaDocument78 pagesGlobalising Cost of Capital Cap Budgeting Case - Akash LodhaKushal AdaniNo ratings yet

- Financials of Fleet Power Inc. 2020 - V2Document53 pagesFinancials of Fleet Power Inc. 2020 - V2john markNo ratings yet

- Wipro Investor PPT q4 Fy 2022Document22 pagesWipro Investor PPT q4 Fy 2022sri KarthikeyanNo ratings yet

- Ystematic Nvestment Lan UTI: An Early & Regular Investment Today, Leads To Prosperous TomorrowDocument26 pagesYstematic Nvestment Lan UTI: An Early & Regular Investment Today, Leads To Prosperous Tomorrown_akash3977No ratings yet

- Exporting Services: A Developing Country PerspectiveFrom EverandExporting Services: A Developing Country PerspectiveRating: 5 out of 5 stars5/5 (2)

- The 6 Pillars of Successful BusinessesDocument81 pagesThe 6 Pillars of Successful BusinessesJoshelle B. BanciloNo ratings yet

- At A Glance Corporate Fact SheetDocument4 pagesAt A Glance Corporate Fact SheetpanchoNo ratings yet

- DerivativesDocument12 pagesDerivativesVenn Bacus RabadonNo ratings yet

- The ABC of Creating A Mean Reversion StrategyDocument11 pagesThe ABC of Creating A Mean Reversion StrategyAnurag GroverNo ratings yet

- Pratim SIP FinalDocument74 pagesPratim SIP Finalpratim shindeNo ratings yet

- International Business and TerrorismDocument4 pagesInternational Business and TerrorismGregory George NinanNo ratings yet

- Fa Unit V Final PDFDocument8 pagesFa Unit V Final PDFAakaash100% (1)

- Are Market Efficient PDFDocument2 pagesAre Market Efficient PDFVignesh BhatNo ratings yet

- SEC Vs SantosDocument12 pagesSEC Vs SantosGigiRuizTicarNo ratings yet

- Ignou McomDocument6 pagesIgnou McomVijay Kumar GNo ratings yet

- Adjudication Order in Respect of Shailesh Shah Securities PVT LTD in The Matter of Essdee Aluminium LimitedDocument9 pagesAdjudication Order in Respect of Shailesh Shah Securities PVT LTD in The Matter of Essdee Aluminium LimitedShyam SunderNo ratings yet

- Capital Account Convertibility (ECO)Document40 pagesCapital Account Convertibility (ECO)KhushbooNo ratings yet

- Answer To MTP - Final - Syllabus 2012 - Dec2015 - Set 1: Paper - 18 - Corporate Financial ReportingDocument26 pagesAnswer To MTP - Final - Syllabus 2012 - Dec2015 - Set 1: Paper - 18 - Corporate Financial ReportingBasant OjhaNo ratings yet

- SFMSOLUTIONS Master Minds PDFDocument10 pagesSFMSOLUTIONS Master Minds PDFHari KrishnaNo ratings yet

- NO No Kwit No Container Size Tanggal Nopol Jumh Harga Keterangan IN OUT IN OUT HariDocument2 pagesNO No Kwit No Container Size Tanggal Nopol Jumh Harga Keterangan IN OUT IN OUT Hariapul sianturiNo ratings yet

- BPI Vs Guevara Case DigestDocument2 pagesBPI Vs Guevara Case DigestAnne Soria33% (3)

- Ross 7 e CH 31Document50 pagesRoss 7 e CH 31Antora HoqueNo ratings yet

- The Bankruptcy of The United StatesDocument8 pagesThe Bankruptcy of The United StatesncwazzyNo ratings yet

- Seth Klarman Baupost Group LettersDocument58 pagesSeth Klarman Baupost Group LettersAndr Ei100% (4)

- FINN 341-Financial Institutions & Market - BashrullahDocument11 pagesFINN 341-Financial Institutions & Market - BashrullahTahir AfzalNo ratings yet

- Global Technology Fund A Acc: Janus HendersonDocument2 pagesGlobal Technology Fund A Acc: Janus Hendersondoc_oz3298No ratings yet

- Blackbook Project On Foreign Exchange and Its Risk Management - 237312993Document61 pagesBlackbook Project On Foreign Exchange and Its Risk Management - 237312993Aman Tiwari75% (4)

- Calculation Methof of KSE-100 IndexDocument23 pagesCalculation Methof of KSE-100 Indexamina_rabia100% (2)

- Company Law PDFDocument3 pagesCompany Law PDFJaspreet SinghNo ratings yet

- Maritime Capital Partners LP Is A Hedge Fund Based in New York, New York Which Founded by Baris Dincer and Greg Gurevich in April 2010.Document2 pagesMaritime Capital Partners LP Is A Hedge Fund Based in New York, New York Which Founded by Baris Dincer and Greg Gurevich in April 2010.BONDTRADER100% (2)

- Super MACD Trader Guide PDFDocument36 pagesSuper MACD Trader Guide PDFPrajan J100% (1)

- Efx2.0 White PaperDocument13 pagesEfx2.0 White PaperThatOneRichGuyNo ratings yet

- DerivativesDocument53 pagesDerivativesnikitsharmaNo ratings yet

- Chapter 10 Stock Valuation A Second LookDocument33 pagesChapter 10 Stock Valuation A Second LookshuNo ratings yet