You might also like

- Plumbing Max FajardoDocument175 pagesPlumbing Max FajardoKeannosuke SabusapNo ratings yet

- ResumeDocument2 pagesResumeKeannosuke SabusapNo ratings yet

- A Damaged Culture By: James Fallows A New Philippines?Document16 pagesA Damaged Culture By: James Fallows A New Philippines?Keannosuke SabusapNo ratings yet

- Architecture in IndiaDocument46 pagesArchitecture in IndiaKeannosuke SabusapNo ratings yet

- Elements of Design: 1. LineDocument9 pagesElements of Design: 1. LineKeannosuke SabusapNo ratings yet

- Planning 1: Landscape DesignDocument44 pagesPlanning 1: Landscape DesignKeannosuke SabusapNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Answers To Chapter 27 and 28 CasesDocument4 pagesAnswers To Chapter 27 and 28 CasesVic RabayaNo ratings yet

- Loan Managemetn of RAKUBDocument72 pagesLoan Managemetn of RAKUBMonirul Islam Milon50% (4)

- Banking Law ProjectDocument25 pagesBanking Law ProjectRavi Singh SolankiNo ratings yet

- Í (Zkfè Pagayunan Lemuelâââââ R Ç 3) 24lî Mr. Lemuel Rutaquio PagayunanDocument4 pagesÍ (Zkfè Pagayunan Lemuelâââââ R Ç 3) 24lî Mr. Lemuel Rutaquio PagayunanJohn Robertson DayaoNo ratings yet

- Sebi 1234567890Document5 pagesSebi 1234567890John DaveNo ratings yet

- What Is RMADocument1 pageWhat Is RMAPurevdorj DorjNo ratings yet

- Non Banking Financial InstitutionsDocument18 pagesNon Banking Financial InstitutionsNimesh Shah100% (1)

- Advanced Accounting Fischer 10th Edition Solutions ManualDocument7 pagesAdvanced Accounting Fischer 10th Edition Solutions ManualDanielLopezxjbn100% (38)

- Acct Statement - XX0647 - 14042023 PDFDocument5 pagesAcct Statement - XX0647 - 14042023 PDFPritam GoswamiNo ratings yet

- A Summer Training Project Report On: "Financial Statement Analysis" OF Orissa State Co-Operative Bank Ltd. BhubaneswarDocument74 pagesA Summer Training Project Report On: "Financial Statement Analysis" OF Orissa State Co-Operative Bank Ltd. BhubaneswarNaman JainNo ratings yet

- Consumer Credit Marketing System in Bangladesh-A Case Study On Dhaka BankDocument13 pagesConsumer Credit Marketing System in Bangladesh-A Case Study On Dhaka BankAli Haider MohammadullahNo ratings yet

- Chapter 2 - Problem SolvingDocument20 pagesChapter 2 - Problem SolvingMaria Licuanan100% (1)

- Deepak ProjectDocument88 pagesDeepak ProjectSandeep JacobNo ratings yet

- Demo Prob Ch02 P2 20Document29 pagesDemo Prob Ch02 P2 20Fady AhmedNo ratings yet

- Credit Risk Literature ReviewDocument6 pagesCredit Risk Literature Reviewnelnlpvkg100% (1)

- Aud 1&2 - CceDocument6 pagesAud 1&2 - Ccecherish melwinNo ratings yet

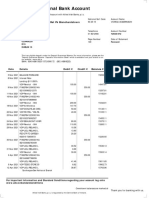

- Personal Bank Account: West End Ret PK BlanchardstownDocument5 pagesPersonal Bank Account: West End Ret PK BlanchardstownViorica Zaporojan Iascerinschi100% (3)

- BRS Practice QuestionsDocument2 pagesBRS Practice Questionssyed ali raza kazmiNo ratings yet

- Coding and Decoding QuestionsDocument28 pagesCoding and Decoding QuestionsAbdulawwal IntisorNo ratings yet

- Sample Question Papers For Certificate Course On Ind AS: The Institute of Chartered Accountants of IndiaDocument36 pagesSample Question Papers For Certificate Course On Ind AS: The Institute of Chartered Accountants of IndiaChristen CastilloNo ratings yet

- Pas 40 Investment PropertyDocument4 pagesPas 40 Investment PropertykristineNo ratings yet

- Accounting 5 - Intermediate Accounting Part 3 Statement of Financial PositonDocument3 pagesAccounting 5 - Intermediate Accounting Part 3 Statement of Financial PositonCj GarciaNo ratings yet

- HDFC ERGO General Insurance Company LimitedDocument2 pagesHDFC ERGO General Insurance Company LimitedArghyaPodderNo ratings yet

- Sbi Project ReportDocument114 pagesSbi Project Reportthyristorscr78% (9)

- Accounting 7th Edition Horngren Solutions ManualDocument75 pagesAccounting 7th Edition Horngren Solutions ManualAdrianHayescgide100% (14)

- Time Value of MoneyDocument45 pagesTime Value of MoneyKimberly BanuelosNo ratings yet

- Suco 2018Document7 pagesSuco 2018PUNI100% (1)

- Account Statement From 1 Mar 2023 To 31 Mar 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument3 pagesAccount Statement From 1 Mar 2023 To 31 Mar 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSuresh VatipalliNo ratings yet

- Seabank Statement GiselaDocument4 pagesSeabank Statement Giseladeajohn093No ratings yet

- Classification of AccountsDocument4 pagesClassification of Accountsvikas sunnyNo ratings yet